Question: QUESTION 1 (CLO 2) The following draft group financial statements are related to JUC Bhd. JUC Group Statement of financial position as at 31 January

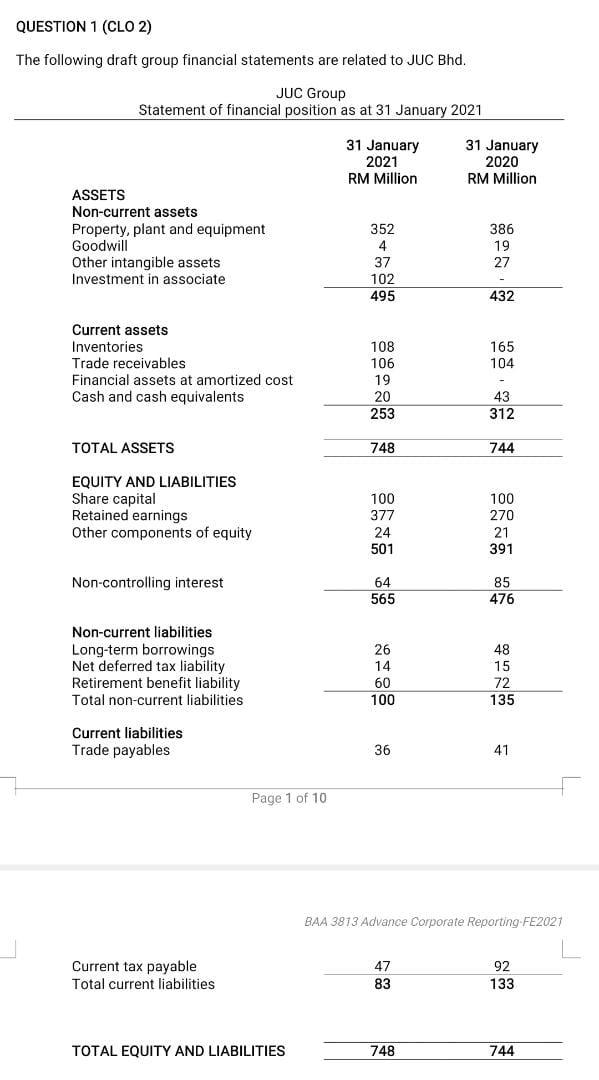

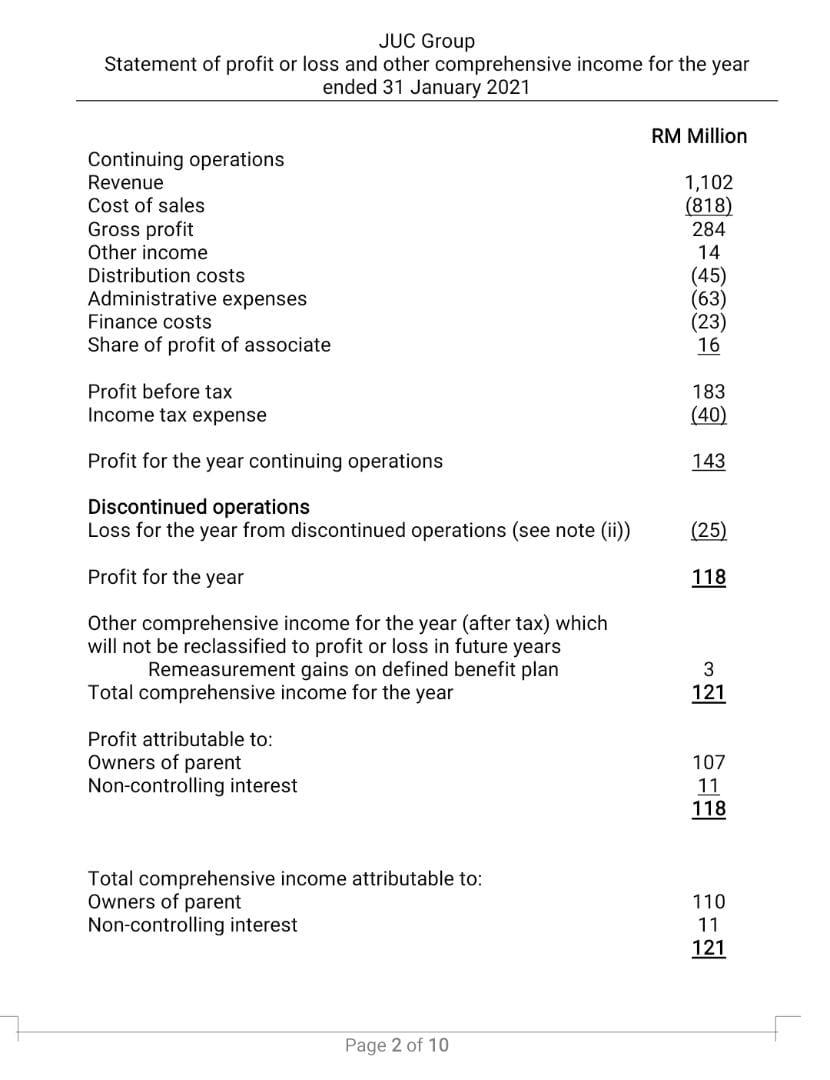

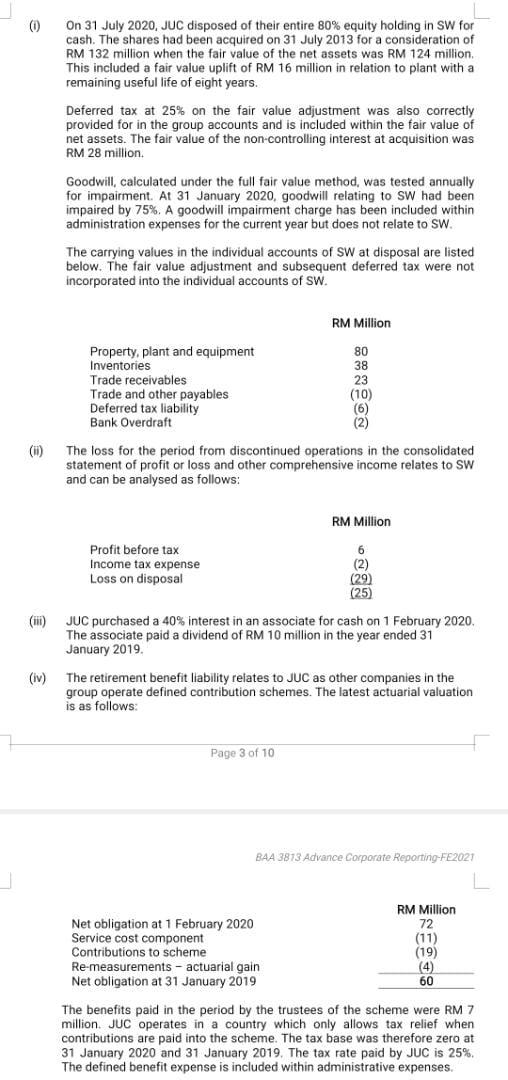

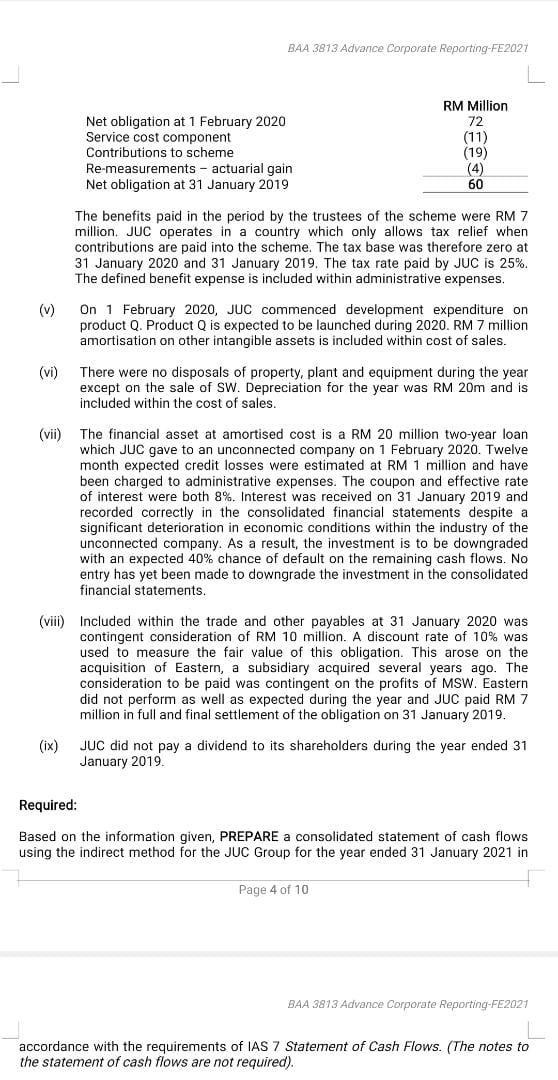

QUESTION 1 (CLO 2) The following draft group financial statements are related to JUC Bhd. JUC Group Statement of financial position as at 31 January 2021 31 January 31 January 2021 2020 RM Million RM Million ASSETS Non-current assets Property, plant and equipment 352 386 Goodwill 4 19 Other intangible assets 37 27 Investment in associate 102 495 432 Current assets Inventories Trade receivables Financial assets at amortized cost Cash and cash equivalents 165 104 108 106 19 20 253 43 312 TOTAL ASSETS 748 744 EQUITY AND LIABILITIES Share capital Retained earnings Other components of equity 100 377 24 501 100 270 21 391 Non-controlling interest 64 565 85 476 Non-current liabilities Long-term borrowings Net deferred tax liability Retirement benefit liability Total non-current liabilities 26 14 60 100 48 15 72 135 Current liabilities Trade payables 36 41 Page 1 of 10 BAA 3873 Advance Corporate Reporting-FE2021 Current tax payable Total current liabilities 47 83 92 133 TOTAL EQUITY AND LIABILITIES 748 744 JUC Group Statement of profit or loss and other comprehensive income for the year ended 31 January 2021 RM Million Continuing operations Revenue Cost of sales Gross profit Other income Distribution costs Administrative expenses Finance costs Share of profit of associate 1,102 (818) 284 14 (45) (63) (23) 16 Profit before tax Income tax expense 183 (40) Profit for the year continuing operations 143 Discontinued operations Loss for the year from discontinued operations (see note (ii) (25) Profit for the year 118 Other comprehensive income for the year after tax) which will not be reclassified to profit or loss in future years Remeasurement gains on defined benefit plan Total comprehensive income for the year 3 121 Profit attributable to: Owners of parent Non-controlling interest 107 11 118 Total comprehensive income attributable to: Owners of parent Non-controlling interest 110 11 121 Page 2 of 10 0 On 31 July 2020, JUC disposed of their entire 80% equity holding in SW for cash. The shares had been acquired on 31 July 2013 for a consideration of RM 132 million when the fair value of the net assets was RM 124 million This included a fair value uplift of RM 16 million in relation to plant with a remaining useful life of eight years. Deferred tax at 25% on the fair value adjustment was also correctly provided for in the group accounts and is included within the fair value of net assets. The fair value of the non-controlling interest at acquisition was RM 28 million Goodwill, calculated under the full fair value method, was tested annually for impairment. At 31 January 2020. goodwill relating to SW had been impaired by 75%. A goodwill impairment charge has been included within administration expenses for the current year but does not relate to SW. The carrying values in the individual accounts of SW at disposal are listed below. The fair value adjustment and subsequent deferred tax were not incorporated into the individual accounts of SW. RM Million Property, plant and equipment Inventories Trade receivables Trade and other payables Deferred tax liability Bank Overdraft 80 38 23 (10) (6) (2) (0) The loss for the period from discontinued operations in the consolidated statement of profit or loss and other comprehensive income relates to SW and can be analysed as follows: RM Million Profit before tax Income tax expense Loss on disposal 6 (2) (29) (25) (ii) JUC purchased a 40% interest in an associate for cash on 1 February 2020, The associate paid a dividend of RM 10 million in the year ended 31 January 2019. (iv) The retirement benefit liability relates to JUC as other companies in the group operate defined contribution schemes. The latest actuarial valuation is as follows: Page 3 of 10 BAA 3813 Advance Corporate Reporting-FE2021 Net obligation at 1 February 2020 Service cost component Contributions to scheme Re-measurements - actuarial gain Net obligation at 31 January 2019 RM Million 72 (11) (19) (4) 60 The benefits paid in the period by the trustees of the scheme were RM 7 million JUC operates in a country which only allows tax relief when contributions are paid into the scheme. The tax base was therefore zero at 31 January 2020 and 31 January 2019. The tax rate paid by JUC is 25% The defined benefit expense is included within administrative expenses. BAA 3813 Advance Corporate Reporting-FE2027 Net obligation at 1 February 2020 Service cost component Contributions to scheme Re-measurements - actuarial gain Net obligation at 31 January 2019 RM Million 72 (11) (19) (4) 60 The benefits paid in the period by the trustees of the scheme were RM 7 million. JUC operates in a country which only allows tax relief when contributions are paid into the scheme. The tax base was therefore zero at 31 January 2020 and 31 January 2019. The tax rate paid by JUC is 25% The defined benefit expense is included within administrative expenses, On 1 February 2020, JUC commenced development expenditure on product Q. Product Q is expected to be launched during 2020. RM 7 million amortisation on other intangible assets is included within cost of sales. (v) (vi) There were no disposals of property, plant and equipment during the year except on the sale of SW. Depreciation for the year was RM 20m and is included within the cost of sales. (vii) The financial asset at amortised cost is a RM 20 million two-year loan which JUC gave to an unconnected company on 1 February 2020. Twelve month expected credit losses were estimated at RM 1 million and have been charged to administrative expenses. The coupon and effective rate of interest were both 8%. Interest was received on 31 January 2019 and recorded correctly in the consolidated financial statements despite a significant deterioration in economic conditions within the industry of the unconnected company. As a result, the investment is to be downgraded an expected 40% chance of default on the remaining cash flows. No entry has yet been made to downgrade the investment in the consolidated financial statements. with an (vii) Included within the trade and other payables at 31 January 2020 was contingent consideration of RM 10 million. A discount rate of 10% was used to measure the fair value of this obligation. This arose on the acquisition of Eastern, a subsidiary acquired several years ago. The consideration to be paid was contingent on the profits of MSW. Eastern did not perform as well as expected during the year and JUC paid RM 7 million in full and final settlement of the obligation on 31 January 2019. (ix) JUC did not pay a dividend to its shareholders during the year ended 31 January 2019 Required: Based on the information given, PREPARE a consolidated statement of cash flows using the indirect method for the JUC Group for the year ended 31 January 2021 in Page 4 of 10 BAA 3813 Advance Corporate Reporting-FE2021 accordance with the requirements of IAS 7 Statement of Cash Flows. (The notes to the statement of cash flows are not required) QUESTION 1 (CLO 2) The following draft group financial statements are related to JUC Bhd. JUC Group Statement of financial position as at 31 January 2021 31 January 31 January 2021 2020 RM Million RM Million ASSETS Non-current assets Property, plant and equipment 352 386 Goodwill 4 19 Other intangible assets 37 27 Investment in associate 102 495 432 Current assets Inventories Trade receivables Financial assets at amortized cost Cash and cash equivalents 165 104 108 106 19 20 253 43 312 TOTAL ASSETS 748 744 EQUITY AND LIABILITIES Share capital Retained earnings Other components of equity 100 377 24 501 100 270 21 391 Non-controlling interest 64 565 85 476 Non-current liabilities Long-term borrowings Net deferred tax liability Retirement benefit liability Total non-current liabilities 26 14 60 100 48 15 72 135 Current liabilities Trade payables 36 41 Page 1 of 10 BAA 3873 Advance Corporate Reporting-FE2021 Current tax payable Total current liabilities 47 83 92 133 TOTAL EQUITY AND LIABILITIES 748 744 JUC Group Statement of profit or loss and other comprehensive income for the year ended 31 January 2021 RM Million Continuing operations Revenue Cost of sales Gross profit Other income Distribution costs Administrative expenses Finance costs Share of profit of associate 1,102 (818) 284 14 (45) (63) (23) 16 Profit before tax Income tax expense 183 (40) Profit for the year continuing operations 143 Discontinued operations Loss for the year from discontinued operations (see note (ii) (25) Profit for the year 118 Other comprehensive income for the year after tax) which will not be reclassified to profit or loss in future years Remeasurement gains on defined benefit plan Total comprehensive income for the year 3 121 Profit attributable to: Owners of parent Non-controlling interest 107 11 118 Total comprehensive income attributable to: Owners of parent Non-controlling interest 110 11 121 Page 2 of 10 0 On 31 July 2020, JUC disposed of their entire 80% equity holding in SW for cash. The shares had been acquired on 31 July 2013 for a consideration of RM 132 million when the fair value of the net assets was RM 124 million This included a fair value uplift of RM 16 million in relation to plant with a remaining useful life of eight years. Deferred tax at 25% on the fair value adjustment was also correctly provided for in the group accounts and is included within the fair value of net assets. The fair value of the non-controlling interest at acquisition was RM 28 million Goodwill, calculated under the full fair value method, was tested annually for impairment. At 31 January 2020. goodwill relating to SW had been impaired by 75%. A goodwill impairment charge has been included within administration expenses for the current year but does not relate to SW. The carrying values in the individual accounts of SW at disposal are listed below. The fair value adjustment and subsequent deferred tax were not incorporated into the individual accounts of SW. RM Million Property, plant and equipment Inventories Trade receivables Trade and other payables Deferred tax liability Bank Overdraft 80 38 23 (10) (6) (2) (0) The loss for the period from discontinued operations in the consolidated statement of profit or loss and other comprehensive income relates to SW and can be analysed as follows: RM Million Profit before tax Income tax expense Loss on disposal 6 (2) (29) (25) (ii) JUC purchased a 40% interest in an associate for cash on 1 February 2020, The associate paid a dividend of RM 10 million in the year ended 31 January 2019. (iv) The retirement benefit liability relates to JUC as other companies in the group operate defined contribution schemes. The latest actuarial valuation is as follows: Page 3 of 10 BAA 3813 Advance Corporate Reporting-FE2021 Net obligation at 1 February 2020 Service cost component Contributions to scheme Re-measurements - actuarial gain Net obligation at 31 January 2019 RM Million 72 (11) (19) (4) 60 The benefits paid in the period by the trustees of the scheme were RM 7 million JUC operates in a country which only allows tax relief when contributions are paid into the scheme. The tax base was therefore zero at 31 January 2020 and 31 January 2019. The tax rate paid by JUC is 25% The defined benefit expense is included within administrative expenses. BAA 3813 Advance Corporate Reporting-FE2027 Net obligation at 1 February 2020 Service cost component Contributions to scheme Re-measurements - actuarial gain Net obligation at 31 January 2019 RM Million 72 (11) (19) (4) 60 The benefits paid in the period by the trustees of the scheme were RM 7 million. JUC operates in a country which only allows tax relief when contributions are paid into the scheme. The tax base was therefore zero at 31 January 2020 and 31 January 2019. The tax rate paid by JUC is 25% The defined benefit expense is included within administrative expenses, On 1 February 2020, JUC commenced development expenditure on product Q. Product Q is expected to be launched during 2020. RM 7 million amortisation on other intangible assets is included within cost of sales. (v) (vi) There were no disposals of property, plant and equipment during the year except on the sale of SW. Depreciation for the year was RM 20m and is included within the cost of sales. (vii) The financial asset at amortised cost is a RM 20 million two-year loan which JUC gave to an unconnected company on 1 February 2020. Twelve month expected credit losses were estimated at RM 1 million and have been charged to administrative expenses. The coupon and effective rate of interest were both 8%. Interest was received on 31 January 2019 and recorded correctly in the consolidated financial statements despite a significant deterioration in economic conditions within the industry of the unconnected company. As a result, the investment is to be downgraded an expected 40% chance of default on the remaining cash flows. No entry has yet been made to downgrade the investment in the consolidated financial statements. with an (vii) Included within the trade and other payables at 31 January 2020 was contingent consideration of RM 10 million. A discount rate of 10% was used to measure the fair value of this obligation. This arose on the acquisition of Eastern, a subsidiary acquired several years ago. The consideration to be paid was contingent on the profits of MSW. Eastern did not perform as well as expected during the year and JUC paid RM 7 million in full and final settlement of the obligation on 31 January 2019. (ix) JUC did not pay a dividend to its shareholders during the year ended 31 January 2019 Required: Based on the information given, PREPARE a consolidated statement of cash flows using the indirect method for the JUC Group for the year ended 31 January 2021 in Page 4 of 10 BAA 3813 Advance Corporate Reporting-FE2021 accordance with the requirements of IAS 7 Statement of Cash Flows. (The notes to the statement of cash flows are not required)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts