Question: Question 15 1 pts Consider the expected returns and risks for two funds I and M in the table below: Ri Rm mean 0.055 0.006345

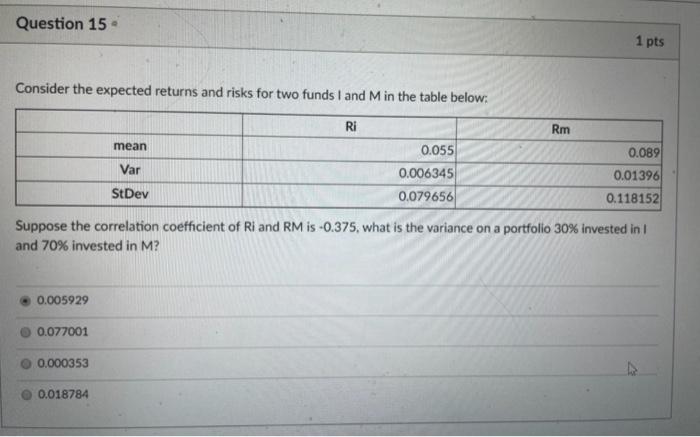

Question 15 1 pts Consider the expected returns and risks for two funds I and M in the table below: Ri Rm mean 0.055 0.006345 0.079656 0.089 0.01396 Var StDev 0.118152 Suppose the correlation coefficient of Ri and RM is -0.375, what is the variance on a portfolio 30% invested in 1 and 70% invested in M? 0.005929 0.077001 0.000353 0.018784

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock