Question: q8q1 please help me answer this question as soon as you can please. Seaforth International wrote off the following accounts receivable as uncollectible for the

q8q1 please help me answer this question as soon as you can please.

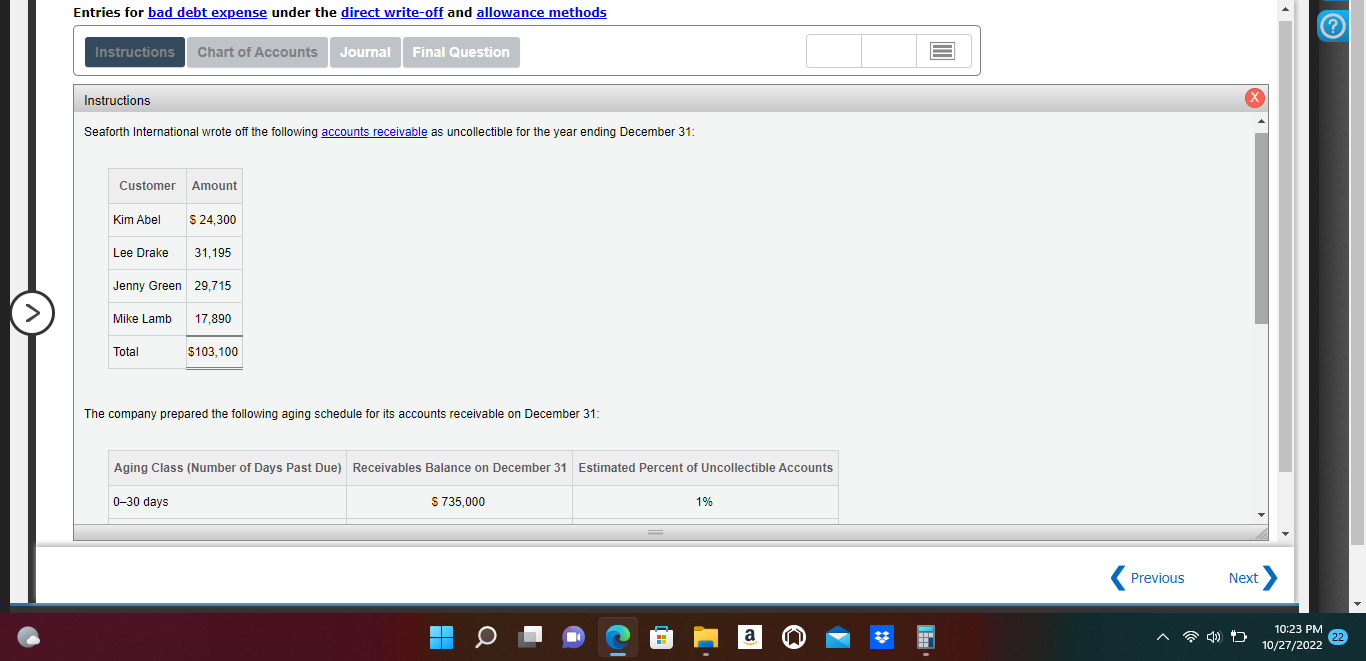

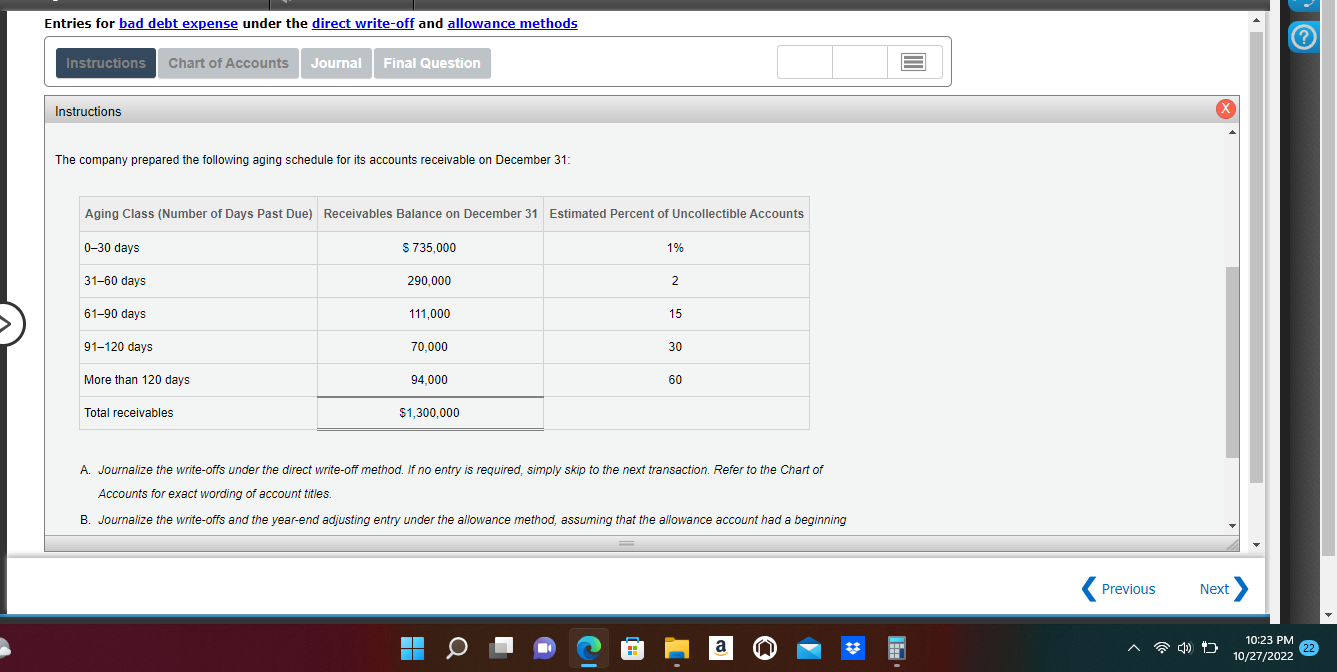

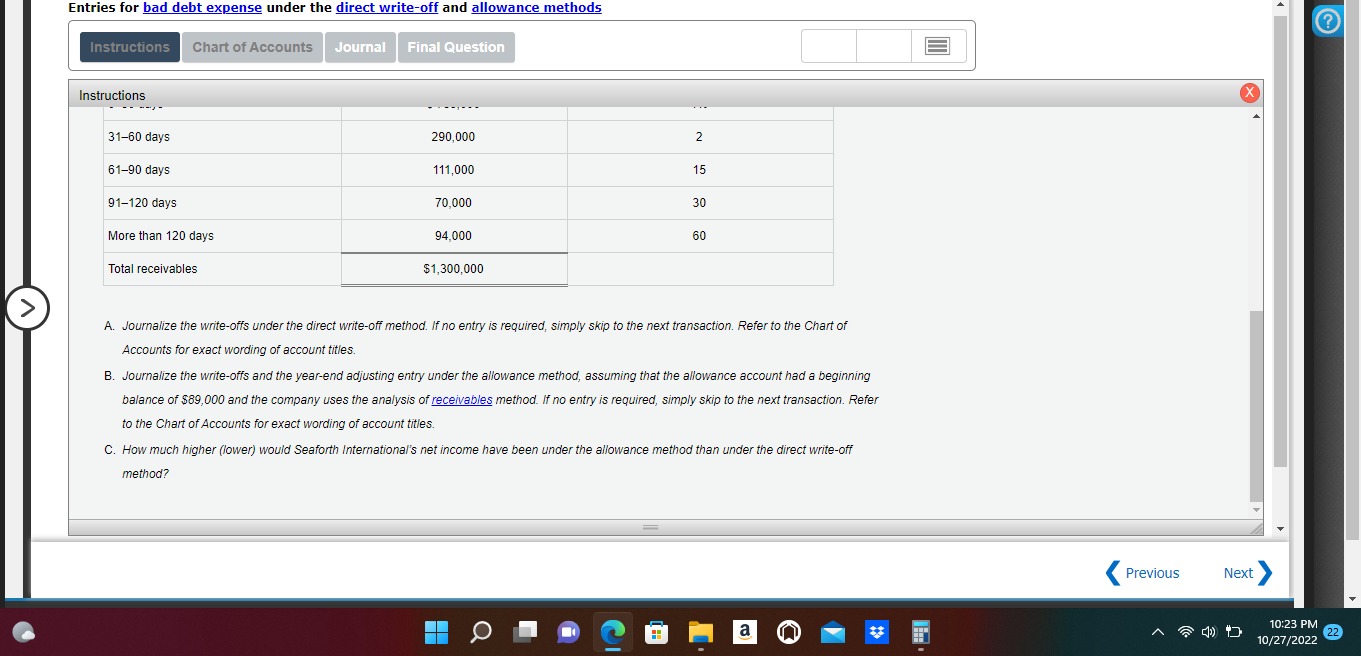

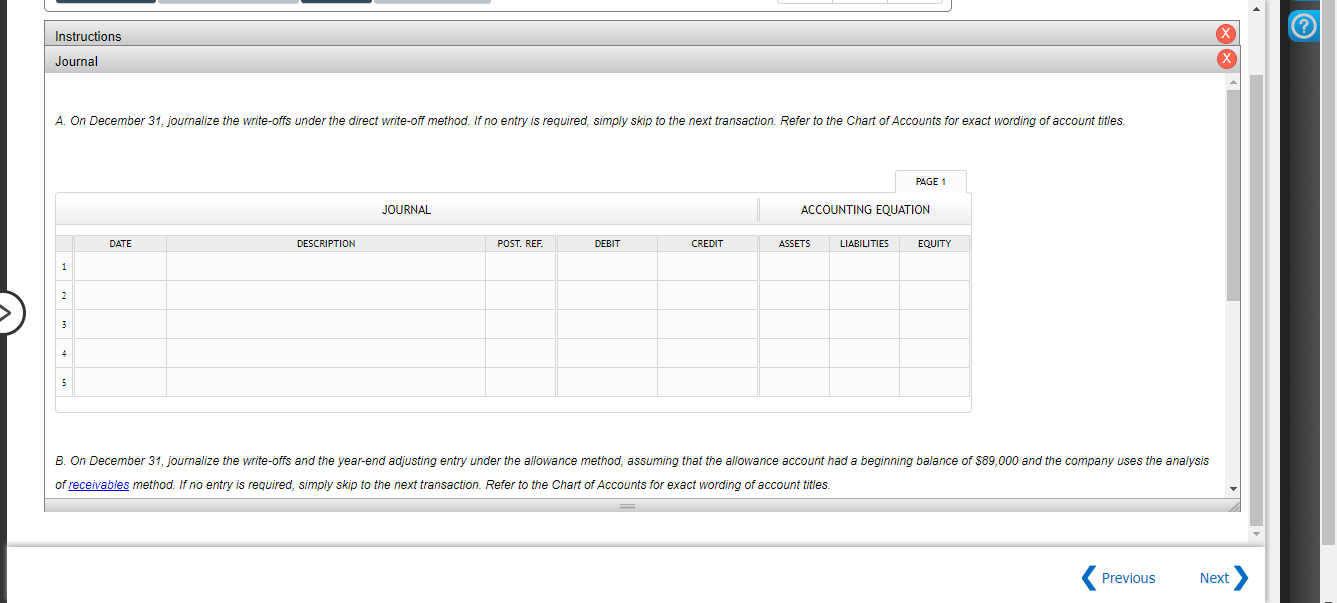

Seaforth International wrote off the following accounts receivable as uncollectible for the year ending December 31: The company prepared the following aging schedule for its accounts receivable on December 31 : The company prepared the following aging schedule for its accounts receivable on December 31 : A. Journalize the write-offs under the direct write-off method. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. B. Journalize the write-offs and the year-end adjusting entry under the allowance method, assuming that the allowance account had a beginning A. Journalize the write-offs under the direct write-off method. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. B. Journalize the write-offs and the year-end adjusting entry under the allowance method, assuming that the allowance account had a beginning balance of $89,000 and the company uses the analysis of receivables method. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. C. How much higher (lower) would Seaforth International's net income have been under the allowance method than under the direct write-off method? of receivables method. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. analysis of method. If no entry is required, simply skip to the next transaction. Refer to the Chart of Accounts for exact wording of account titles. Entries for bad debt expense under the direct write-off and allowance methods

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts