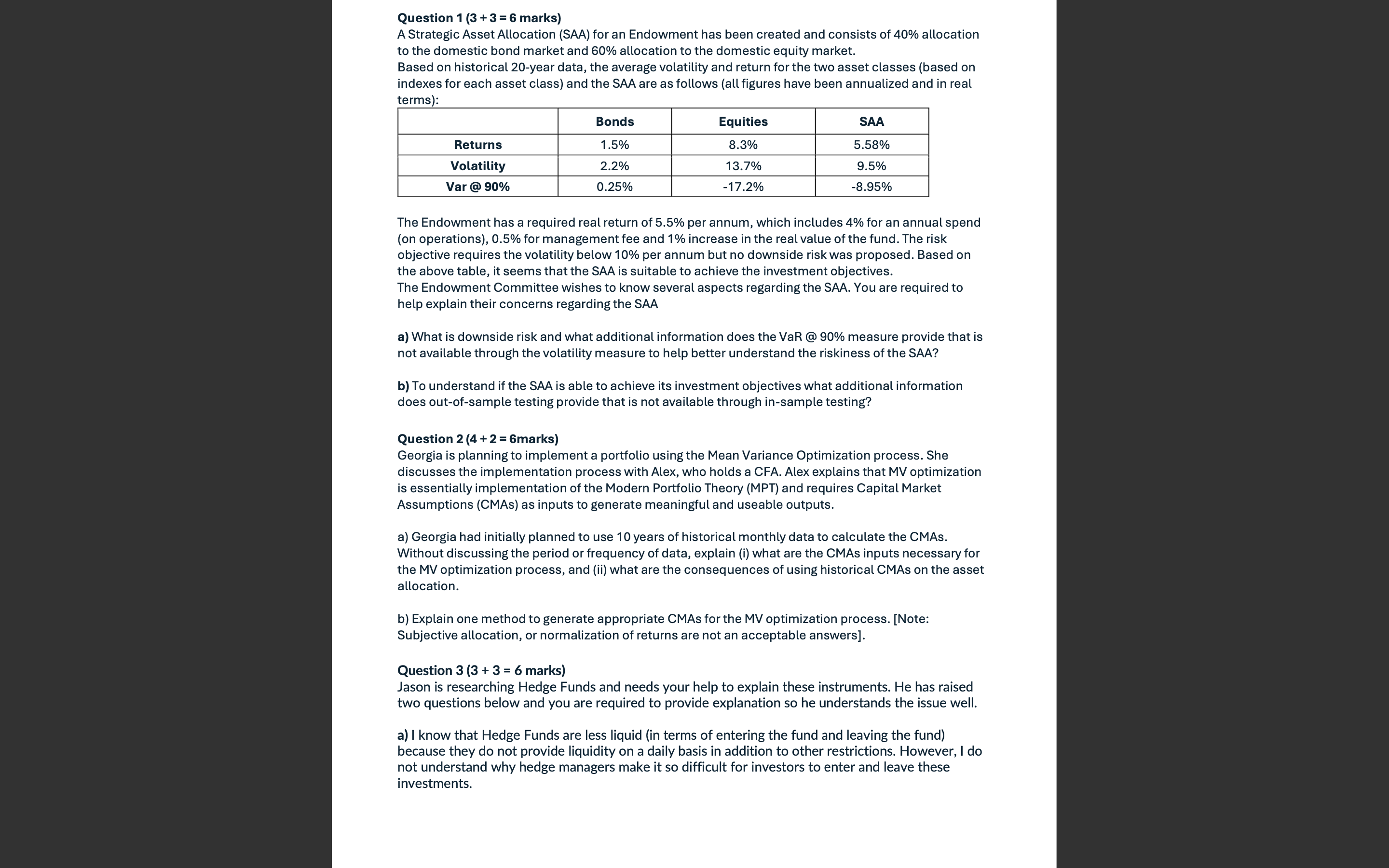

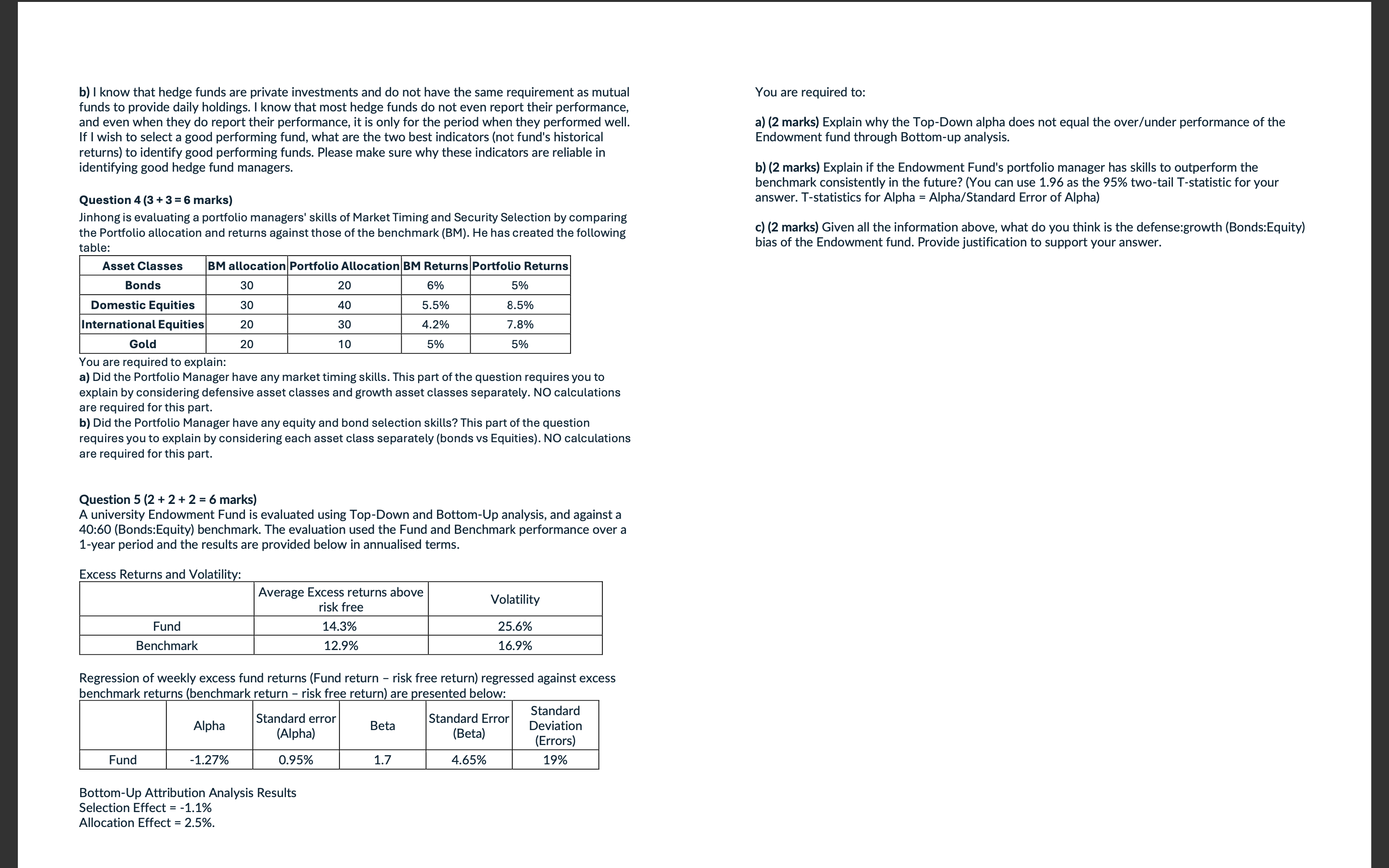

Question: Question 1 (3 +3 = 6 marks) A Strategic Asset Allocation (SAA) for an Endowment has been created and consists of 40% allocation to the

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock