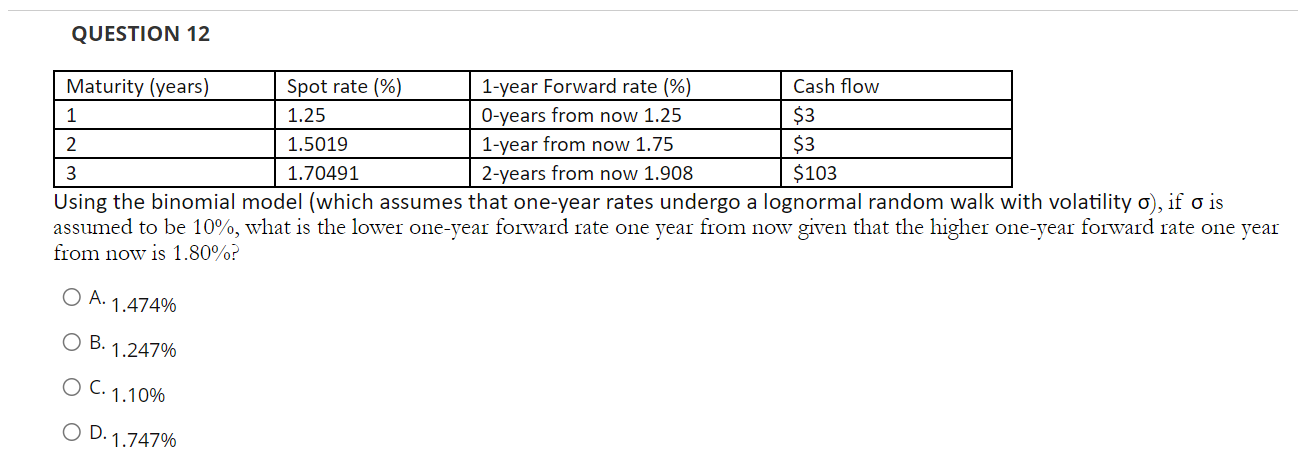

Question: QUESTION 12 Using the binomial model (which assumes that one-year rates undergo a lognormal random walk with volatility ), if is assumed to be 10%,

QUESTION 12 Using the binomial model (which assumes that one-year rates undergo a lognormal random walk with volatility ), if is assumed to be 10%, what is the lower one-year forward rate one year from now given that the higher one-year forward rate one year from now is 1.80% ? A. 1.474% B. 1.247% C. 1.10% D. 1.747%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock