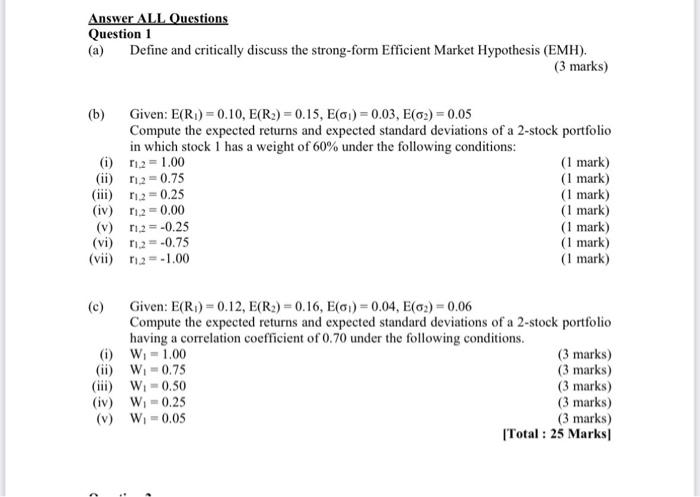

Question: Question 1 a) Define and critically discuss the strong-form Efficient Market Hypothesis (EMH). (3 marks) b) Given: E(R1)=0.10,E(R2)=0.15,E(1)=0.03,E(2)=0.05 Compute the expected returns and expected standard

Question 1 a) Define and critically discuss the strong-form Efficient Market Hypothesis (EMH). (3 marks) b) Given: E(R1)=0.10,E(R2)=0.15,E(1)=0.03,E(2)=0.05 Compute the expected returns and expected standard deviations of a 2-stock portfolio in which stock 1 has a weight of 60% under the following conditions: c) Given: E(R1)=0.12,E(R2)=0.16,E(1)=0.04,E(2)=0.06 Compute the expected returns and expected standard deviations of a 2-stock portfolio having a correlation coefficient of 0.70 under the following conditions. (i) W1=1.00 (ii) W1=0.75 (iii) W1=0.50 (3 marks) (iv) W1=0.25 (3 marks) (v) W1=0.05 (3 marks) (3 marks) [Total : 25 Marks]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts