Question: Question 12 8 pts Please answer the next question based on the following quotes on currency options contracts for Swiss francs (CHF), where each

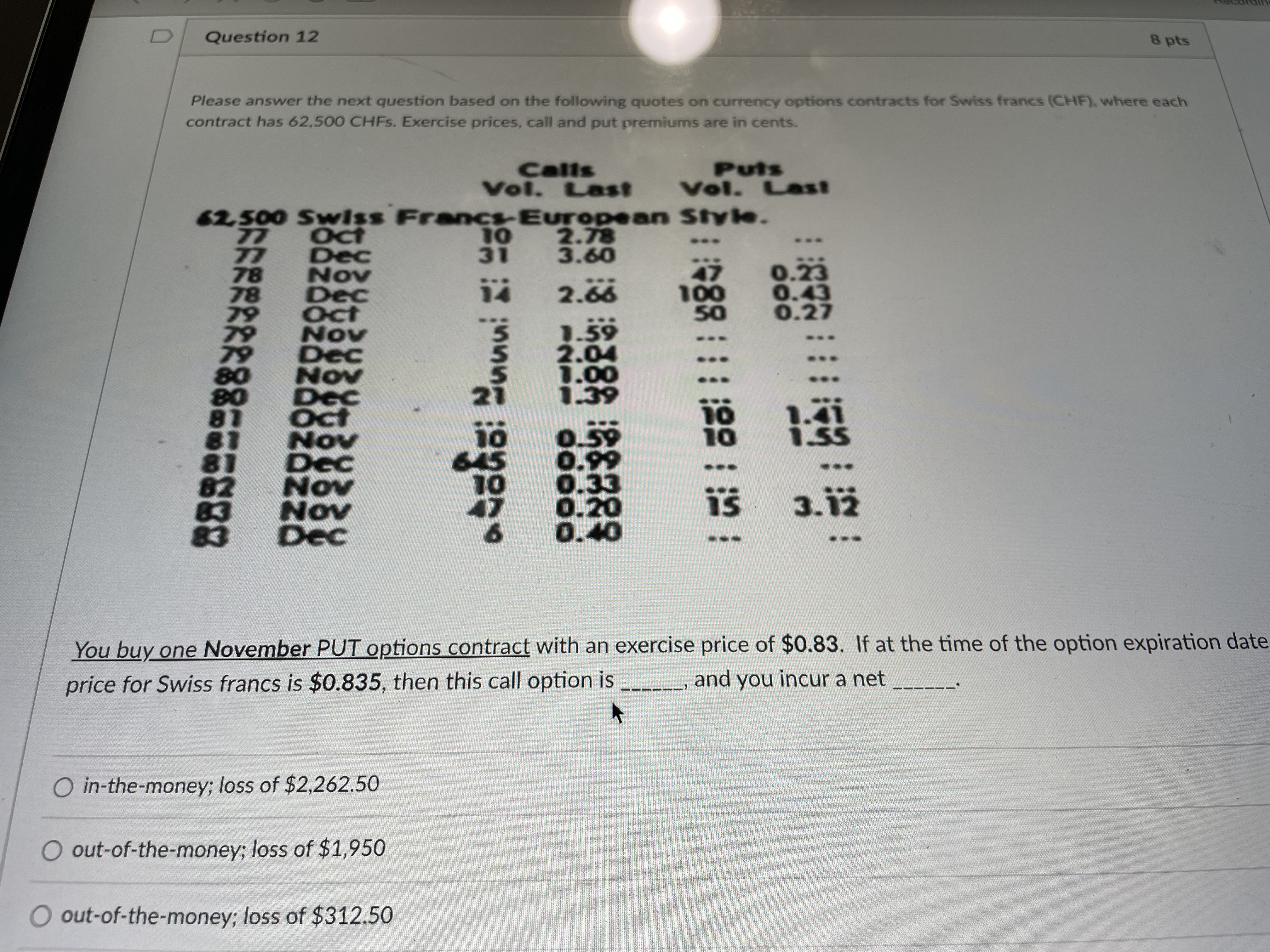

Question 12 8 pts Please answer the next question based on the following quotes on currency options contracts for Swiss francs (CHF), where each contract has 62,500 CHFs. Exercise prices, call and put premiums are in cents. Calls Vol. Last Puts Vol. Last 62,500 Swiss Francs-European Style. 77 Oct 10 2.78 Dec 31 3.60 Nov Dec 127 i 2.66 47 100 Oct 1988 0.23 0.43 50 0.27 Nov 79 Dec 80 Nov 80 Dec 81 Oct 81 Nov 81 Dec 82 Nov 83 Nov 83 Dec sada unui 1.59 2.04 1.00 1.39 0.59 10 10 13 0.99 0.33 0.20 3.12 0.40 You buy one November PUT options contract with an exercise price of $0.83. If at the time of the option expiration date price for Swiss francs is $0.835, then this call option is ___________, and you incur a net O in-the-money; loss of $2,262.50 O out-of-the-money; loss of $1,950 O out-of-the-money; loss of $312.50

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts