Question: Question 12 Please answer the next questions based on the following Chase Bank's direct spot and forward markets quotes for EUR right now (1/1/XX), and

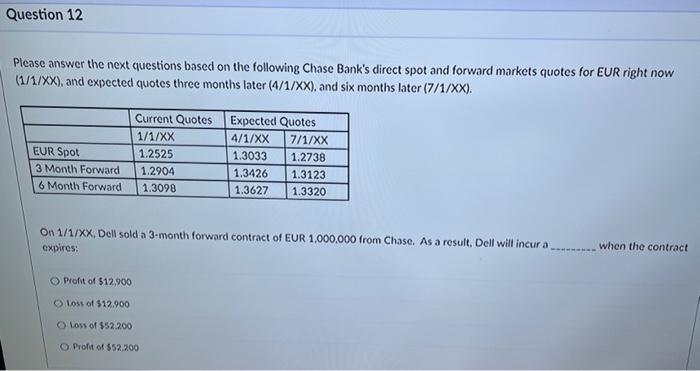

Question 12 Please answer the next questions based on the following Chase Bank's direct spot and forward markets quotes for EUR right now (1/1/XX), and expected quotes three months later (4/1/XX), and six months later (7/1/XX). Current Quotes Expected Quotes 1/1/XX 4/1/XX 1.2525 1.3033 EUR Spot 3 Month Forward 1.2904 6 Month Forward 1.3098 1.3426 1.3627 O Profit of $12,900 O Loss of $12.900 O Loss of $52.200 O Profit of $52.200 7/1/XX 1.2738 1.3123 1.3320 On 1/1/XX, Dell sold a 3-month forward contract of EUR 1,000,000 from Chase. As a result, Dell will incur a expires: when the contract

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock