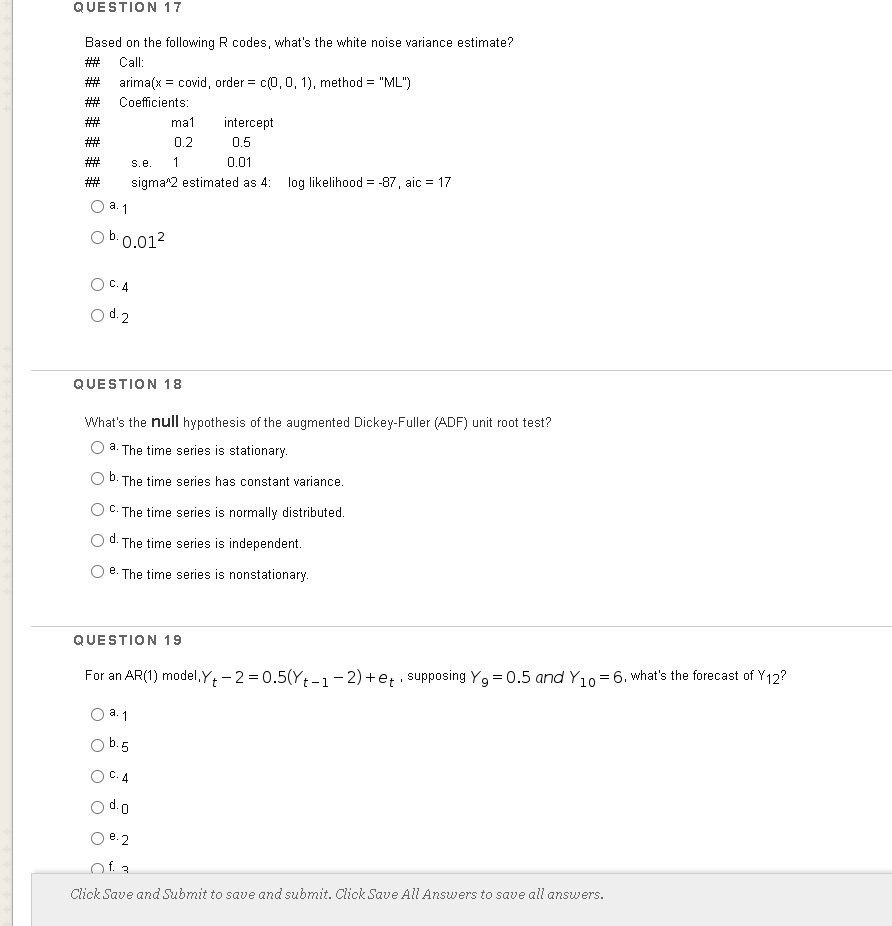

Question: QUESTION 17 Based on the following R codes, what's the white noise variance estimate? ## Call: arima(x = covid, order = c(0, 0, 1), method

QUESTION 17 Based on the following R codes, what's the white noise variance estimate? ## Call: arima(x = covid, order = c(0, 0, 1), method = "ML") ## Coefficients: ## mal intercept ## 0.2 U.5 ## S. e 0.01 sigma 2 estimated as 4: log likelihood = -87, aic = 17 0 a 1 O b. 0.012 OC.4 O d. 2 QUESTION 18 What's the null hypothesis of the augmented Dickey-Fuller (ADF) unit root test? O 3. The time series is stationary. O b. The time series has constant variance. O C. The time series is normally distributed. O d. The time series is independent O E. The time series is nonstationary. QUESTION 19 For an AR(1) model,Y, - 2 =0.5(Yt -1 -2) +et . supposing Y9 =0.5 and Y10 =6. what's the forecast of Y12? O a. 1 Ob. 5 O C. 4 O d. 0 Oe. Z Of. 3 Click Save and Submit to save and submit. Click Save All Answers to save all answers

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts