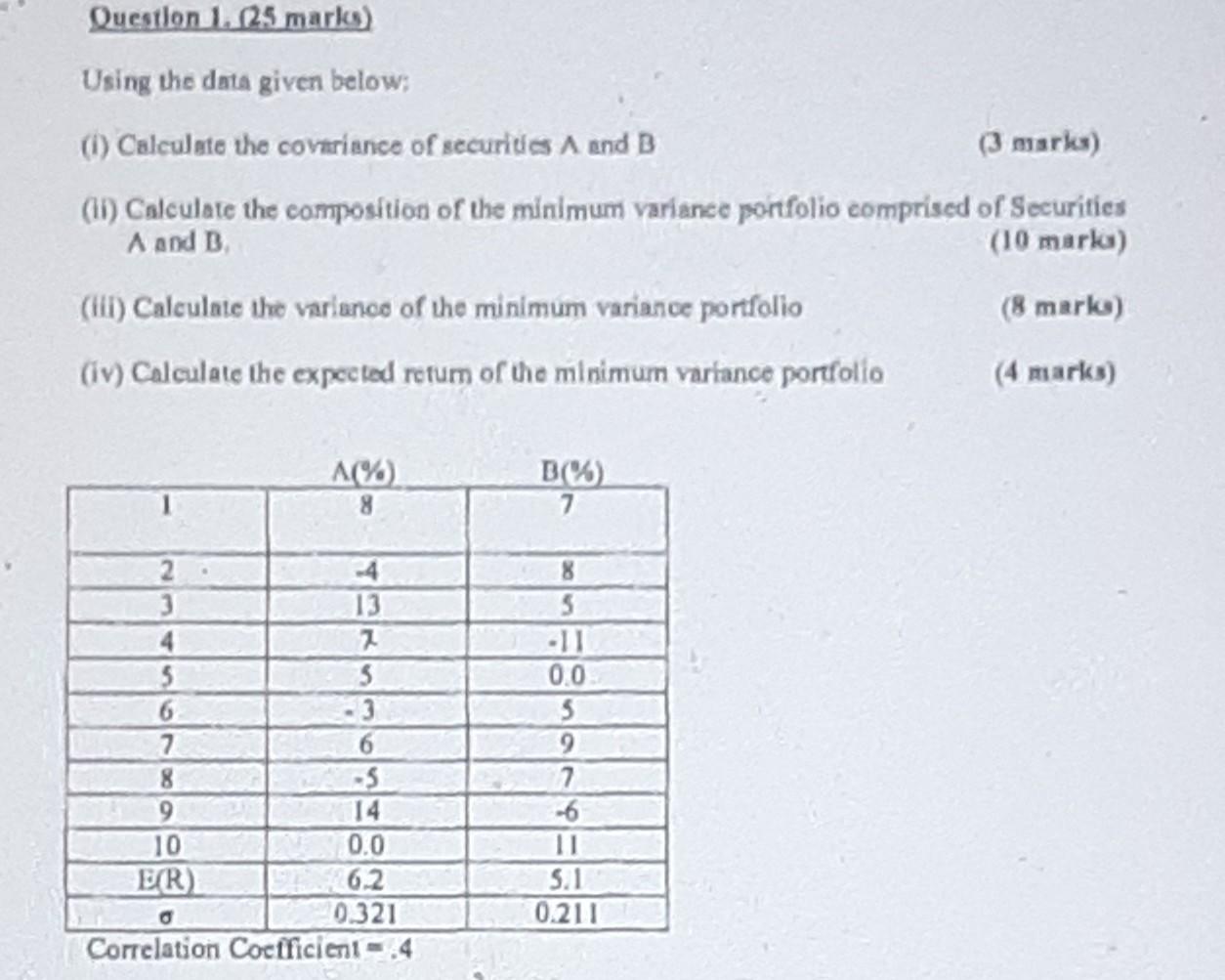

Question: Question 1. 2.5 marks Using the data given below; (i) Calculate the covariance of securities A and B (3 marks) (ii) Calculate the composition of

Question 1. 2.5 marks Using the data given below; (i) Calculate the covariance of securities A and B (3 marks) (ii) Calculate the composition of the minimum variance portfolio comprised of Securifies A and B, (10 marka) (iii) Calculate the variance of the minimum variance portfolio (8 mark) (iv) Calculate the expected retum of the minimum variance portfolio (4 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock