Question: Question 12 1 pts State Return State il Return Investment State Ill Return (p=0.3) (p=0.5) (0-02) A 5% 7% 2% B 6% 8% 396 Given

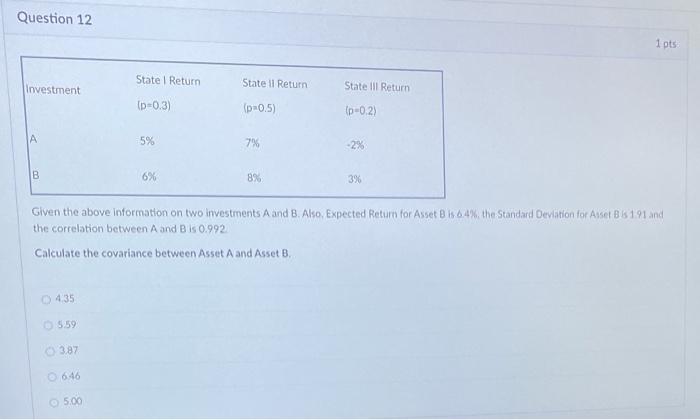

Question 12 1 pts State Return State il Return Investment State Ill Return (p=0.3) (p=0.5) (0-02) A 5% 7% 2% B 6% 8% 396 Given the above information on two investments A and B. Also, Expected Return for Asset B 64%. the Standard Deviation for Asset B & 191 and the correlation between A and B is 0.992 Calculate the covariance between Asset A and Asset B. 435 5.59 387 6.46 5.00

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock