Question: QUESTION 1 The attached data set provides information in Eviews format about the following variables Gross Domestic Product =GDP Velocity of money = M2V Federal

QUESTION 1

The attached data set provides information in Eviews format about the following variables

Gross Domestic Product =GDP Velocity of money = M2V Federal Debt as % of GDP =debt Gross private saving = save

Run the regression of GDP on M2V and Debt and answer the following questions.

homework all.wf1

QUESTION 2

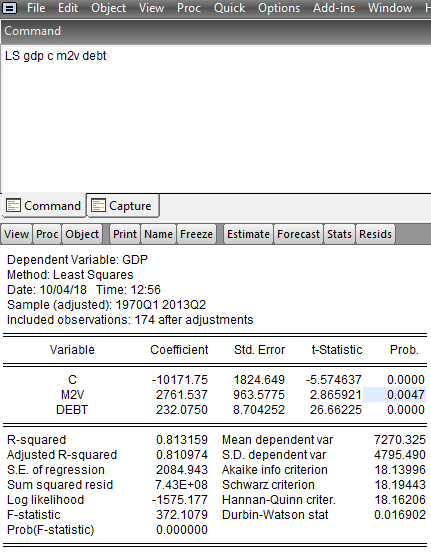

Use the Eviews results in question one and choose the correct answer.

| the sign of M2V and debt coefficients make sense because as the velocity of money increases, the debt increases too. | ||

| the sign of M2V and debt coefficients make sense because as the velocity of money increases so does GDP and as the debt increases, so does GDP increases. | ||

| the sign of debt is not correct. it should be positive | ||

| the sign of velocity is not correct, it should be negative. |

QUESTION 3

Interpret the coefficient of M2V

| As GDP increase, M2V increase as much as 2761.53 . | ||

| If Debt increases by, GDP will increase by 232.07 units. | ||

| If M2V increases by I unit , GDP will increase by 2761 units, assuming Debt remains constant. | ||

| If GDP increases by 1 units, Debt will increase by 232.07 units, assuming all other variables remain constant. |

QUESTION 4

The R sqaured of the regression shows that:

| the regression is a good fit. | ||

| If all the variables increase by 1 unit GDP will increase by 81% | ||

| 81% of variation in GDP around its mean is explained by M2V and Debt | ||

| we should not use R squared to measure goodness of fit. |

QUESTION 5

Choose one of the following answers:

| The null hypothesis for T test in front of M2v is H0: the sample slope = 0 | ||

| The null hypothesis for T test in front of M2v is H0: GDP has no effect on M2V in reality | ||

| The null hypothesis for T test in front of debt is H0: Debt has no effect on GDP in reality. | ||

| The null hypothesis for T test in front of debt is H0: Debt has a significant effect on GDP |

QUESTION 6

the degree of freedom for the estimated t values is

| 174 | ||

| 172 | ||

| 171 | ||

| 170 |

QUESTION 7

The Estimated T values implies:

| We can reject the null hypothesis at 5% level of significance. | ||

| We should Drop M2V and Debt from the regression. | ||

| the effects of M2V and Debt on GDP are statistically different from zero at 5% level of significance. | ||

| the effects of M2V and Debt on GDP are statistically zero at 5% level of significance. |

QUESTION 8

choosing the significance level of 5% means

| 5% of times we are wrong when we reject the null. | ||

| 5% of times we are correct when we reject the null. | ||

| 5% of times we are correct when we can not reject the null. | ||

| 5% of times we are wrong when we can not reject the null. |

QUESTION 10

Choose one of the following answers.

| The estimated F statistic of the regression tests the null hypothesis that R squaredof the regression is significantly different from zero. | ||

| The estimated F statistic of the regression tests the null hypothesis that the joint effect of all the variables in the regression is significantly different from zero. | ||

| The F test is one sided test. | ||

| All other answers are correct. |

QUESTION 11

choose one of the following answers.

| The degree of freedom of the estimated F in the regression is 3, 174 and it rejects the null hypothesis that R squared is zero. | ||

| The degree of freedom of the estimated F in the regression is 2, 171 and it rejects the null hypothesis that R squared is zero. | ||

| The degree of freedom of the estimated F in the regression is 3, 172 and it rejects the null hypothesis that R squared is zero. | ||

| The degree of freedom of the estimated F in the regression is 2, 171 and it can not reject the null hypothesis that R squared is zero. |

a File Edit Object View Proc Quick Options Add-ins WindowH Command LS gdp c m2v debt CommandCapture View Proc Object Print Name Freeze Estimate Forecast Stats Resids Dependent Variable: GDP Method: Least Squares Date: 10/04/18 Time: 12:56 Sample (adjusted): 1970Q1 201302 Included observations: 174 after adjustments Variable Coefficient Std. Error t-Statistic Prob M2V DEBT 10171.75 1824.649 -5.574637 0.0000 2761.537 963.5775 2.865921 0.0047 232.0750 8.704252 26.66225 0.0000 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.813159 Mean dependent var 0.810974 S.D. dependent var 2084.943 Akaike info criterion 7.43E+08 Schwarz criterion 1575.177 Hannan-Quinn criter 372.1079 Durbin-Watson stat 0.000000 7270.325 4795.490 18.13996 18.19443 18.16206 0.016902

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts