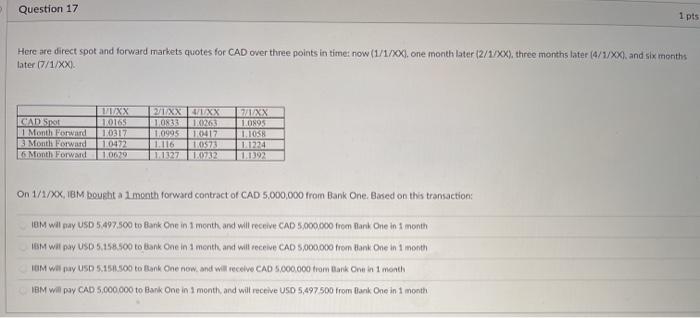

Question: Question 17 1 pts Here are direct spot and forward markets quotes for CAD over three points in time now (1/1/XX), one month later (2/1/XX),

Question 17 1 pts Here are direct spot and forward markets quotes for CAD over three points in time now (1/1/XX), one month later (2/1/XX), three months later (4/1/XX), and six months later (7/1/XX CAD Srl 1 Month Forward Month Forward 6 Month Forward XX 10165 10317 1.0472 1.0629 1XXXX LXX 1.0833 161263 LONS 1.0995 10417 10 10573 11224 11-17271.0232 11392 On 1/1/XX, IBM bought a 1 month forward contract of CAD 5,000,000 from Bank One. Based on this transaction: lem wil pay USD 5497.500 to Bank One in 1 month and will receive CAD 5.000.000 from Bank One in 3 month 1 W X USD 5.158.500 to Bank one in a month and will receive CAD 5,000,000 from Hank One in 1 month IOM Wilay USD 5.151.500 to Bank One now, and will receive CAD 5.000.000 from Bank One in 1 month IBM Wilay CAD 5,000,000 to Bank One in 1 month and will receive USD 5,497 500 from Bank One in 1 month

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts