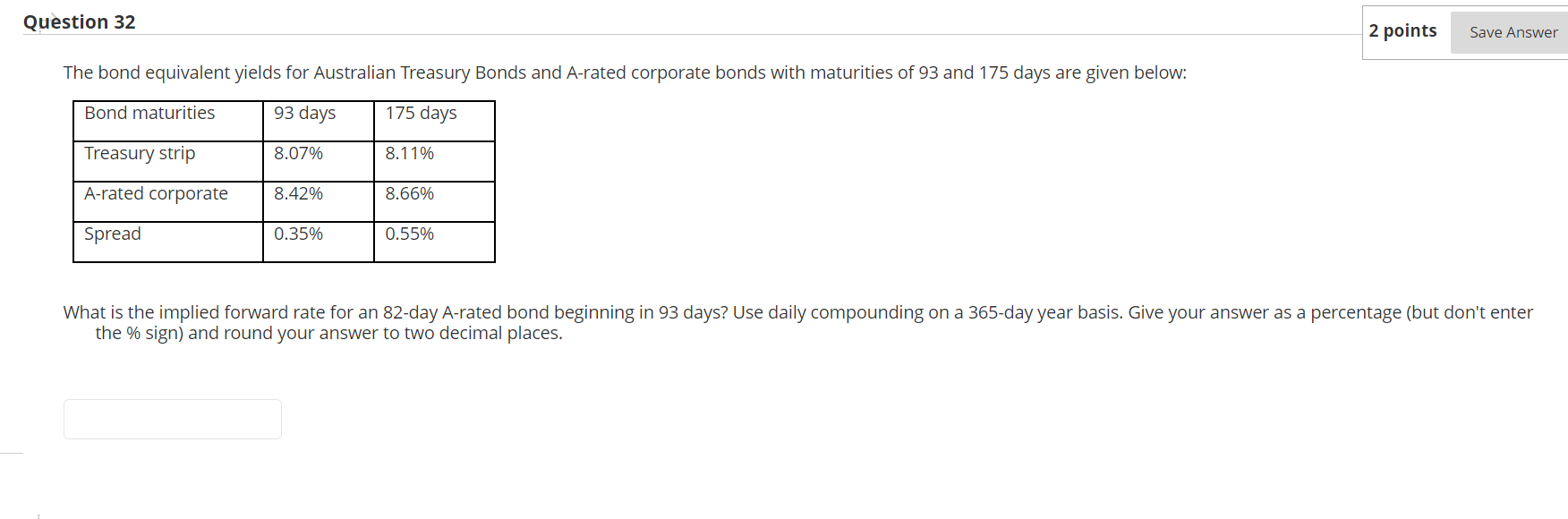

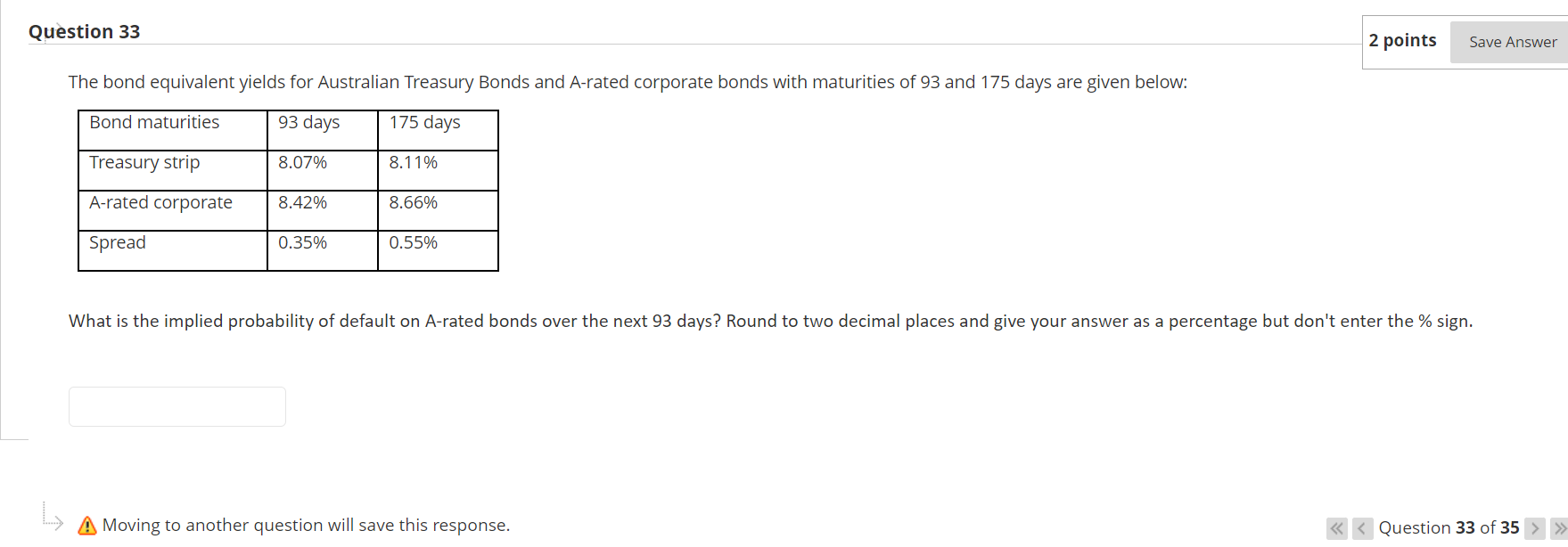

Question: Quastlon 32 2 points Save Answer The bond equivalent yields for Australian Treasury Bonds and Aerated corporate bonds with maturities of 93 and 175 days

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock