Question: QUESTION 13 12 points Save Answer BB Default 0 Suppose the one-year transition matrix is as follows Intial Rating Ratings at year end (probability %)

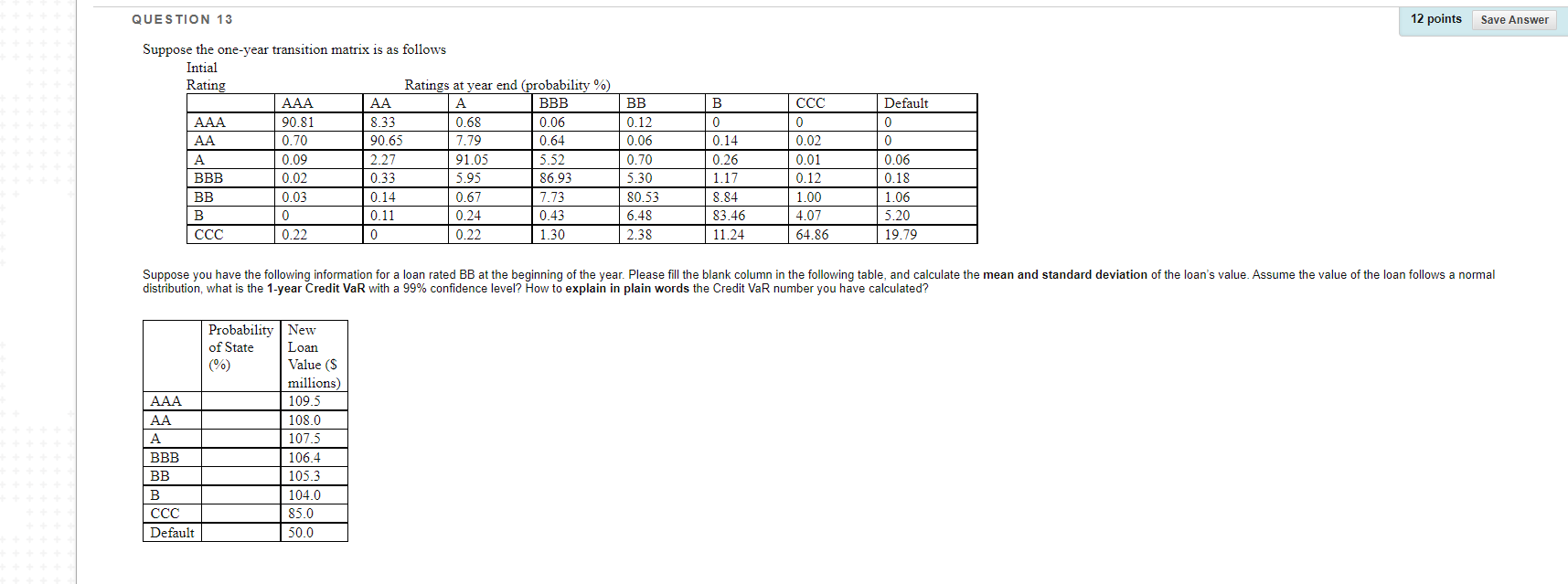

QUESTION 13 12 points Save Answer BB Default 0 Suppose the one-year transition matrix is as follows Intial Rating Ratings at year end (probability %) AAA AA A BBB AAA 90.81 8.33 0.68 0.06 AA 0.70 90.65 7.79 0.64 A 0.09 2.27 91.05 5.52 BBB 0.02 0.33 5.95 86.93 BB 0.03 0.14 0.67 7.73 B 0 0.11 0.24 0.43 0.22 0 0.22 1.30 0.12 0.06 0.70 5.30 80.53 6.48 2.38 B 0 0.14 0.26 1.17 8.84 83.46 11.24 0 0.02 0.01 0.12 1.00 4.07 64.86 0 0.06 0.18 1.06 5.20 19.79 Suppose you have the following information for a loan rated BB at the beginning of the year. Please fill the blank column in the following table, and calculate the mean and standard deviation of the loan's value. Assume the value of the loan follows a normal distribution, what is the 1-year Credit VaR with a 99% confidence level? How to explain in plain words the Credit VaR number you have calculated? AAA AA A BBB BB B CCC Default Probability New of State Loan Value (S millions) 109.5 108.0 107.5 106.4 105.3 104.0 85.0 50.0 QUESTION 13 12 points Save Answer BB Default 0 Suppose the one-year transition matrix is as follows Intial Rating Ratings at year end (probability %) AAA AA A BBB AAA 90.81 8.33 0.68 0.06 AA 0.70 90.65 7.79 0.64 A 0.09 2.27 91.05 5.52 BBB 0.02 0.33 5.95 86.93 BB 0.03 0.14 0.67 7.73 B 0 0.11 0.24 0.43 0.22 0 0.22 1.30 0.12 0.06 0.70 5.30 80.53 6.48 2.38 B 0 0.14 0.26 1.17 8.84 83.46 11.24 0 0.02 0.01 0.12 1.00 4.07 64.86 0 0.06 0.18 1.06 5.20 19.79 Suppose you have the following information for a loan rated BB at the beginning of the year. Please fill the blank column in the following table, and calculate the mean and standard deviation of the loan's value. Assume the value of the loan follows a normal distribution, what is the 1-year Credit VaR with a 99% confidence level? How to explain in plain words the Credit VaR number you have calculated? AAA AA A BBB BB B CCC Default Probability New of State Loan Value (S millions) 109.5 108.0 107.5 106.4 105.3 104.0 85.0 50.0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts