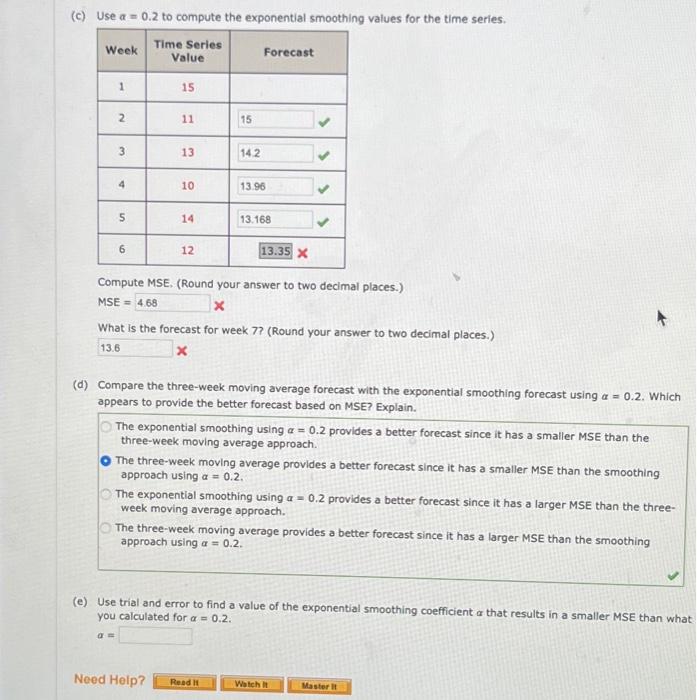

Question: question 1 (c) Use =0.2 to compute the exponential smoothing values for the time series. Compute MSE, (Round your answer to two decimal places.) MSE

(c) Use =0.2 to compute the exponential smoothing values for the time series. Compute MSE, (Round your answer to two decimal places.) MSE = x What is the forecast for week 7? (Round your answer to two decimal places.) x (d) Compare the three-week moving average forecast with the exponential smoothing forecast using =0.2. Which appears to provide the better forecast based on MSE? Explain. The exponential smoothing using =0.2 provides a better forecast since it has a smaller MSE than the three-week moving average approach. The three-week moving average provides a better forecast since it has a smaller MSE than the smoothing approach using =0.2. The exponential smoothing using =0.2 provides a better forecast since it has a larger MSE than the threeweek moving average approach. The three-week moving average provides a better forecast since it has a larger MSE than the smoothing approach using =0.2. (e) Use trial and error to find a value of the exponential smoothing coefficient that results in a smaller MSE than wha you calculated for =0.2. a=

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts