Question: Question 1 - Define the required behaviour and outline the type of behaviour that organisation need ? CASES FOR ANALYSIS The following cases, which reflect

Question 1 - Define the required behaviour and outline the type of behaviour that organisation need ?

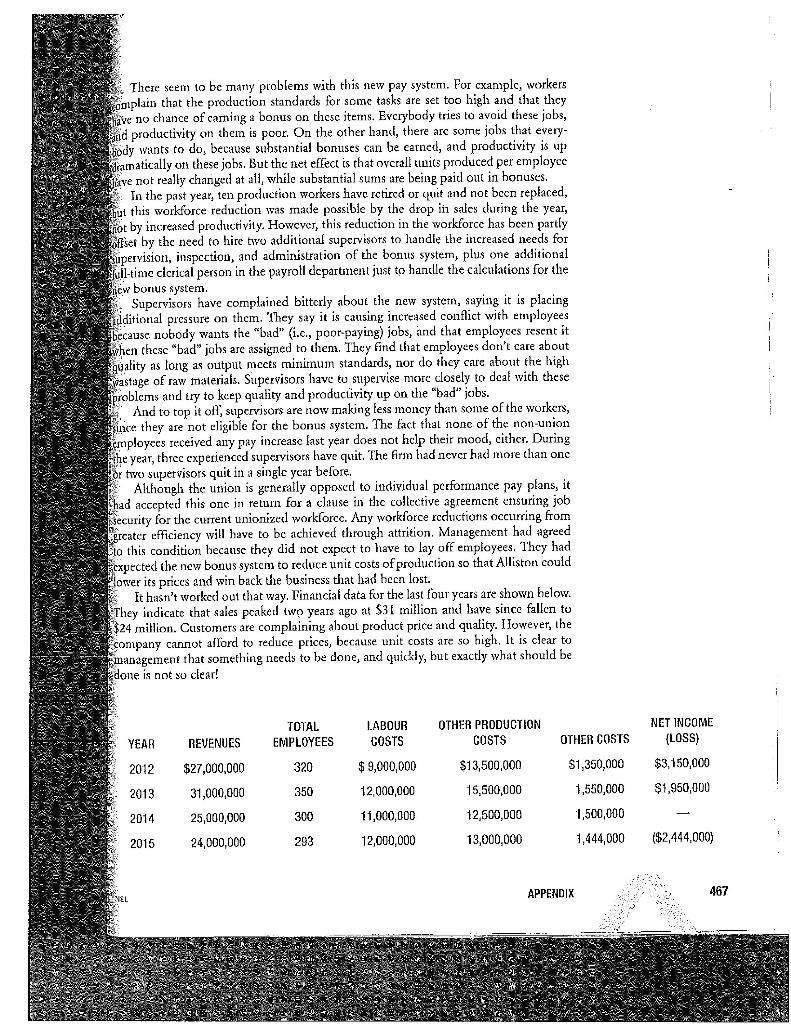

CASES FOR ANALYSIS The following cases, which reflect a range of compensation issues and organizational types, can be used in a variety of ways. They are presented without any questions attached to them to allow instructors flexibility in their use. They can be used in conjunction with the end-of-chapter case questions to illustrate compensation is sucs retevant to that chap het and to provide opportunities for applying compensation concepts. They can also be ised as a basis for major term assignments or group projects. Some arc short cuough to be used as cxam cases. And, of course, they can serve as a basis for lively class discussions of many important compensation issues. ACHTYMICHUK MACHINE WORKS At the Achtypichulachine Works, cach department horeer two clean-up empley Pecs who clean around the machines and also take care of the wash.coms, hallways, and Father areas. The cleaning job has le lowest status of thy in the plant although the bay Its fairly good becage the plant has had difficulty gesing enough clans. The pay for cleaners is based oa flat hourly rated provides galy mandatory fences. There e 20 leaners in ati. They port to the supervisors of the delegits in hich they works out the supervisors are very dissatisfied with them. A conigol com- plaint is that as soon as a cleaner knows what is bected on the job and learned to do it night, he or she quits. Moreover, the cleanekega trequently absent and often come late. ALLISTON INSTRUMENTS Alliston Instruments is a manufacturer of specialty medical instruments located in south- ei Ontario, Manufacturing involves two types of processes. First, individual workers produce the components for the medical instruments in latches of various sizes, using variety of machine tools and equipment. Then other workers assemble the compo nelies into finished products. Assembly is done scquentially , with each product passing through four to six workstations isefore completion. The quality of the products, which crucial, depends on both the quality of the component parts that are produced and the quality of the assembly process. It is late January 2016 the financial statements for 2015 have just been released. They are grim. For the first time in the company's 50-year history, the firm has shown a loss. The company's chief executive officer believes a lot of this has to do with produc- ton problerus. The 2015 production reports indicate that although the number of units produced per employec showed a slight increase last year, the number of defective units Sitaclied an all-time high. In addition, there was a high rate of wastage of raw materials and Folhet supplies. Although total sales (and therefore total production) are down from the Previous year, total labour costs are up. As a result, costs per unit are at an all-time high. 465 Because you are an expert in human resources management, the CEO has asked for your help. As background for your work, the CEO briefs you on industry condi- tions. Until two years ago, the firm had enjoyed increasing sales over many years. It had also had increasing profits, with a record profit of over $3 million in 2012. I lowever, in the last two years, the medical instruments industry has become more competitive. High-quality medical instruments are now being produced by several Asiar frns, two of which entered the Canadian market in 2013. (Previously, the main competiturs in the Canadian market were U.S. and European firms, but they are not much of a problem because their products are very high priced.) Because of low labour costs, the Asian firms are able to price their products attractively; however, buycts initially held back, concerned about potential quality problems. So for a while, it appeared as if Alliston's customers (mainly hospitals and health clinics) would remain loyal, even though they were themselves under pressure to cut costs, due to budget cuts. But in late 2013, an Asian competitor made a major salcs push by slashing prices, and this cut dramatically into Alliston's 2014 salcs. In mid-2014, Alliston laid off 50 employees. Although the firm had laid off employees from time to time in the past during production lulls, this was the largest layoff in company history "To make up for the loss of sales, Alliston added a number of new products to its line. Over er the years, the company had tended to stick with the same set of products, although new products were being put into use in the hospitals.) While some of these new products sold well, they didn't really make money, because production costs were higher due to the need for new equipment and extensive employee training. Moreover, most employees preferred to work on the old products, so supervisors had to use a lot of pressure to get them 10 work on the new products. Alliston's 250 production workers have been unionized since the 1960s. In 2012, they staged a short but bitter strike. Because product demand was so high, the company diel not want a long work stoppage, and the union was able to win significant wage increases for 2013 and 2014 (a two-year contract was signed). Since then, union-management relations, never very good, have been quite strained. Relations between supervisors and workers are no better. Supervisors complain about lazy workers who don't care if they du a good job or not, and workers complain about overbeating supervisors who allocate work unfairly and all their time watching and harassing employees. Interestingly, the employce turnover rate is tow at Alliston, Pay at the firm is above average, and the benefits package, which increases with scriority, is very good, com- prising about 25 percent of total compensation. Comparable alternative employment opportunities in the area are quite scarce. In late 2014, in an effort to increuse efficiency, the firm persuaded the union to acceplan incentive system in which employees would reccive, in addition to their hourly wages, a bonus bascd on individual output, rather than an increase in base pay for 2015. A standard per-hour production rate for each item or assembly operation was cstablished based on estimated 2014 production levels. (However, because the firm had never kept detailed records, these standards were simply based on the estimates of supervisors.) Under the new system, if production per hour for a particular itcm cxceeds 2014 levels, the employee receives a fixed sum for each piece produced over that levet, in adidi- tion to the normal hourly pay. Of course, employees co tiot receive a bonus for items that arc not of satisfactory quality, and supervisors arc cxpected to deduct these from the e e employee totals. However, there are no sct standarts for quality, and each supervisor scems to sct different standards, 466 APPENDIX NEL i There seem to be many problems with this new pay system. For example, workers coolplain that the production standards for some tasks are set too high and that they have no chance of carning a bonus on thesc items. Everybody tries to avoid these jobs, and productivity on them is poor. On the other hand, there are some jobs that every- kody wants to do, because substantial bonuses can be carned, and productivity is up Framatically with these jobs. But the net effect is that overall tunits produced per employee Jave not really changed at all , while substantial sums are being pail out in bonuses. In the past year, ten production workers have retired or quit and not been replaced, Lut this workforce reduction was made possible by the drop in sales during the year, iot by increased productivity. However, this reduction in the workforce has been partly offset by the need to hire two additional supervisors to handle the increased needs for Supervision, inspection, and administration of the bonus system, plus one additional full-timc clcrical person in the payroll departament just to handle the calculations for the Sacw bonus system Supervisors have complained bitterly about the new system, saying it is placing additional pressure on them. They say it is causing increased conflict with employees because nobody wants the "bad" (1.c., poor paying) jobs, and that employees resent it uwhen chcsc "bad" jobs are assigned to them. They find that employees don't care about quality as long as output meets minimum standards, nor do they care about the high wastage of raw materials. tu supervise more closely to deal with these problems and try to keep quality and producvity up on the "bad" jobs. to top it off, supervisors are now making tess money than some of the workers, Hrince they are not eligible for the bonus system. The fact that none of the non-union employees received any pay increasc last year does not help their mood, cither. During the year, three experienced supervisors have quit. The firm had never had more than one for two supervisors quit in a single year before. Although the union is generally opposed to individual pcefomance pay plans, it had accepted this one in return for a clause in the collective agreement ensuring job security for the current unionizel workforce. Any workforce recluctions occurring from to be achieved through attrition Management had agreed Lia this condition because they did not expect to have to lay off employees. They had expected the new bonus system to reduce unit costs of production so that Alliston could lower its prices and win back the business that had heen n lost. It hasn't worked out that way. I'inancial data for the last four ycars are shown helow. They indicate that sales peaked two years ago at $36 million and have since fallen tu 324 million. Customers are complaining about product price and quality. Ilowever, the company cannot afford to reduce prices, because unit costs are so high. It is clear to management that something needs to be done, and quickly, but exactly what should be done is not so clear! And i LABOUR COSTS OTHER PRODUCTION COSTS NET INCOME {LOSS) YEAR REVENUES OTHER COSTS TOTAL EMPLOYEES 320 2012 $27,000,000 $ 9,000,000 $13,500,000 $1,350,000 $3,150,000 2013 31,000,000 350 12,000,000 15,500,000 $1,950,000 1,550,000 1,500,000 2014 25,000,000 300 11,000,000 12,500,000 2015 24,000,000 293 12,000,000 13,000,000 1,444,000 ($2,444,000) APPENDIX 467Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock