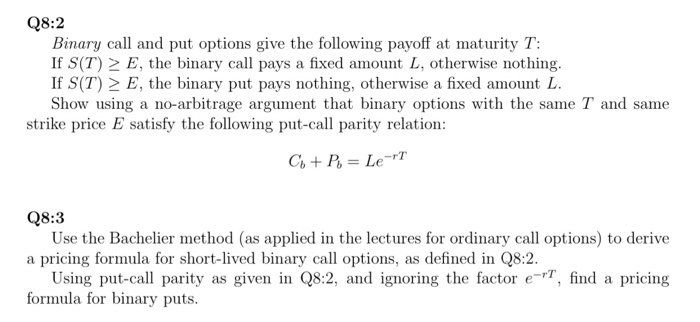

Question: Q8:2 Binary call and put options give the following payoff at maturity T: If S(T) E, the binary call pays a fixed amount L, otherwise

Q8:2 Binary call and put options give the following payoff at maturity T: If S(T) E, the binary call pays a fixed amount L, otherwise nothing. If S(T) > E, the binary put pays nothing, otherwise a fixed amount L. Show using a no-arbitrage argument that binary options with the same T and same strike price E satisfy the following put-call parity relation: C + P = Le-rT Q8:3 Use the Bachelier method (as applied in the lectures for ordinary call options) to derive a pricing formula for short-lived binary call options, as defined in Q8:2. Using put-call parity as given in Q8:2, and ignoring the factor e-T, find a pricing formula for binary puts. Q8:2 Binary call and put options give the following payoff at maturity T: If S(T) E, the binary call pays a fixed amount L, otherwise nothing. If S(T) > E, the binary put pays nothing, otherwise a fixed amount L. Show using a no-arbitrage argument that binary options with the same T and same strike price E satisfy the following put-call parity relation: C + P = Le-rT Q8:3 Use the Bachelier method (as applied in the lectures for ordinary call options) to derive a pricing formula for short-lived binary call options, as defined in Q8:2. Using put-call parity as given in Q8:2, and ignoring the factor e-T, find a pricing formula for binary puts

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts