Question: QUESTION 1 (6 points): There is a futures contract calling for delivery of one share of XYZ six months from today. You observe the following

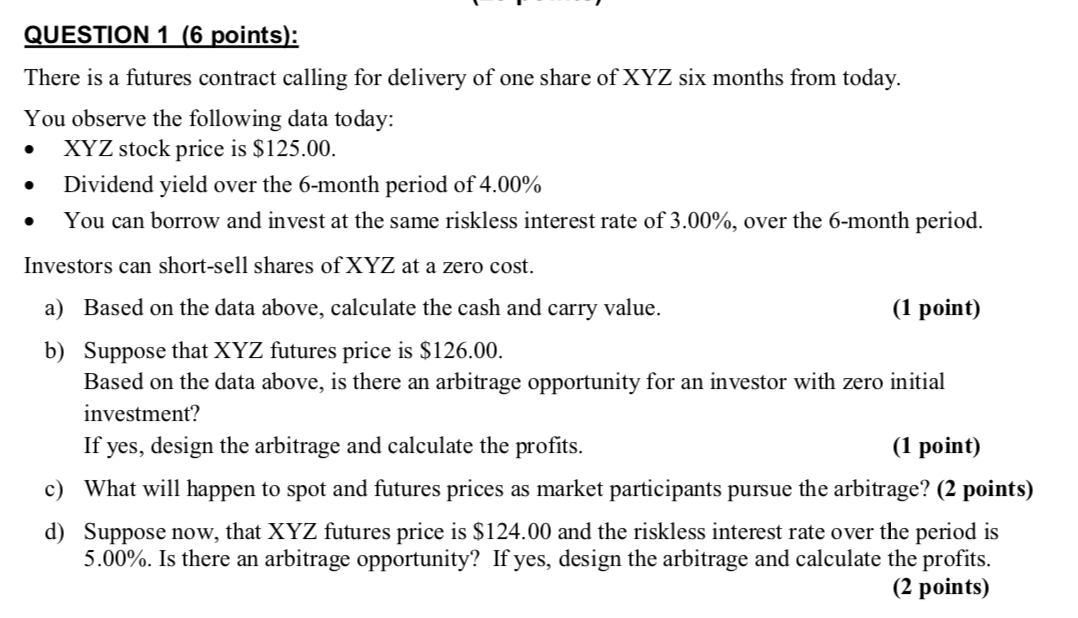

QUESTION 1 (6 points): There is a futures contract calling for delivery of one share of XYZ six months from today. You observe the following data to day: XYZ stock price is $125.00. Dividend yield over the 6-month period of 4.00% You can borrow and invest at the same riskless interest rate of 3.00%, over the 6-month period. Investors can short-sell shares of XYZ at a zero cost. a) Based on the data above, calculate the cash and carry value. (1 point) b) Suppose that XYZ futures price is $126.00. Based on the data above, is there an arbitrage opportunity for an investor with zero initial investment? If yes, design the arbitrage and calculate the profits. (1 point) c) What will happen to spot and futures prices as market participants pursue the arbitrage? (2 points) d) Suppose now, that XYZ futures price is $124.00 and the riskless interest rate over the period is 5.00%. Is there an arbitrage opportunity? If yes, design the arbitrage and calculate the profits. (2 points) QUESTION 1 (6 points): There is a futures contract calling for delivery of one share of XYZ six months from today. You observe the following data to day: XYZ stock price is $125.00. Dividend yield over the 6-month period of 4.00% You can borrow and invest at the same riskless interest rate of 3.00%, over the 6-month period. Investors can short-sell shares of XYZ at a zero cost. a) Based on the data above, calculate the cash and carry value. (1 point) b) Suppose that XYZ futures price is $126.00. Based on the data above, is there an arbitrage opportunity for an investor with zero initial investment? If yes, design the arbitrage and calculate the profits. (1 point) c) What will happen to spot and futures prices as market participants pursue the arbitrage? (2 points) d) Suppose now, that XYZ futures price is $124.00 and the riskless interest rate over the period is 5.00%. Is there an arbitrage opportunity? If yes, design the arbitrage and calculate the profits. (2 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts