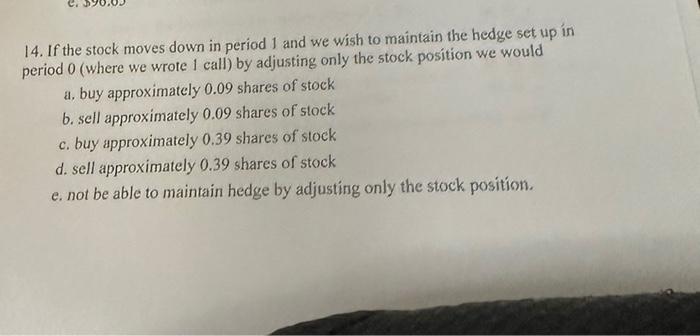

Question: question 14 is based on the info below! please read all and show work! thanks 14. If the stock moves down in period 1 and

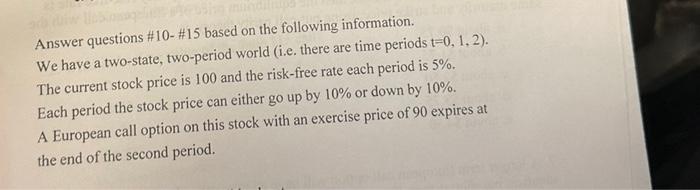

14. If the stock moves down in period 1 and we wish to maintain the hedge set, up in period 0 (where we wrote 1 call) by adjusting only the stock position we would a. buy approximately 0.09 shares of stock b. sell approximately 0.09 shares of stock c. buy approximately 0.39 shares of stock d. sell approximately 0.39 shares of stock e. not be able to maintain hedge by adjusting only the stock position. Answer questions #10 - \#15 based on the following information. We have a two-state, two-period world (i.e. there are time periods t=0,1,2 ). The current stock price is 100 and the risk-free rate each period is 5%. Each period the stock price can either go up by 10% or down by 10%. A European call option on this stock with an exercise price of 90 expires at the end of the second period

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts