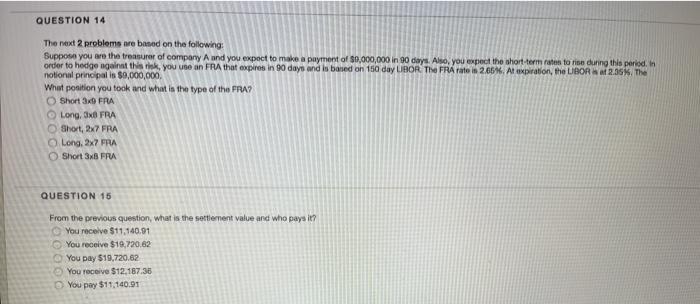

Question: QUESTION 14 The next 2 problems are based on the following: Suppose you are the treasurer of company A and you expect to make a

QUESTION 14 The next 2 problems are based on the following: Suppose you are the treasurer of company A and you expect to make a payment of $9,000,000 in 90 days. Also, you expect the short term rates to rise during this period. In order to hedge against think you use an FRA that copies in 90 days and is based on 150 day LIBOR TI FRA rate is 2.66%. Atlixpiration, the UBOR 2.35%. The notional principal is $9,000,000 What position you took and what is the type of the FRA? Short 30 FRA Long, 3x8 FRA Short, 2x7 FRA Long, 2x2 FRA Short 38 FPA QUESTION 15 From the previous question, what is the settlement value and who pays it? You receive $11.140.91 You receive $19,720.62 You pay $19,720.62 You receive $12.187.36 You pay $11.140.91

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts