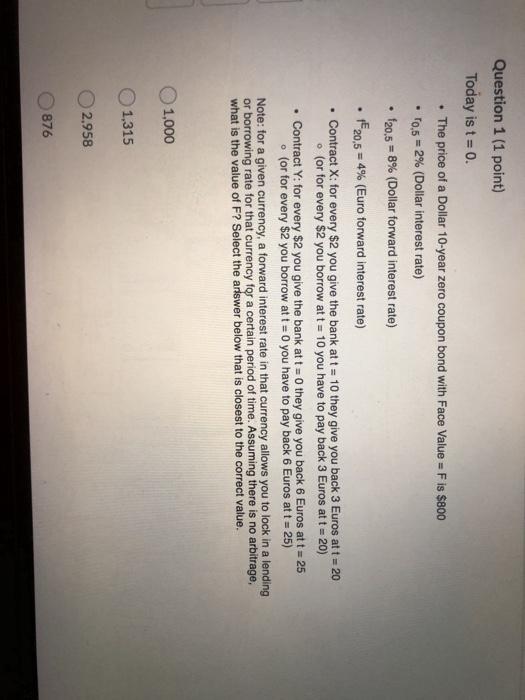

Question: . . Question 1 (1 point) Today is t = 0. The price of a Dollar 10-year zero coupon bond with Face Value = F

. . Question 1 (1 point) Today is t = 0. The price of a Dollar 10-year zero coupon bond with Face Value = F is $800 10.5 = 2% (Dollar interest rate) f20,5 = 8% (Dollar forward interest rate) 20,5 = 4% (Euro forward interest rate) Contract X: for every $2 you give the bank att = 10 they give you back 3 Euros att = 20 (or for every $2 you borrow at t = 10 you have to pay back 3 Euros att = 20) Contract Y: for every $2 you give the bank at t=0 they give you back 6 Euros att = 25 (or for every $2 you borrow at t = 0 you have to pay back 6 Euros at t = 25) Note: for a given currency, a forward interest rate in that currency allows you to lock in a lending or borrowing rate for that currency for a certain period of time. Assuming there is no arbitrage, what is the value of F? Select the answer below that is closest to the correct value. . 1,000 1,315 2,958 876 . . Question 1 (1 point) Today is t = 0. The price of a Dollar 10-year zero coupon bond with Face Value = F is $800 10.5 = 2% (Dollar interest rate) f20,5 = 8% (Dollar forward interest rate) 20,5 = 4% (Euro forward interest rate) Contract X: for every $2 you give the bank att = 10 they give you back 3 Euros att = 20 (or for every $2 you borrow at t = 10 you have to pay back 3 Euros att = 20) Contract Y: for every $2 you give the bank at t=0 they give you back 6 Euros att = 25 (or for every $2 you borrow at t = 0 you have to pay back 6 Euros at t = 25) Note: for a given currency, a forward interest rate in that currency allows you to lock in a lending or borrowing rate for that currency for a certain period of time. Assuming there is no arbitrage, what is the value of F? Select the answer below that is closest to the correct value. . 1,000 1,315 2,958 876

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts