Question: Question 1: This question has two parts: part (a) accepts or reject special order (chapter 10) and part (b) discounted cash flow (chapter 13) a)

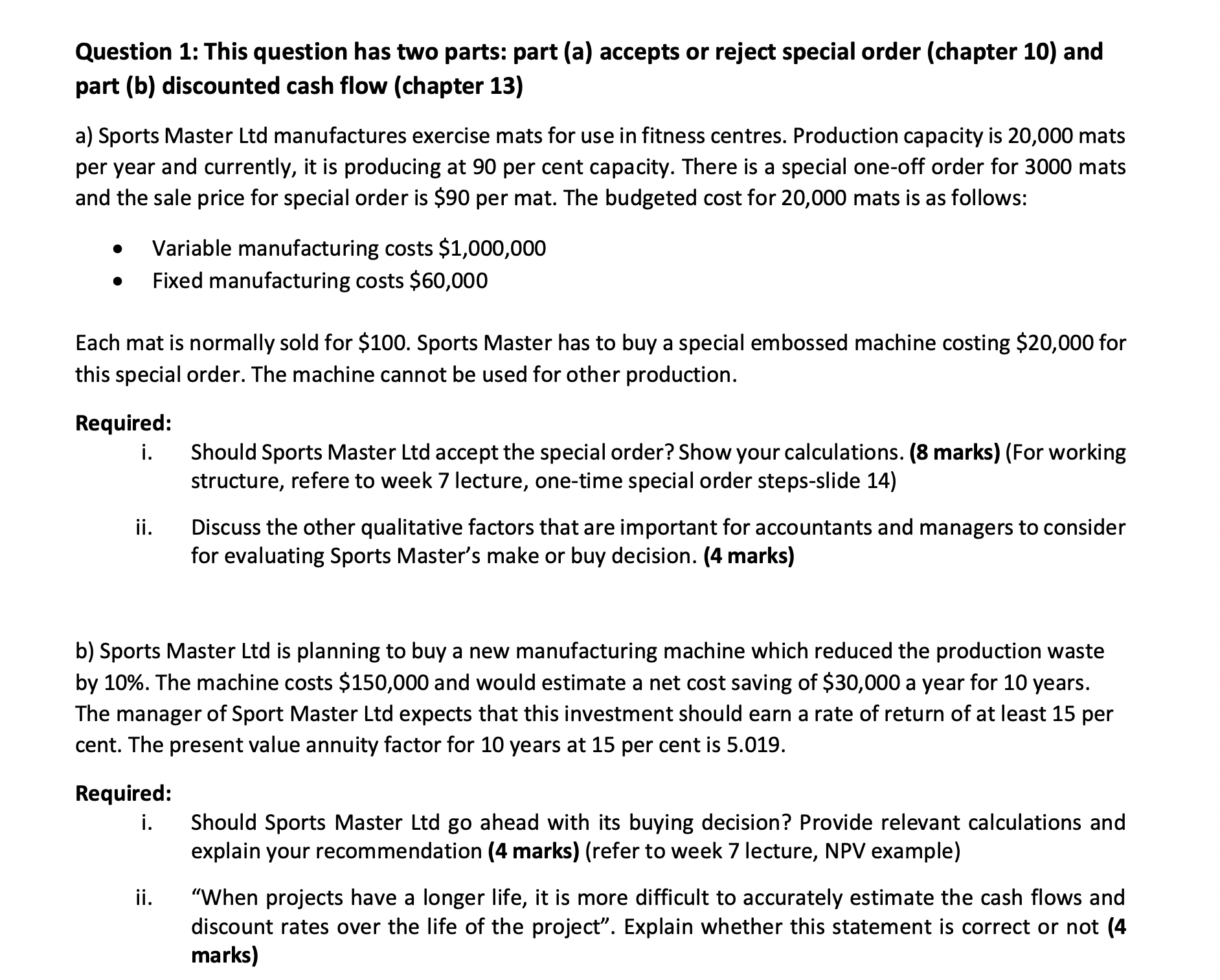

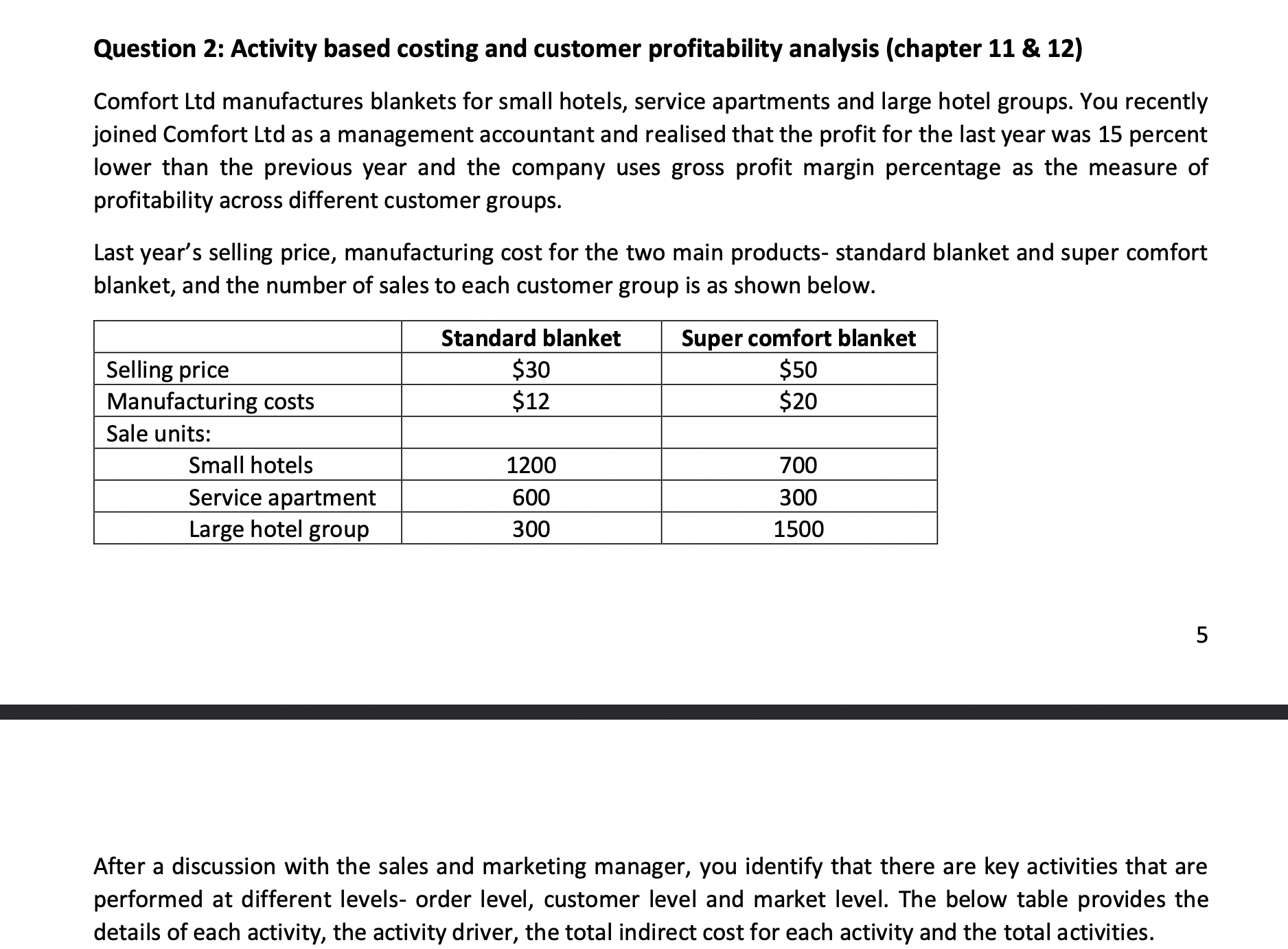

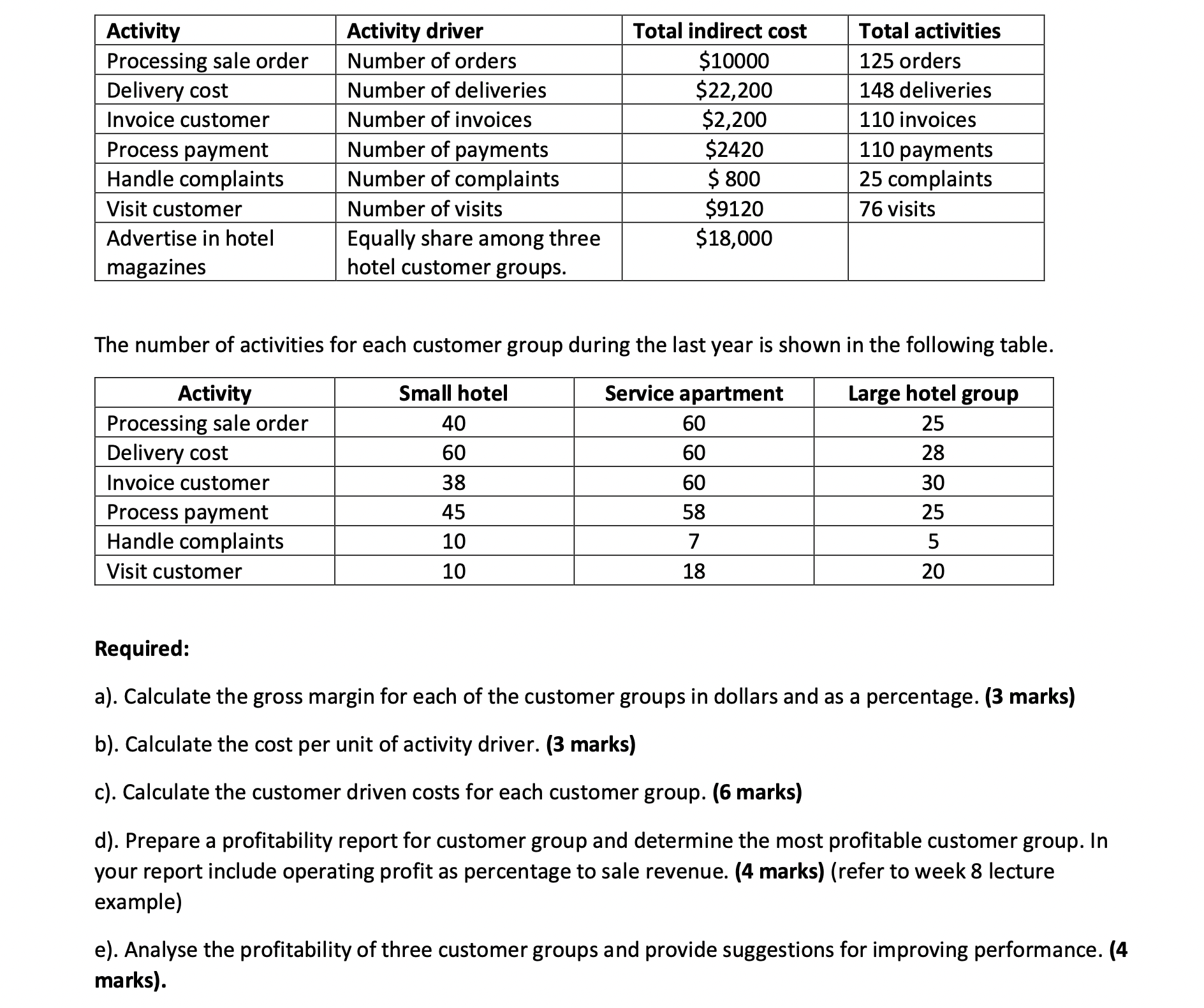

Question 1: This question has two parts: part (a) accepts or reject special order (chapter 10) and part (b) discounted cash flow (chapter 13) a) Sports Master Ltd manufactures exercise mats for use in fitness centres. Production capacity is 20,000 mats per year and currently, it is producing at 90 per cent capacity. There is a special one-off order for 3000 mats and the sale price for special order is $90 per mat. The budgeted cost for 20,000 mats is as follows: 0 Variable manufacturing costs $1,000,000 0 Fixed manufacturing costs $60,000 Each mat is normally sold for $100. Sports Master has to buy a special embossed machine costing $20,000 for this special order. The machine cannot be used for other production. Required: i. Should Sports Master Ltd accept the special order? Show your calculations. (8 marks) (For working structure, refere to week 7 lecture, one-time special order steps-slide 14) ii. Discuss the other qualitative factors that are important for accountants and managers to consider for evaluating Sports Master's make or buy decision. (4 marks) b) Sports Master Ltd is planning to buy a new manufacturing machine which reduced the production waste by 10%. The machine costs $150,000 and would estimate a net cost saving of $30,000 a year for 10 years. The manager of Sport Master Ltd expects that this investment should earn a rate of return of at least 15 per cent. The present value annuity factor for 10 years at 15 per cent is 5.019. Required: i. Should Sports Master Ltd go ahead with its buying decision? Provide relevant calculations and explain your recommendation (4 marks) (refer to week 7 lecture, NPV example) ii. "When projects have a longer life, it is more difficult to accurately estimate the cash flows and discount rates over the life of the project". Explain whether this statement is correct or not (4 marks) Question 2: Activity based costing and customer profitability analysis (chapter 11 & 12) Comfort Ltd manufactures blankets for small hotels, service apartments and large hotel groups. You recently joined Comfort Ltd as a management accountant and realised that the profit for the last year was 15 percent lower than the previous year and the company uses gross profit margin percentage as the measure of profitability across different customer groups. Last year's selling price, manufacturing cost for the two main products- standard blanket and super comfort blanket, and the number of sales to each customer group is as shown below. Standard blanket Super comfort blanket Selling price $30 $50 Manufacturing costs $12 $20 Sale units: Small hotels 1200 700 Service apartment 600 300 Large hotel group 300 1500 After a discussion with the sales and marketing manager, you identify that there are key activities that are performed at different levels- order level, customer level and market level. The below table provides the details of each activity, the activity driver, the total indirect cost for each activity and the total activities. Activity Activity driver Total indirect cost Total activities Processing sale order Number of orders $10000 125 orders Delivery cost Number of deliveries $22,200 148 deliveries Invoice customer Number of invoices $2,200 110 invoices Process payment Number of payments $2420 110 payments Handle complaints Number of complaints 5 800 25 complaints Visit customer Number of visits $9120 76 visits Advertise in hotel Equally share among three $18,000 magazines hotel customer groups. The number of activities for each customer group during the last year is shown in the following table. Activity Small hotel Service apartment Large hotel group Processing sale order Delivery cost Invoice customer Process payment Handle complaints Visit customer Required: a). Calculate the gross margin for each of the customer groups in dollars and as a percentage. (3 marks) b). Calculate the cost per unit of activity driver. (3 marks) c). Calculate the customer driven costs for each customer group. (6 marks) d). Prepare a profitability report for customer group and determine the most profitable customer group. In your report include operating profit as percentage to sale revenue. (4 marks) (refer to week 8 lecture example) e). Analyse the profitability of three customer groups and provide suggestions for improving performance. (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts