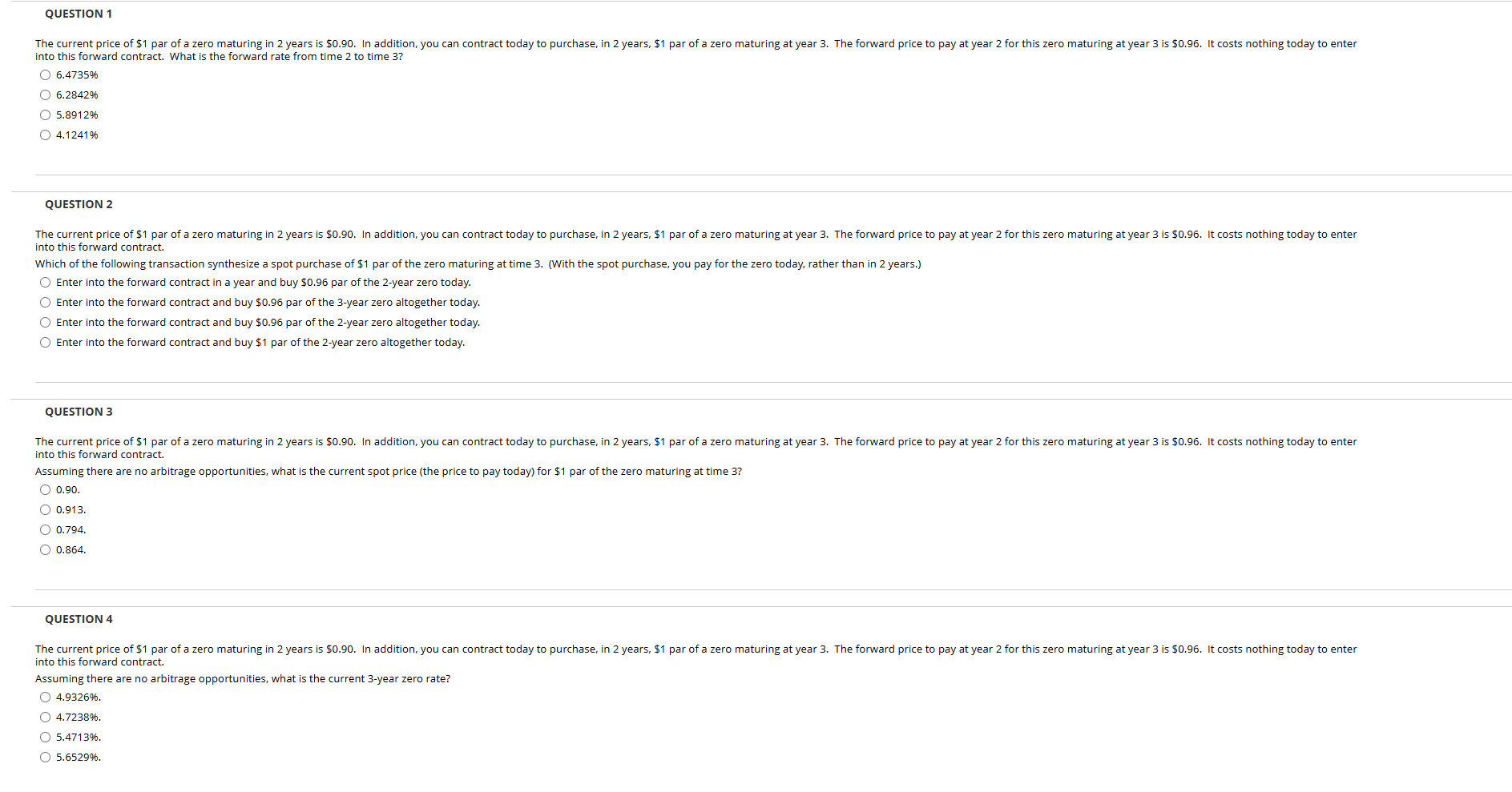

Question: QUESTION 1 into this forward contract. What is the forward rate from time 2 to time 3 ? ( 6 . 4 7 3

QUESTION into this forward contract. What is the forward rate from time to time QUESTION into this forward contract. Which of the following transaction synthesize a spot purchase of $ par of the zero maturing at time With the spot purchase, you pay for the zero today, rather than in years. Enter into the forward contract in a year and buy $ par of the year zero today.Enter into the forward contract and buy $ par of the year zero altogether today. Enter into the forward contract and buy $ par of the year zero altogether today. Enter into the forward contract and buy $ par of the year zero altogether today. QUESTION into this forward contract. Assuming there are no arbitrage opportunities, what is the current spot price the price to pay today for $ par of the zero maturing at time checkmark QUESTION into this forward contract. Assuming there are no arbitrage opportunities, what is the current year zero rate? smile

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock