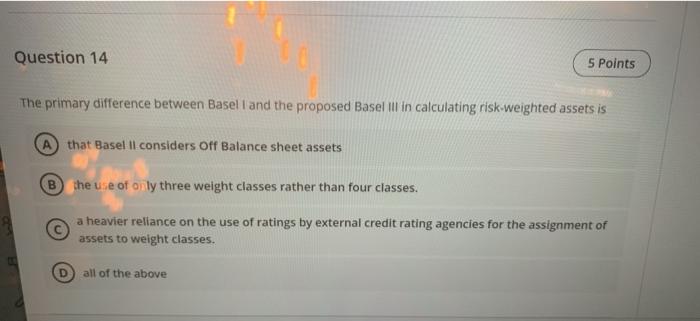

Question: Question 14 5 Points The primary difference between Basell and the proposed Basel ill in calculating risk-weighted assets is A that Basel Il considers Off

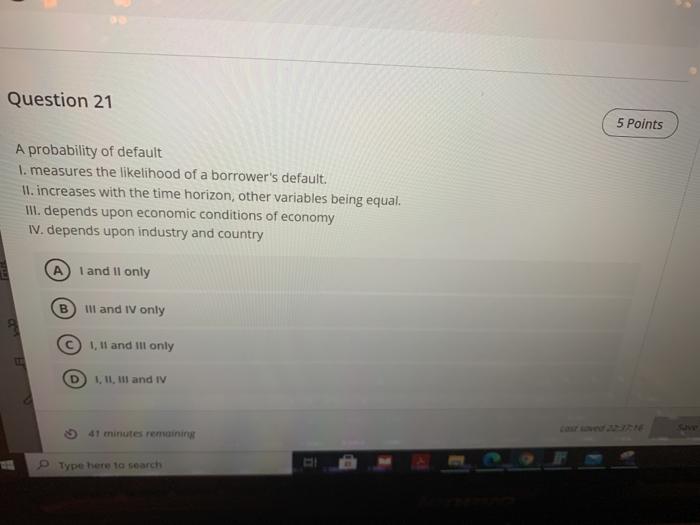

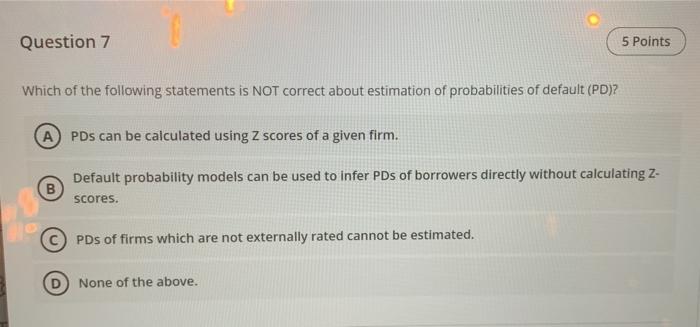

Question 14 5 Points The primary difference between Basell and the proposed Basel ill in calculating risk-weighted assets is A that Basel Il considers Off Balance sheet assets B the use of oily three weight classes rather than four classes. a heavier reliance on the use of ratings by external credit rating agencies for the assignment of assets to weight classes. D all of the above Question 21 5 Points A probability of default 1. measures the likelihood of a borrower's default. II. increases with the time horizon, other variables being equal. M. depends upon economic conditions of economy IV. depends upon industry and country A) I and II only B II and IV only 1, 11 and ill only UNI, II and IV D 41 minutes remaining Type here to search GE Question 7 5 Points Which of the following statements is NOT correct about estimation of probabilities of default (PD)? A PDs can be calculated using Z scores of a given firm. Default probability models can be used to infer PDs of borrowers directly without calculating Z- scores. PDs of firms which are not externally rated cannot be estimated. None of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts