Question: Q5 Exercise 16-28 (Static) Multiple temporary differences; balance sheet presentation; financial statement effects [LO16-2, 16-3, 16-5, 16-6, 16-8] Exercise 16-28 (Static) Multiple temporary differences; balance

Q5 Exercise 16-28 (Static) Multiple temporary differences; balance sheet presentation; financial statement effects [LO16-2, 16-3, 16-5, 16-6, 16-8]

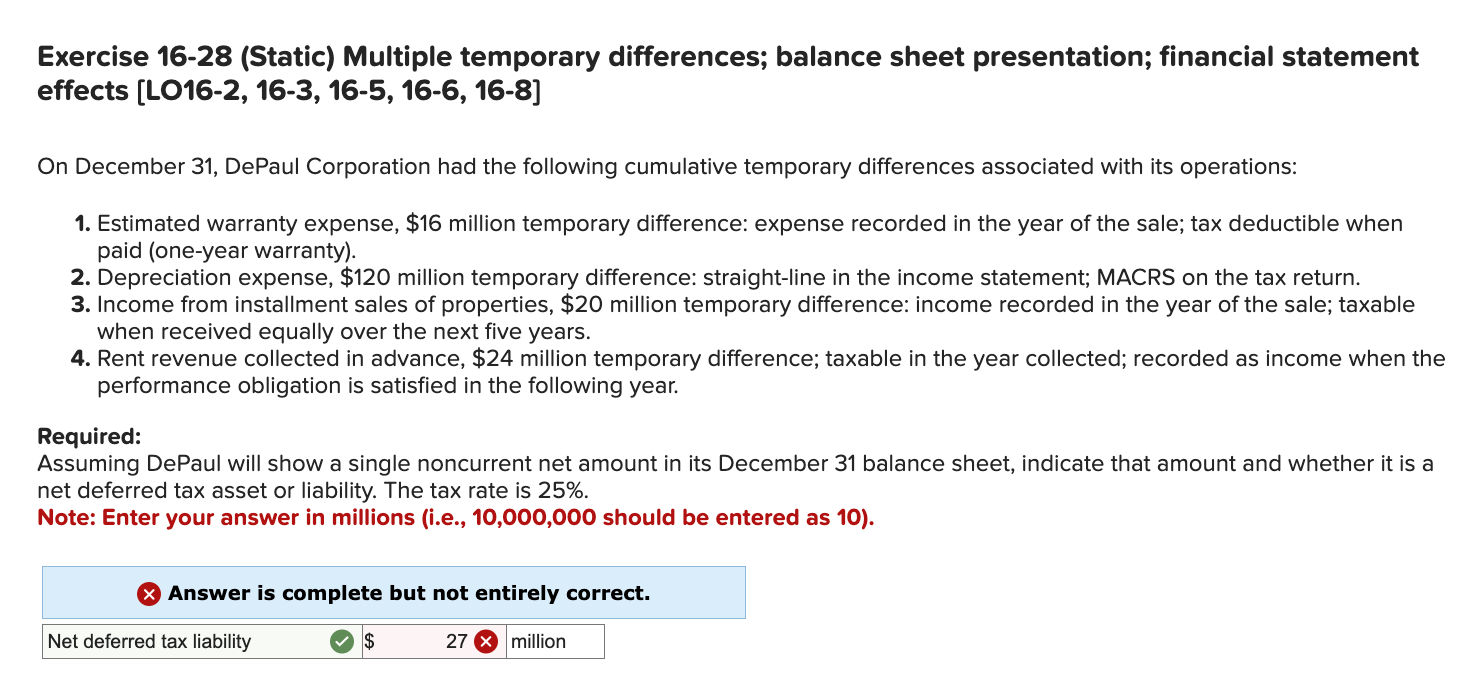

Exercise 16-28 (Static) Multiple temporary differences; balance sheet presentation; financial statement effects [LO16-2, 16-3, 16-5, 16-6, 16-8] On December 31, DePaul Corporation had the following cumulative temporary differences associated with its operations: 1. Estimated warranty expense, $16 million temporary difference: expense recorded in the year of the sale; tax deductible when paid (one-year warranty). 2. Depreciation expense, $120 million temporary difference: straight-line in the income statement; MACRS on the tax return. 3. Income from installment sales of properties, $20 million temporary difference: income recorded in the year of the sale; taxable when received equally over the next five years. 4. Rent revenue collected in advance, $24 million temporary difference; taxable in the year collected; recorded as income when the performance obligation is satisfied in the following year. Required: Assuming DePaul will show a single noncurrent net amount in its December 31 balance sheet, indicate that amount and whether it is a net deferred tax asset or liability. The tax rate is 25%. Note: Enter your answer in millions (i.e., 10,000,000 should be entered as 10)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts