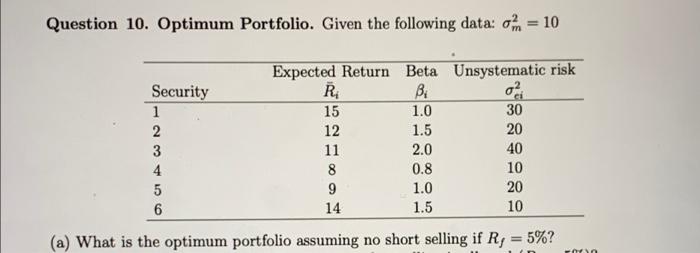

Question: Question 10. Optimum Portfolio. Given the following data: om = 10 R Security 1 2 3 4 5 6 Expected Return Beta Unsystematic risk Bi

Question 10. Optimum Portfolio. Given the following data: om = 10 R Security 1 2 3 4 5 6 Expected Return Beta Unsystematic risk Bi 15 1.0 30 12 1.5 20 11 2.0 40 8 0.8 10 9 1.0 20 14 1.5 10 (a) What is the optimum portfolio assuming no short selling if R, = 5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock