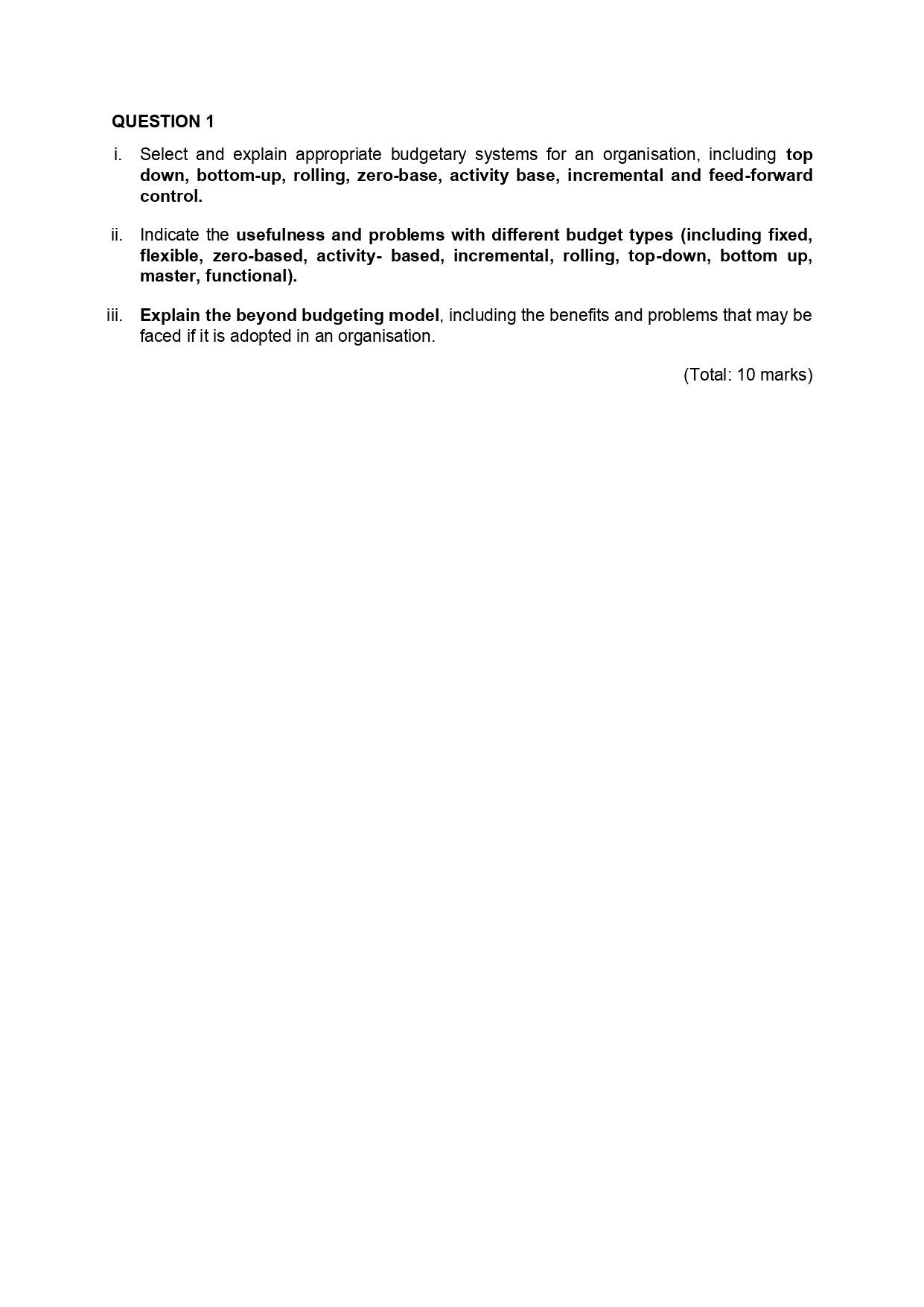

Question: QUESTION 1 i. Select and explain appropriate budgetary systems for an organisation, including top down, bottom-up, rolling, zero-base, activity base, incremental and feed-forward control. Indicate

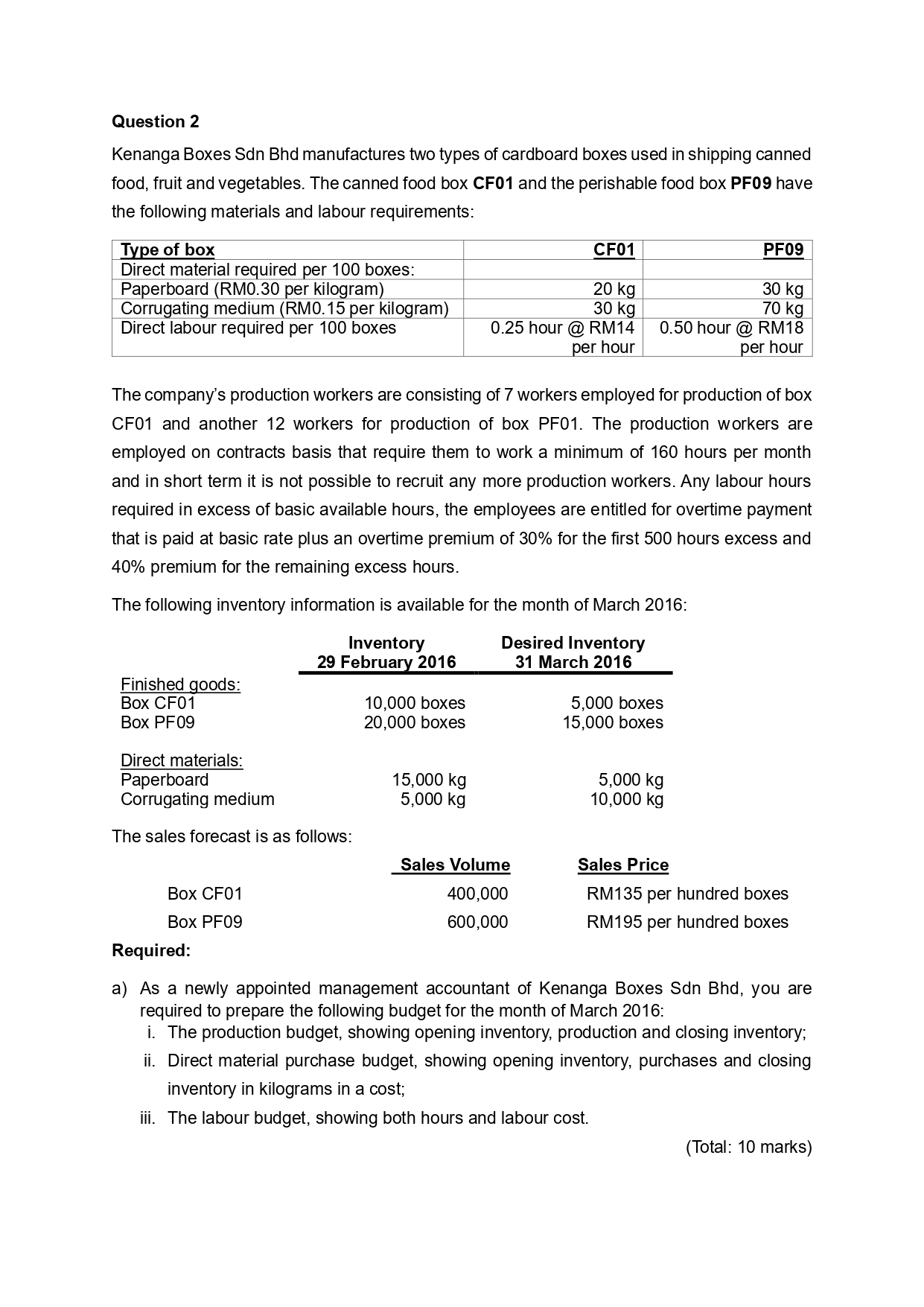

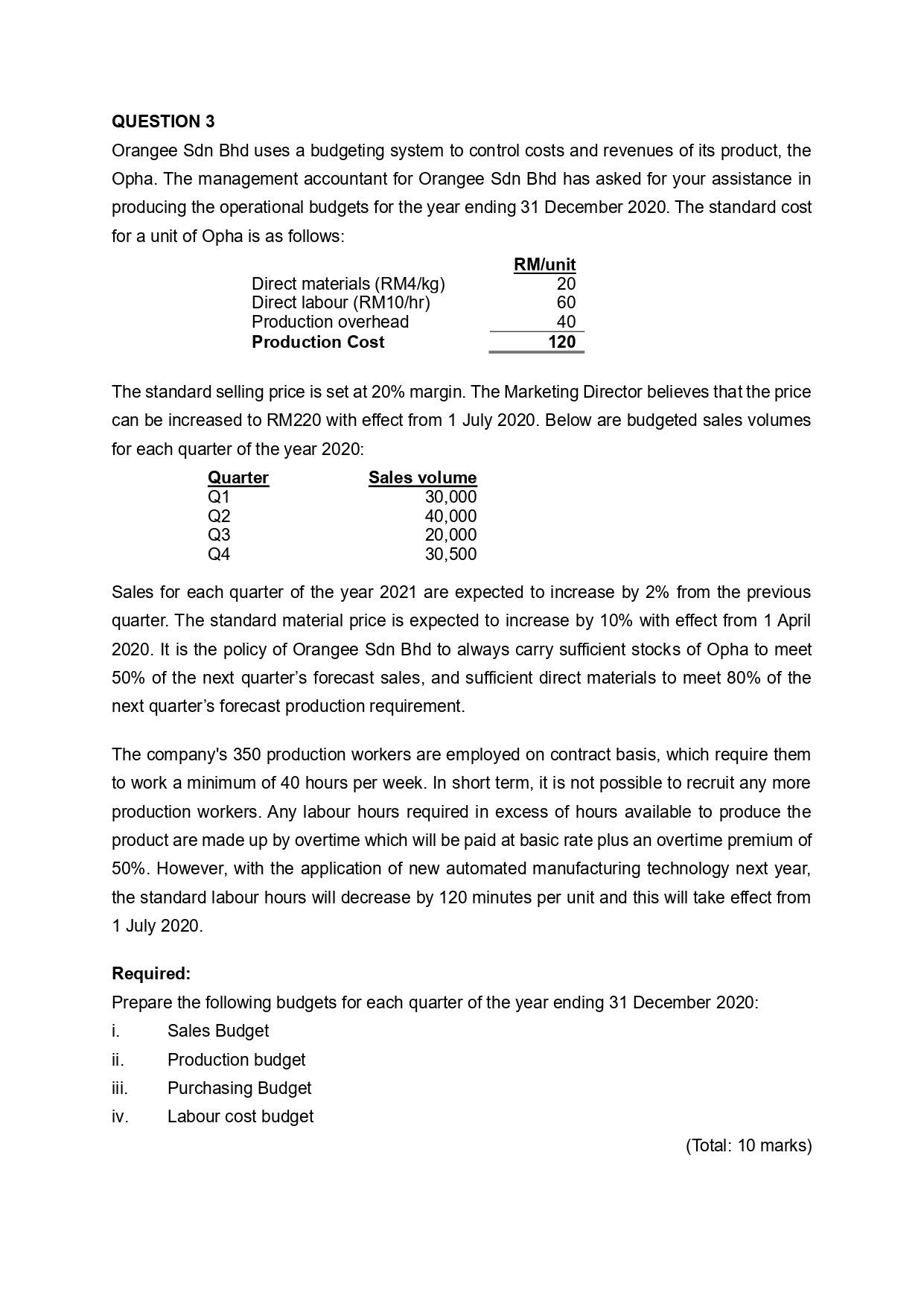

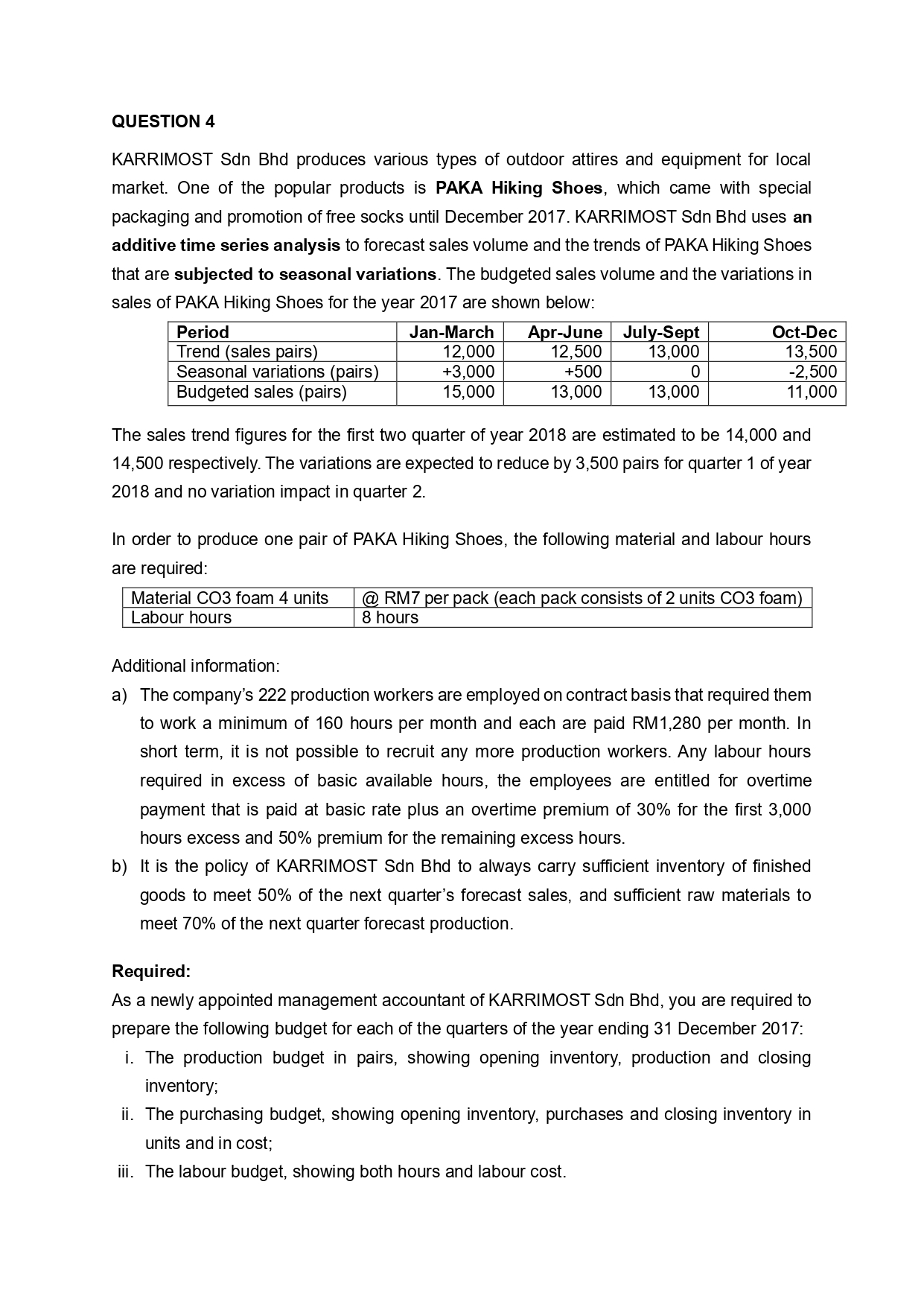

QUESTION 1 i. Select and explain appropriate budgetary systems for an organisation, including top down, bottom-up, rolling, zero-base, activity base, incremental and feed-forward control. Indicate the usefulness and problems with different budget types (including fixed, flexible, zero-based, activity- based, incremental, rolling, top-down, bottom up, master, functional). iii. Explain the beyond budgeting model, including the benefits and problems that may be faced if it is adopted in an organisation. (Total: 10 marks)Question 2 Kenanga Boxes Sdn Bhd manufactures two types of cardboard boxes used in shipping canned food, fruit and vegetables. The canned food box CF01 and the perishable food box PF09 have the following materials and labour requirements: Type of box CF01 PF09 Direct material required per 100 boxes: . Paperboard (RMO.30 per kilogram) . 20 kg 30 kg Corrugating medium (RMO.15 per kilogram) _ 30 kg 70 kg _ Direct labour required per 100 boxes 0.25 hour @ RM14 0.50 hour @ RM18 per hour per hour The company's production workers are consisting of 7 workers employed for production of box CF01 and another 12 workers for production of box PF01. The production workers are employed on contracts basis that require them to work a minimum of 160 hours per month and in short term it is not possible to recruit any more production workers. Any labour hours required in excess of basic available hours, the employees are entitled for overtime payment that is paid at basic rate plus an overtime premium of 30% for the rst 500 hours excess and 40% premium for the remaining excess hours. The following inventory information is available for the month of March 2016: Inventory Desired Inventory 29 Februa 2016 31 March 2016 Finished goods: Box CF01 10,000 boxes 5,000 boxes Box PF09 20,000 boxes 15,000 boxes Direct materials: Paperboard 15,000 kg 5,000 kg Corrugating medium 5,000 kg 10,000 kg The sales forecast is as follows: Sales Volume Sales Price Box CF01 400,000 RM135 per hundred boxes Box PF09 600,000 RM195 per hundred boxes Required: a) As a newly appointed management accountant of Kenanga Boxes Sdn Bhd, you are required to prepare the following budget for the month of March 2016: i. The production budget, showing opening inventory, production and closing inventory; ii. Direct material purchase budget, showing opening inventory, purchases and closing inventory in kilograms in a cost; iii. The labour budget, showing both hours and labour cost. (Total: 10 marks) QUESTION 3 Orangee Sdn Bhd uses a budgeting system to control costs and revenues of its product, the Opha. The management accountant for Orangee Sdn Bhd has asked for your assistance in producing the operational budgets for the year ending 31 December 2020. The standard cost for a unit of Opha is as follows: RMlunit Direct materials (RM4fkg) 20 Direct labour (RM10lhr) 60 Production overhead 40 Production Cost 120 The standard selling price is set at 20% margin. The Marketing Director believes that the price can be increased to RM220 with effect from 1 July 2020. Below are budgeted sales volumes for each quarter of the year 2020: Quarter Sales volume Q1 30,000 02 40,000 Q3 20,000 Q4 30,500 Sales for each quarter of the year 2021 are expected to increase by 2% from the previous quarter. The standard material price is expected to increase by 10% with effect from 1 April 2020. It is the policy of Orangee Sdn Bhd to always carry sufcient stocks of Opha to meet 50% of the next quarter's forecast sales, and sufcient direct materials to meet 80% of the next quarter's forecast production requirement. The company's 350 production workers are employed on contract basis, which require them to work a minimum of 40 hours per week. In short term, it is not possible to recruit any more production workers. Any labour hours required in excess of hours available to produce the product are made up by overtime which will be paid at basic rate plus an overtime premium of 50%. However, with the application of new automated manufacturing technology next year, the standard labour hours will decrease by 120 minutes per unit and this will take effect from 1 July 2020. Required: Prepare the following budgets for each quarter of the year ending 31 December 2020: i. Sales Budget ii. Production budget iii. Purchasing Budget iv. Labour cost budget (Total: 10 marks) QUESTION 4 KARRIMOST Sdn Bhd produces various types of outdoor attires and equipment for local market. One of the popular products is PAKA Hiking Shoes, which came with special packaging and promotion of free socks until December 2017. KARRI MOST Sdn Bhd uses an additive time series analysis to forecast sales volume and the trends of PAKA Hiking Shoes that are subjected to seasonal variations. The budgeted sales volume and the variations in sales of PAKA Hiking Shoes for the year 2017 are shown below: Period Jan-March Apr-June July-Sept Oct-Dec Trend (sales pairs) | 12,000 12,500 13,000 13,500 Seasonal variations (pairs) I +3000 +500 0 -2,500 Budgeted sales (pairs) | 15,000 13,000 13,000 11,000 The sales trend figures for the rst two quarter of year 2018 are estimated to be 14,000 and 14,500 respectively. The variations are expected to reduce by 3,500 pairs for quarter 1 of year 2018 and no variation impact in quarter 2. In order to produce one pair of PAKA Hiking Shoes, the following material and labour hours are required: Material CO3 foam 4 units @ RM7 per pack (each pack consists of 2 units CO3 foamL Labour hours 8 hours Additional information: a) The company's 222 production workers are employed on contract basis that required them to work a minimum of 160 hours per month and each are paid RM1,280 per month. In short term, it is not possible to recruit any more production workers. Any labour hours required in excess of basic available hours, the employees are entitled for overtime payment that is paid at basic rate plus an overtime premium of 30% for the rst 3,000 hours excess and 50% premium for the remaining excess hours. b) It is the policy of KARRIMOST Sdn Bhd to always carry sufcient inventory of nished goods to meet 50% of the next quarter's forecast sales, and sufcient raw materials to meet 70% of the next quarter forecast production. Required: As a newly appointed management accountant of KARRIMOST Sdn Bhd, you are required to prepare the following budget for each of the quarters of the year ending 31 December 2017: i. The production budget in pairs, showing opening inventory, production and closing inventory; ii. The purchasing budget, showing opening inventory, purchases and closing inventory in units and in cost; iii. The labour budget, showing both hours and labour cost. (Total: 10 marks)QUESTION 5 Nine West Sdn Bhd produces intricate component parts for local markets. The divisional manager is recently concerned about a lack of coordination between purchasing and production personnel and believes that a monthly budgeting system with time series analysis would be better than the present system. The manager of Nine West Division has decided to develop budget information for the third quarter of the current year as a trial before the budget system is implemented for the entire scal year. In response to the manager's request for data that could be used to develop budget information, the controller of Nine west Division accumulated the following data: Sales The actual sales through June 30, 2015, of the current year, are given below. April (actual) 3,500 May (actual) 3,800 June (actual) 5,000 The sales of component parts are subjected to seasonal variations which are shown below: April May June July August September October +500 -200 l 0 +400 -300 l 0 l -600 Direct Material Data regarding the materials used in the component are shown in the following table. The desired monthly ending inventory for the direct materials isto have sufcient materials on hand to provide for 50% of the current month's production needs. Direct Units of materials Cost per unit of Inventory level Material per component material (RM) 30!6!2015 MAT 101 0.6 kg 5.00 1836 kg Direct Labour Each component must pass through two processes to be completedData regarding the direct labour are as follows: Process Hours per nished Cost per direct labour hour component (RM) Assembly 2 5.50 Finishing 0.8 6.00 Finished Goods (component parts) inventory The desired monthly ending inventory is 80 percent of the next month's estimated sales. Required: a. Calculate the seasonally adjusted sales volume for each month of the second quarter of the current year. b. Calculate the forecast sales volume for the each month of the third quarter for the current year assuming the trend keep on continue. c. Prepare Production budget and Material Purchase budget for each month of the third quarter of the current year. cl. Prepare labour cost budget for the third quarter of the current year (in total only) (Total: 10 marks)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!