Question: Question 1. Many countries have used interest rate increases to protect their currencies for many years. What are the pros and cons of using this

Question 1.

Many countries have used interest rate increases to protect their currencies for many years. What are the pros and cons of using this strategy?

Question 2.

In the case of Iceland, the country was able to sustain a large current account deficit for several years, and at the same time have ever-rising interest rates and a stronger and stronger currency. Then one day, it all changed. How does that happen?

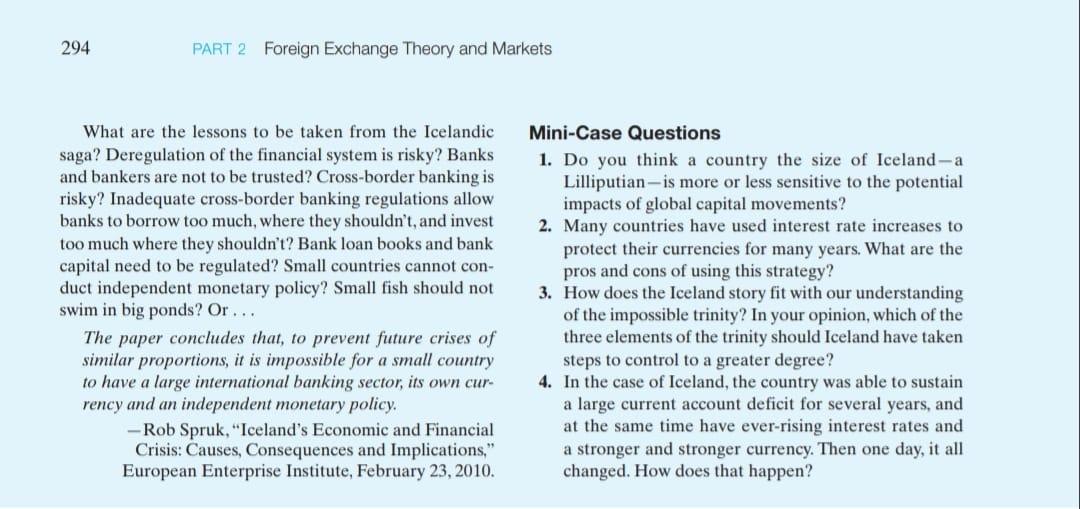

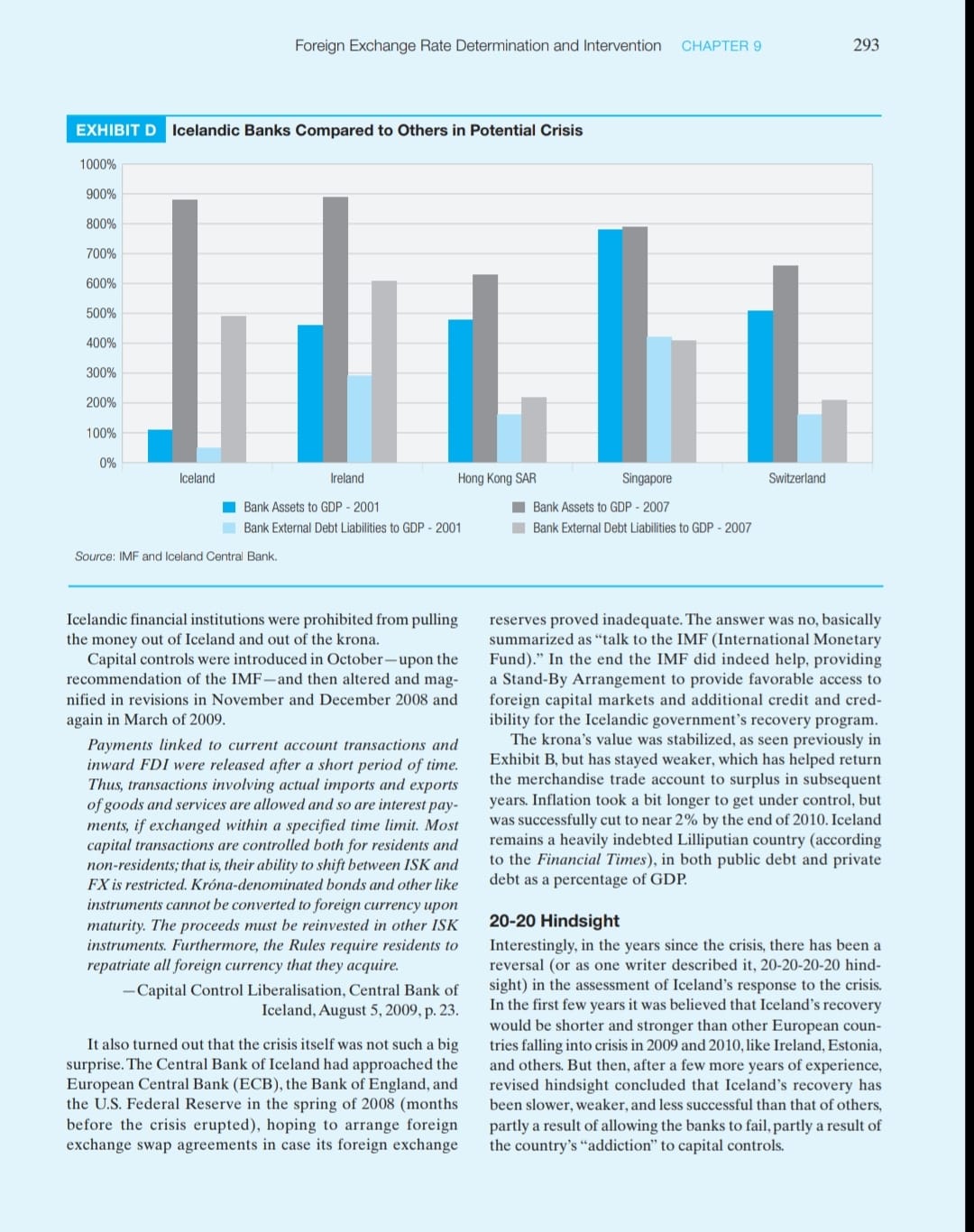

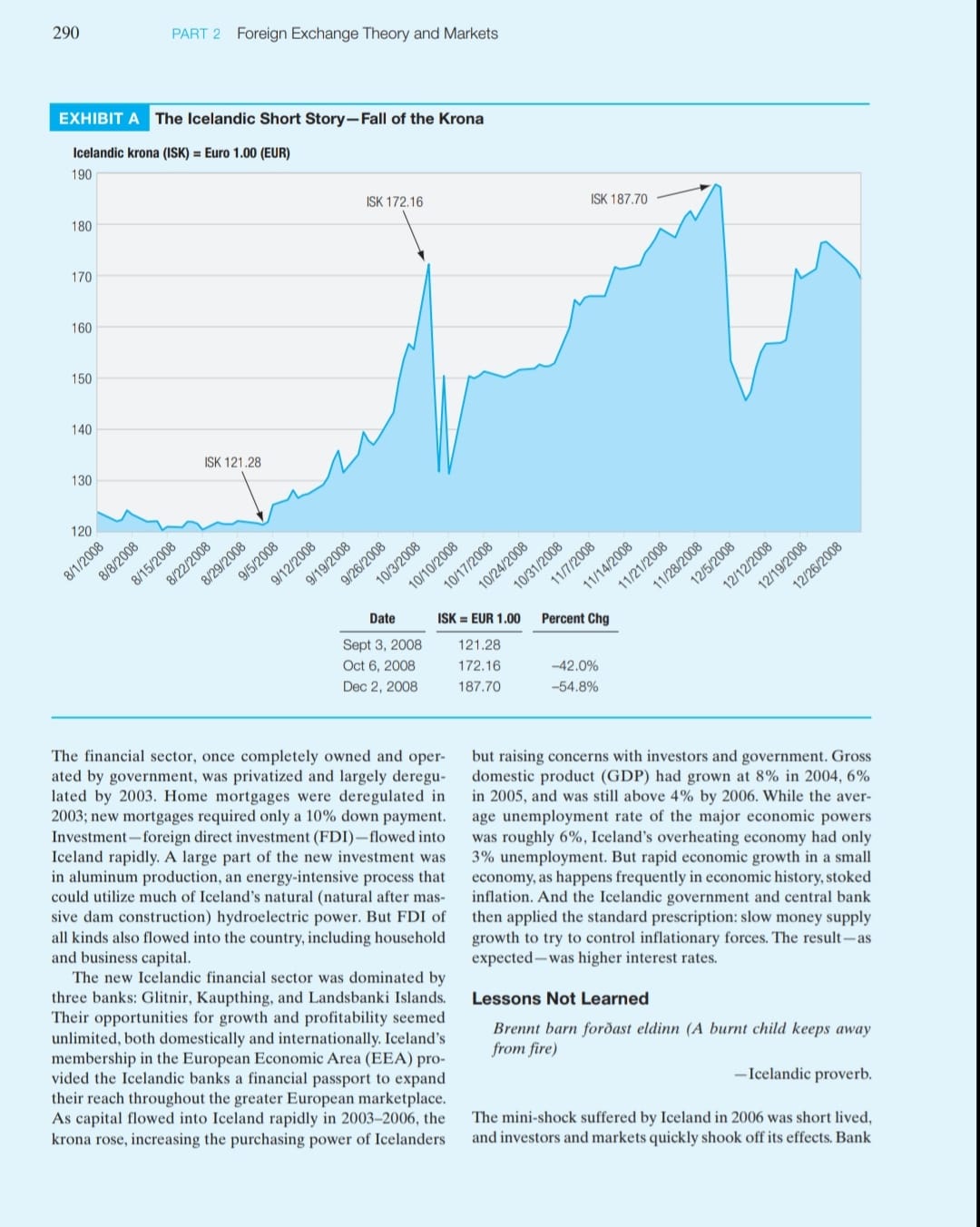

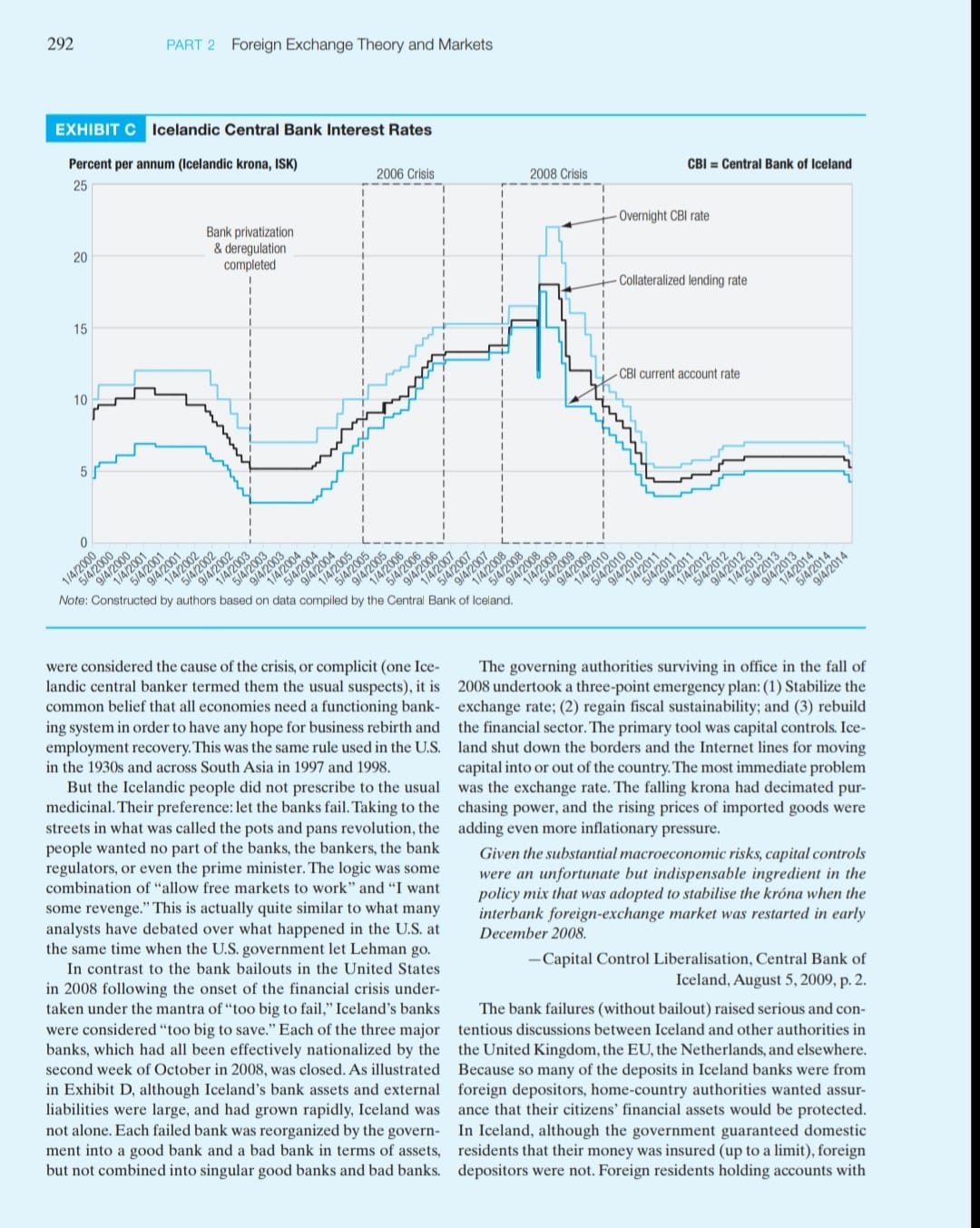

294 PART L' Foreign Exchange Theory and Markets What are the lessons to be taken from the Icelandic saga? Deregulation of the nancial system is risky? Banks and bankers are not to be trusted? Cross-border banking is risky? Inadequate crossborder banking regulations allow banks to borrow too mueh. where they shouldn't. and invest too much where they shouldn't? Bank loan books and bank capital need to be regulated? Small countries cannot con- duct independent monetary policy? Small sh should not swim in big ponds? Or . . . The paper concludes that. to prevent future crises of sinit'irtr proportions. it is impossible for a small country to have a large international banking sector. its own citr- rency and an independent monetary policy. Rob Spruk. "Iceland's Economic and Financial Crisis: Causes. Consequences and Implications,\" European Enterprise Institute. February 23. 2010. Mini-Case Questions 1. 4. Do you think a country the size of Iceland a Lilliputianis more or less sensitive to the potential impacts of global capital movements? Many countries have used interest rate increases to protect their currencies for many years What are the pros and cons of using this strategy? How does the Iceland story [it with our understanding of the impossible trinity? in your opinion. which of the three elements of the trinity should lce land have taken steps to control to a greater degree? In the case of Iceland. the country was able to sustain a large current account decit for several years. and at the same time have ever-rising interest rates and a stronger and stronger currency. Then one day. it all changed. How does that happen? Foreign Exchange Rate Determination and Intervention CHAPTER 9 293 EXHIBIT D Icelandic Banks Compared to Others in Potential Crisis 1000% 900% 800% 7009 600% 500% 4009 300% 200% 100% 0% Iceland Ireland Hong Kong SAR Singapore Switzerland Bank Assets to GDP - 2001 Bank Assets to GDP - 2007 Bank External Debt Liabilities to GDP - 2001 Bank External Debt Liabilities to GDP - 2007 Source: IMF and Iceland Central Bank. Icelandic financial institutions were prohibited from pulling reserves proved inadequate. The answer was no, basically the money out of Iceland and out of the krona. summarized as "talk to the IMF (International Monetary Capital controls were introduced in October-upon the Fund)." In the end the IMF did indeed help, providing recommendation of the IMF-and then altered and mag- a Stand-By Arrangement to provide favorable access to nified in revisions in November and December 2008 and foreign capital markets and additional credit and cred- again in March of 2009. ibility for the Icelandic government's recovery program. Payments linked to current account transactions and The krona's value was stabilized, as seen previously in inward FDI were released after a short period of time. Exhibit B, but has stayed weaker, which has helped return Thus, transactions involving actual imports and exports the merchandise trade account to surplus in subsequent of goods and services are allowed and so are interest pay- years. Inflation took a bit longer to get under control, but ments, if exchanged within a specified time limit. Most was successfully cut to near 2% by the end of 2010. Iceland capital transactions are controlled both for residents and remains a heavily indebted Lilliputian country (according non-residents; that is, their ability to shift between ISK and to the Financial Times), in both public debt and private FX is restricted. Krona-denominated bonds and other like debt as a percentage of GDP. instruments cannot be converted to foreign currency upon maturity. The proceeds must be reinvested in other ISK 20-20 Hindsight instruments. Furthermore, the Rules require residents to Interestingly, in the years since the crisis, there has been a repatriate all foreign currency that they acquire. reversal (or as one writer described it, 20-20-20-20 hind- - Capital Control Liberalisation, Central Bank of sight) in the assessment of Iceland's response to the crisis. Iceland, August 5, 2009, p. 23. In the first few years it was believed that Iceland's recovery would be shorter and stronger than other European coun- It also turned out that the crisis itself was not such a big tries falling into crisis in 2009 and 2010, like Ireland, Estonia, surprise. The Central Bank of Iceland had approached the and others. But then, after a few more years of experience, European Central Bank (ECB), the Bank of England, and revised hindsight concluded that Iceland's recovery has the U.S. Federal Reserve in the spring of 2008 (months been slower, weaker, and less successful than that of others, before the crisis erupted), hoping to arrange foreign partly a result of allowing the banks to fail, partly a result of exchange swap agreements in case its foreign exchange the country's "addiction" to capital controls.290 PART 2 Foreign Exchange Theory and Markets EXHIBIT A The Icelandic Short Story-Fall of the Krona Icelandic krona (ISK) = Euro 1.00 (EUR) 190 ISK 172.16 ISK 187.70 180 170 160 150 140 ISK 121.28 130 120 8/1/2008 8/8/2008 8/15/2008 8/22/2008 8/29/2008 9/5/2008 9/12/2008 9/19/2008 9/26/2008 10/3/2008 10/10/2008 10/17/2008 10/24/2008 10/31/2008 11/7/2008 11/14/2008 11/21/2008 11/28/2008 12/5/2008 12/12/2008 12/19/2008 12/26/2008 Date ISK = EUR 1.00 Percent Chg Sept 3, 2008 121.28 Oct 6, 2008 172.16 -42.0% Dec 2, 2008 187.70 -54.8% The financial sector, once completely owned and oper- but raising concerns with investors and government. Gross ated by government, was privatized and largely deregu- domestic product (GDP) had grown at 8% in 2004, 6% lated by 2003. Home mortgages were deregulated in in 2005, and was still above 4% by 2006. While the aver- 2003; new mortgages required only a 10% down payment. age unemployment rate of the major economic powers Investment-foreign direct investment (FDI)-flowed into was roughly 6%, Iceland's overheating economy had only Iceland rapidly. A large part of the new investment was 3% unemployment. But rapid economic growth in a small in aluminum production, an energy-intensive process that economy, as happens frequently in economic history, stoked could utilize much of Iceland's natural (natural after mas- inflation. And the Icelandic government and central bank sive dam construction) hydroelectric power. But FDI of then applied the standard prescription: slow money supply all kinds also flowed into the country, including household growth to try to control inflationary forces. The result-as and business capital. expected- was higher interest rates. The new Icelandic financial sector was dominated by three banks: Glitnir, Kaupthing, and Landsbanki Islands. Lessons Not Learned Their opportunities for growth and profitability seemed unlimited, both domestically and internationally. Iceland's Brennt barn fordast eldinn (A burnt child keeps away membership in the European Economic Area (EEA) pro- from fire) vided the Icelandic banks a financial passport to expand -Icelandic proverb. their reach throughout the greater European marketplace. As capital flowed into Iceland rapidly in 2003-2006, the The mini-shock suffered by Iceland in 2006 was short lived, krona rose, increasing the purchasing power of Icelanders and investors and markets quickly shook off its effects. BankForeign Exchange Fiate Determination and Intervention - --'-f i 5 - 291 _XHIBIT B The Icelandic KronaEuropean Euro Spot Exchange Rate Icelandic mm: {Isa} . Earn 1.00 (sun: 20\" 2006 Crisis 180 150 140 120 100 80 x. 50 L .aaaaaaaaas :amasaeaaaaseaa madame; s K\" s 2008 Crisis lending returned. and within two years the Icelandic econ- omy was in more troubie than ever. In 2007 and 2008 Iceland's interest rates continued to riseboth market rates {like bank overnight rates) and central bank policy rates Global credit agencies rated the major Icelandic banks AAA. Capital owed into Icelandic banks. and the banks in turn funneled that capital into all possible investments (and loans] domestically and interna- tionally. Iceland's banks created Ice-save. an Internet bank- ing system to reach out to depositors in Great Britain and the Netherlands. It worked. Iceland's bank balance sheets grew 100% of GDP in 2003 to just below 1.000% of GDP by 2008. Iceiand's banks were now more international than Ice- landic. {By the end of 200'? their total deposits were 45% in British pounds. 22% Icelandic krona. 16% euro. 3% dollar, and 14% other.) Iceiandic real estate and equity prices boomed. Increased consumer and business spending resulted in the growth in merchandise and service imports. while the rising krona depressed exports. The merchandise service. and income balances in the current account all went into deficit. Behaving like an emerging market country that had just discovered oi]. Icelanders dropped their fishing hooks. abandoned their boats. and became bankers. Every- one wanted a piece of the pie. and the pie appeared to be growing at an innite rate. Everyone could become rich. Then it all stopped. suddenly. without notice. Whether it was caused by the failure of Lehman Brothers in the U.S.. or was a victim of the same forces. it is hard to say. But beginning in September 2008 the krona started falling and capital started eeing. Interest rates were increased even further to try to entice (or "bribe"] money to stay in Iceland and in krona. None of it worked.As illustrated by Exhibit B. the krona's fall was large. dramatic. and some- what permanent. In retrospect. the 2006 crisis had been only a ripple: 2008 proved to be a tsunami. Now those same interest rates, which had been driven up by both markets and policy. prevented any form of renewal-mortgage loans were either impossible to get or impossible to afford. business loans were too expensive given the new limited business outlook.The international interbank market. which had largely frozen up during the midst of the crisis in September and October 2008. now treated the Icelandic financial sector like a leper.As illus- trated by Exhibit C. interest rates had a long way to fall to reach earth (the Central Bank of Iceland's overnight rate rose to well over 20%]. Aftermath: The Policy Response There is a common precept observed by governments and central banks when they fall victim to nancial crises: save the banks. Regardless of whether the banks and bankers 292 PART 2 Foreign Exchange Theory and Markets EXHIBIT C Icelandic Central Bank Interest Rates Percent per annum (Icelandic krona, ISK) CBI = Central Bank of Iceland 2006 Crisis 2008 Crisis 25 Overnight CBI rate Bank privatization 20 & deregulation completed Collateralized lending rate 15 - CBI current account rate 10 5 14/2000 2000 9005 12006 514/2080 9/4/2001 1147200 914/2001 5/4/2002 914/2002 1/4/2003 5/4/2003 914/2003 5/4/2004 2412004 $14/200 314/200 11412007 314 2007 914/2007 1/4/2008 ja/2008 1/4/2009 9/4/2008 5/4/2009 1/4 2010 9/4/2009 9/4 2010 1/4/2011 9/4/2010 914 2011 D/4/2011 0/4 2012 1/4/2012 9/4/2012 9/4 2013 1/472013 1/4/2014 914/2013 4/2014 9/4/2 Note: Constructed by authors based on data compiled by the Central Bank of Iceland. were considered the cause of the crisis, or complicit (one Ice- The governing authorities surviving in office in the fall of landic central banker termed them the usual suspects), it is 2008 undertook a three-point emergency plan: (1) Stabilize the common belief that all economies need a functioning bank- exchange rate; (2) regain fiscal sustainability; and (3) rebuild ing system in order to have any hope for business rebirth and the financial sector. The primary tool was capital controls. Ice- employment recovery. This was the same rule used in the U.S. land shut down the borders and the Internet lines for moving in the 1930s and across South Asia in 1997 and 1998. capital into or out of the country. The most immediate problem But the Icelandic people did not prescribe to the usual was the exchange rate. The falling krona had decimated pur- medicinal. Their preference: let the banks fail. Taking to the chasing power, and the rising prices of imported goods were streets in what was called the pots and pans revolution, the adding even more inflationary pressure. people wanted no part of the banks, the bankers, the bank Given the substantial macroeconomic risks, capital controls regulators, or even the prime minister. The logic was some were an unfortunate but indispensable ingredient in the combination of "allow free markets to work" and "I want policy mix that was adopted to stabilise the krona when the some revenge." This is actually quite similar to what many interbank foreign-exchange market was restarted in early analysts have debated over what happened in the U.S. at December 2008. the same time when the U.S. government let Lehman go. In contrast to the bank bailouts in the United States - Capital Control Liberalisation, Central Bank of in 2008 following the onset of the financial crisis under- Iceland, August 5, 2009, p. 2. taken under the mantra of "too big to fail," Iceland's banks The bank failures (without bailout) raised serious and con- were considered "too big to save." Each of the three major tentious discussions between Iceland and other authorities in banks, which had all been effectively nationalized by the the United Kingdom, the EU, the Netherlands, and elsewhere. second week of October in 2008, was closed. As illustrated Because so many of the deposits in Iceland banks were from in Exhibit D, although Iceland's bank assets and external foreign depositors, home-country authorities wanted assur- liabilities were large, and had grown rapidly, Iceland was ance that their citizens' financial assets would be protected. not alone. Each failed bank was reorganized by the govern- In Iceland, although the government guaranteed domestic ment into a good bank and a bad bank in terms of assets, residents that their money was insured (up to a limit), foreign but not combined into singular good banks and bad banks. depositors were not. Foreign residents holding accounts withMini-Case Iceland-A Small Country in with economic change. As inflationary pressures rose, the a Global Crisis Central Bank of Iceland had tightened monetary policy, There was the short story, and the longer more complex interest rates rose. Higher interest rates attracted capital story. Iceland had seen both. And what was the moral of the from outside Iceland, primarily European capital, and the story? Was the moral that it's better to be a big fish in a little banking system was flooded with capital. The banks in turn pond, or was it once burned twice shy, or something else? invested heavily in everything from real estate to Land Iceland was a country of only 300,000 people. It was rel- Rovers (or Game Overs as they became known). atively geographically isolated, but its culture and economy Then September of 2008 happened. The global financial were heavily intertwined with that of Europe, specifically crisis, largely originating in the United States and its real northern Europe and Scandinavia. A former property of estate-securitized-mortgage-debt-credit-default-swap cri- Denmark, it considered itself both independent and yet sis brought much of the international financial system and Danish. Iceland's economy was historically driven by fish- major industrial economies to a halt. Investments failed- ing and natural resource development. Although not flashy in the U.S., in Europe, in Iceland. Loans to finance those by any sense of the word, they had proven to be solid and bad investments fell delinquent. The Icelandic economy lasting industries, and in recent years, increasingly profit- and its currency-the krona-collapsed. As illustrated in able. At least that was until Iceland discovered "banking." Exhibit A, the krona fell more than 40% against the euro in roughly 30 days, more than 50% in 90 days. Companies failed, banks failed, unemployment grew, and inflation boomed. The Icelandic Crisis: The Short Story Eventually, a long, slow, and painful recovery began. Iceland's economy had grown very rapidly in the 2000 to 2008 period. Growth was so strong and so rapid that inflation- The Icelandic Crisis: The Longer Story an ill of the past in most of the economic world - was a The longer story of Iceland's crisis has its roots in the growing problem. As a small, industrialized and open econ- mid-1990s, when Iceland, like many other major indus- omy, capital was allowed to flow into and out of Iceland trial economies, embraced privatization and deregulation. 4Copyright @ 2015 Thunderbird School of Global Management, Arizona State University. All rights reserved. This case was prepared by Professor Michael H. Moffett for the purpose of classroom discussion only

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!