Question: Question 2 0 / 10 points Figeroua Corporation estimates that it lost $90,000 in inventory from a recent flood. The following information is available from

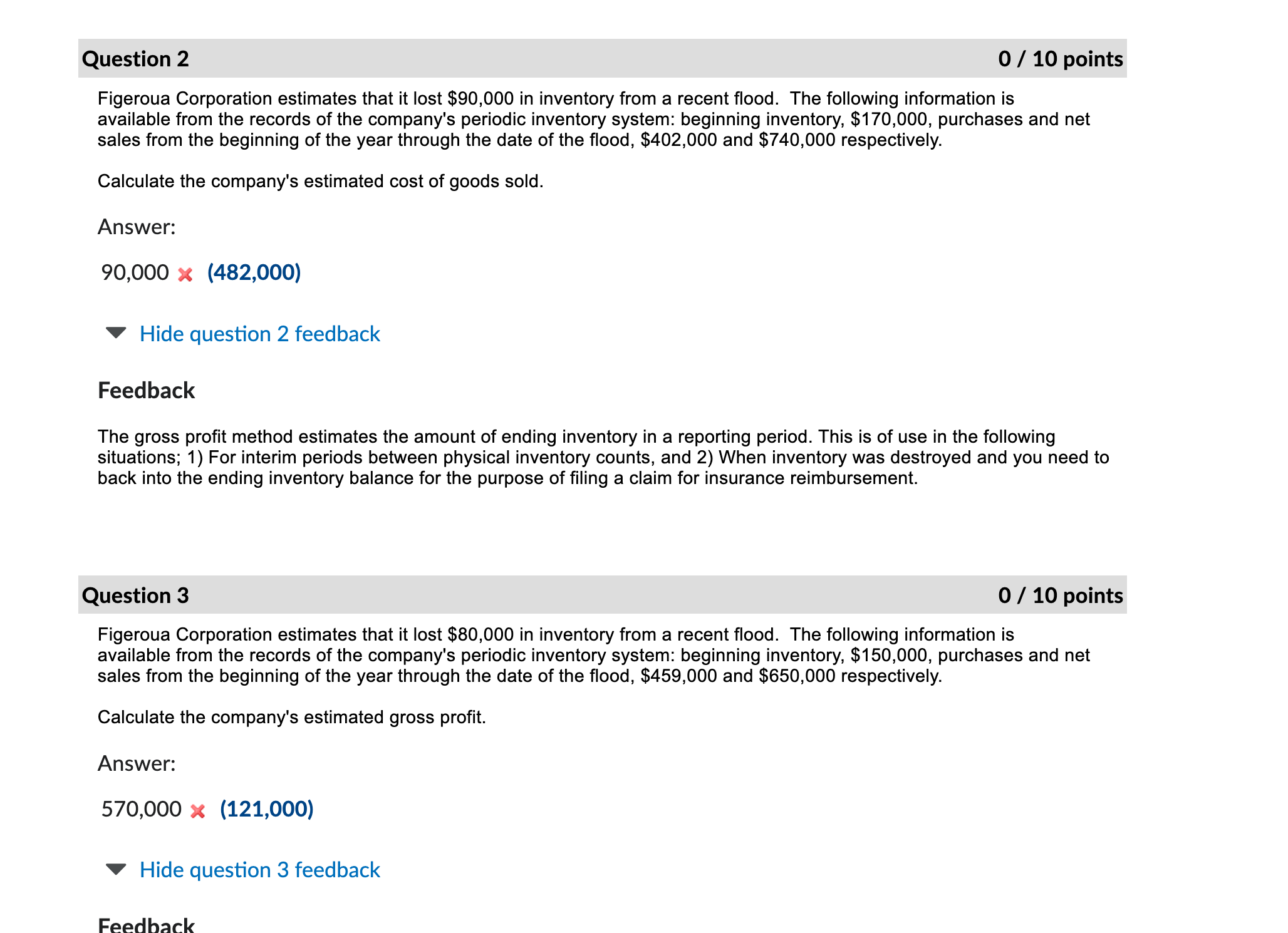

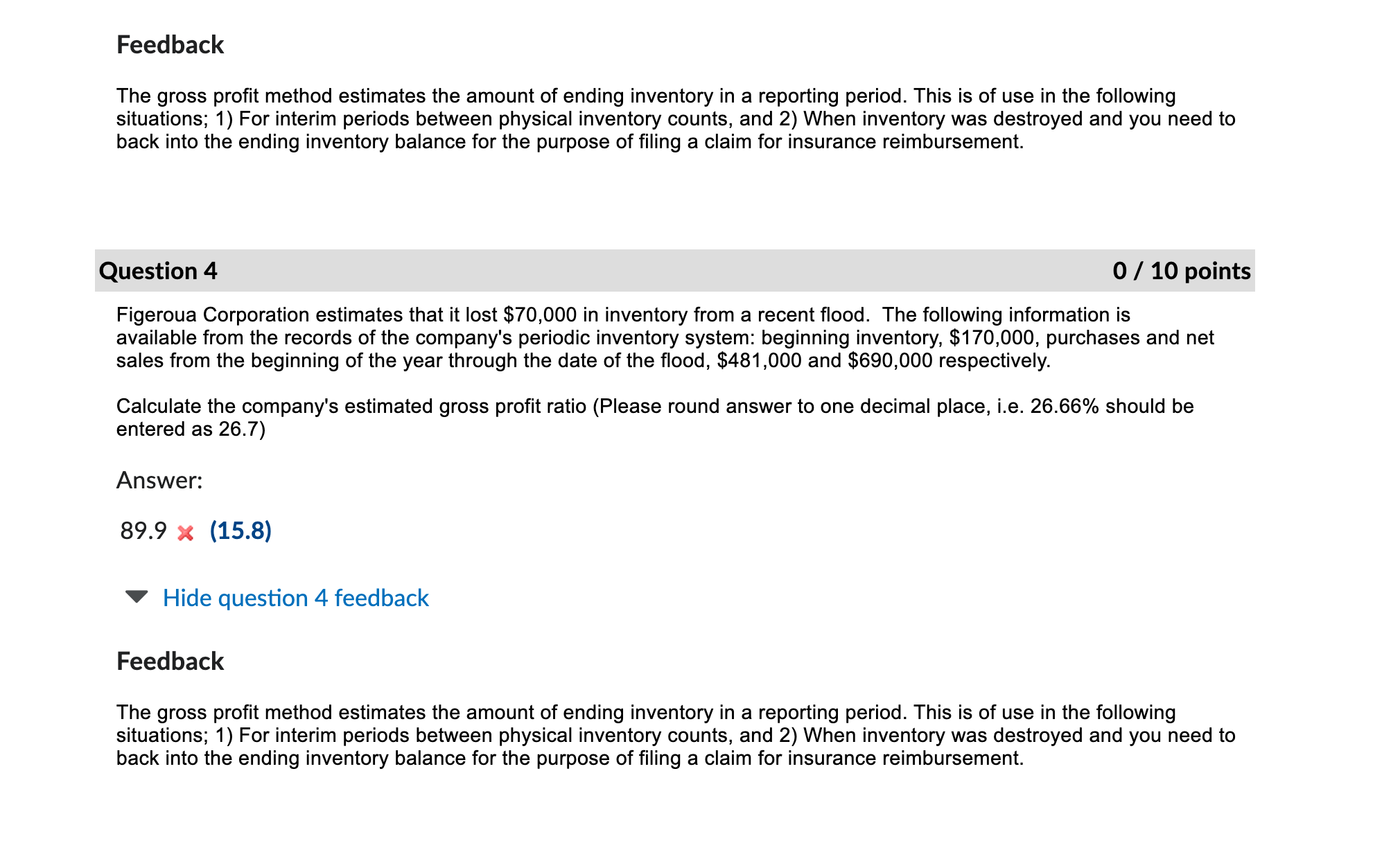

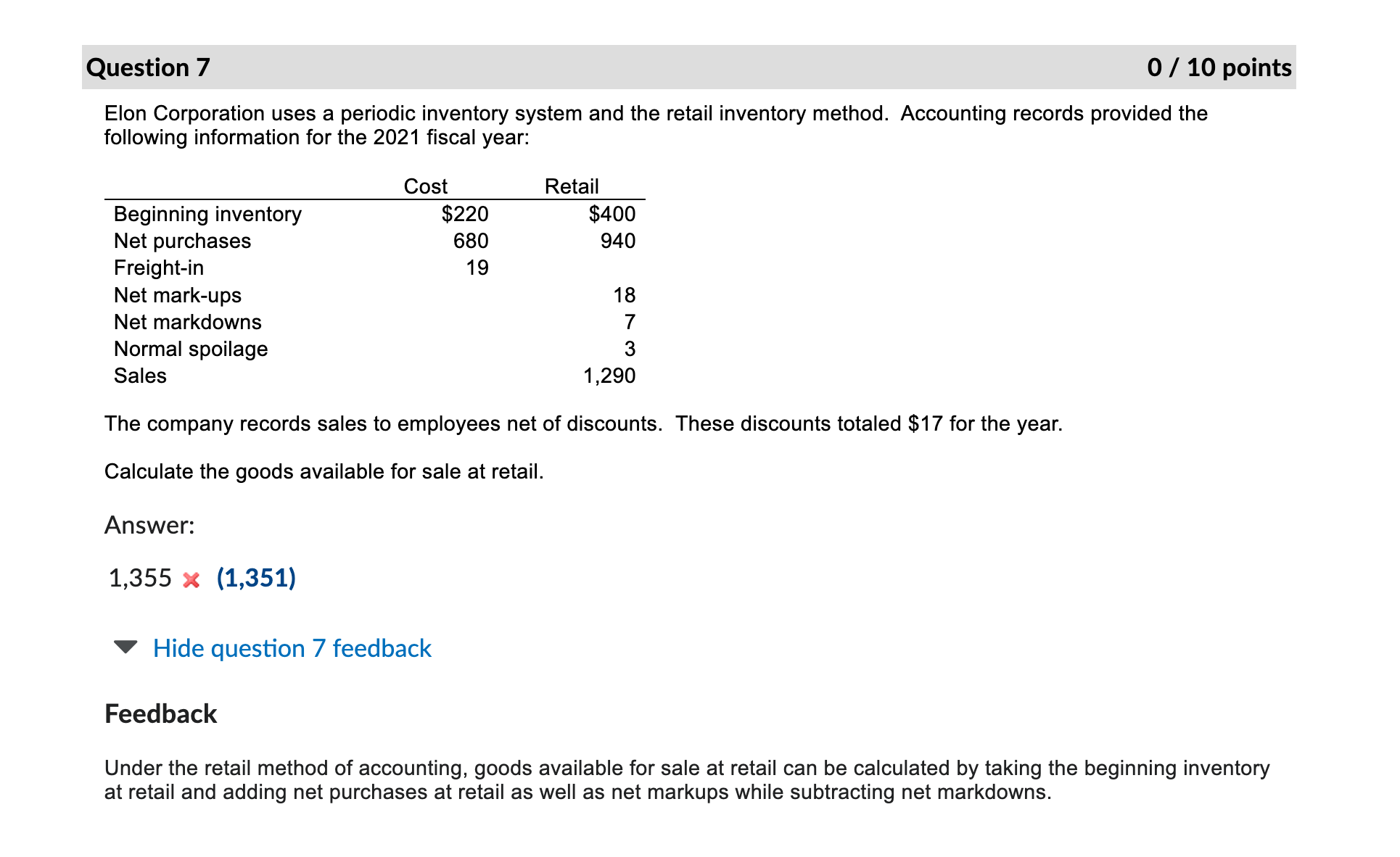

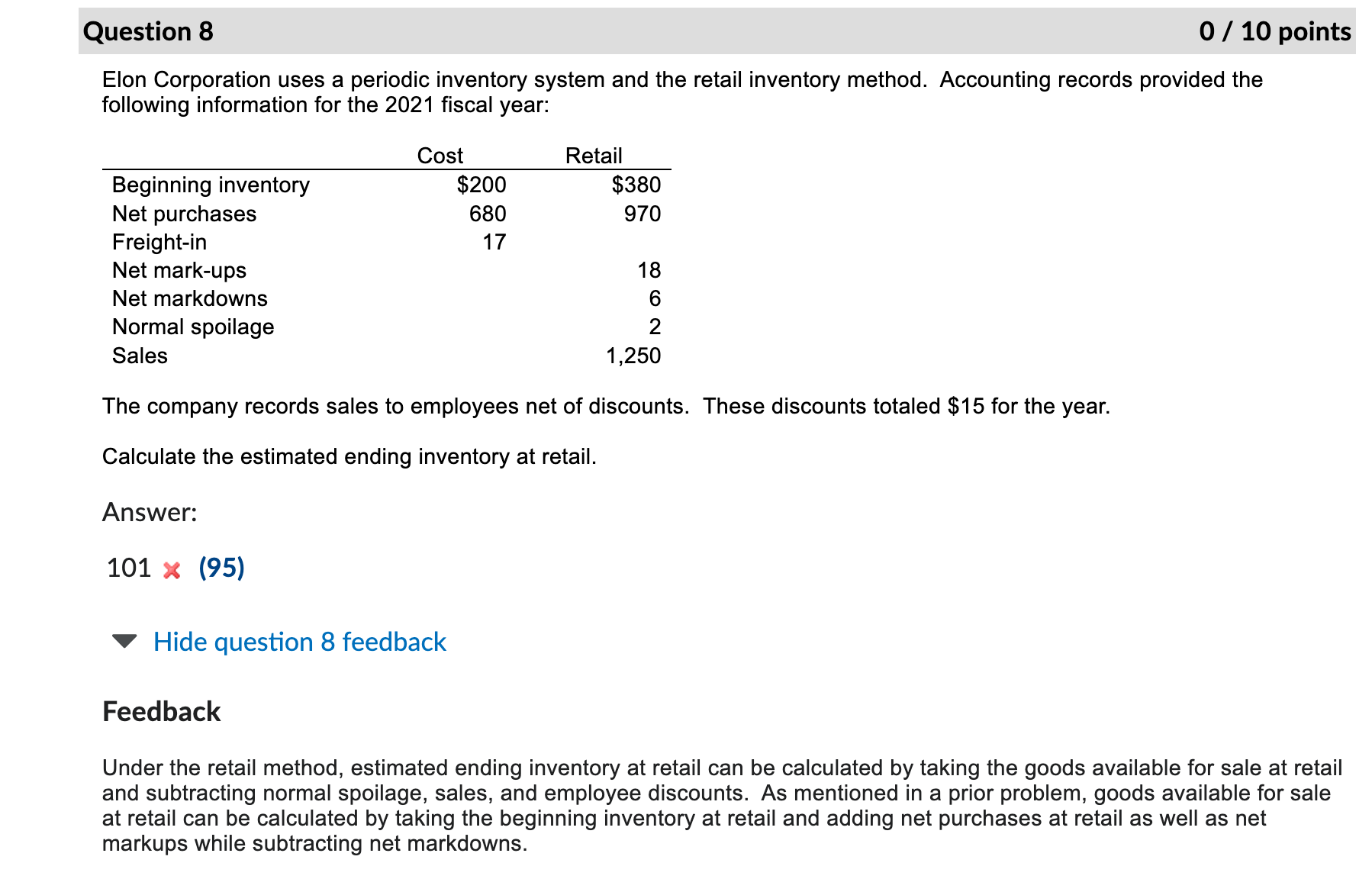

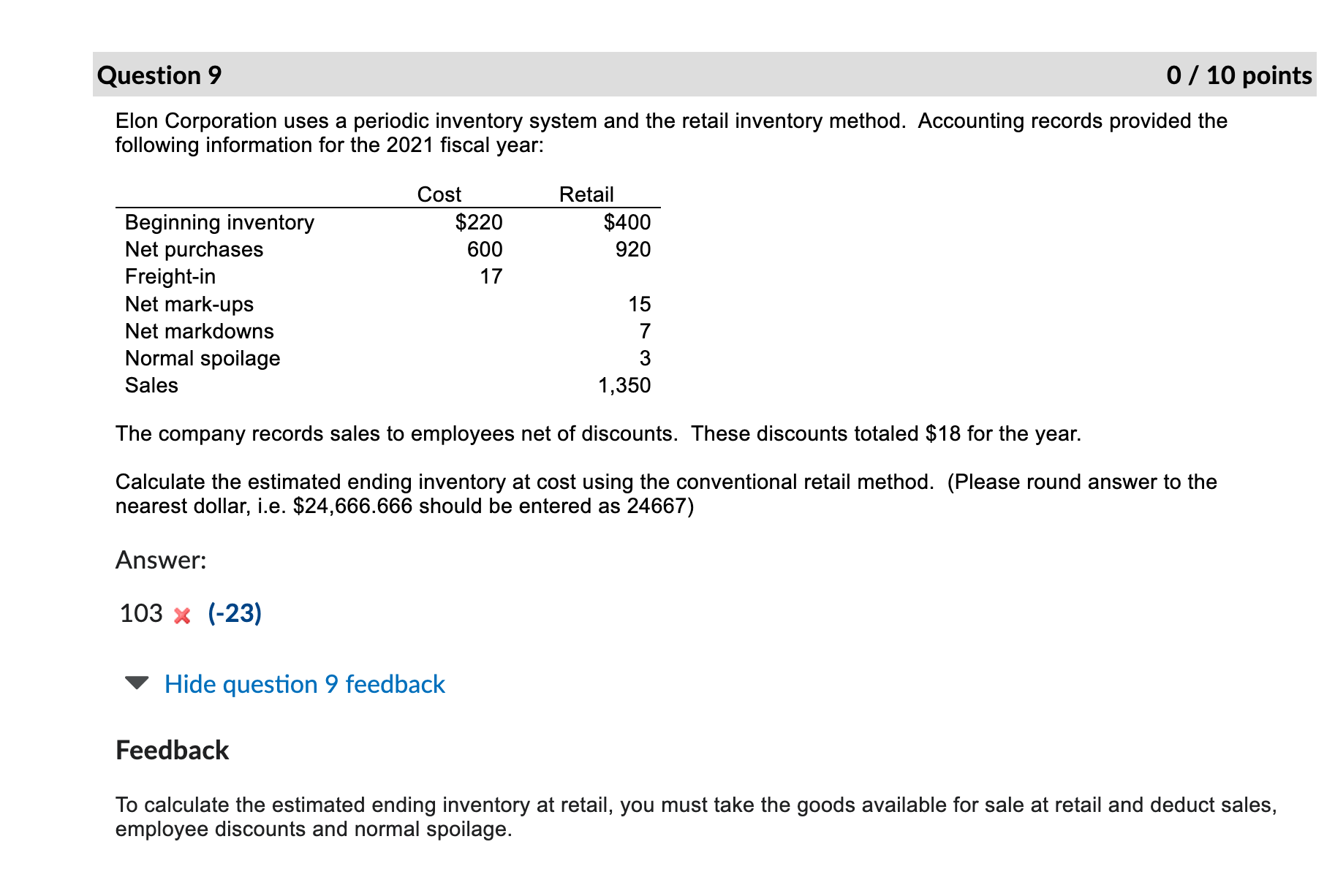

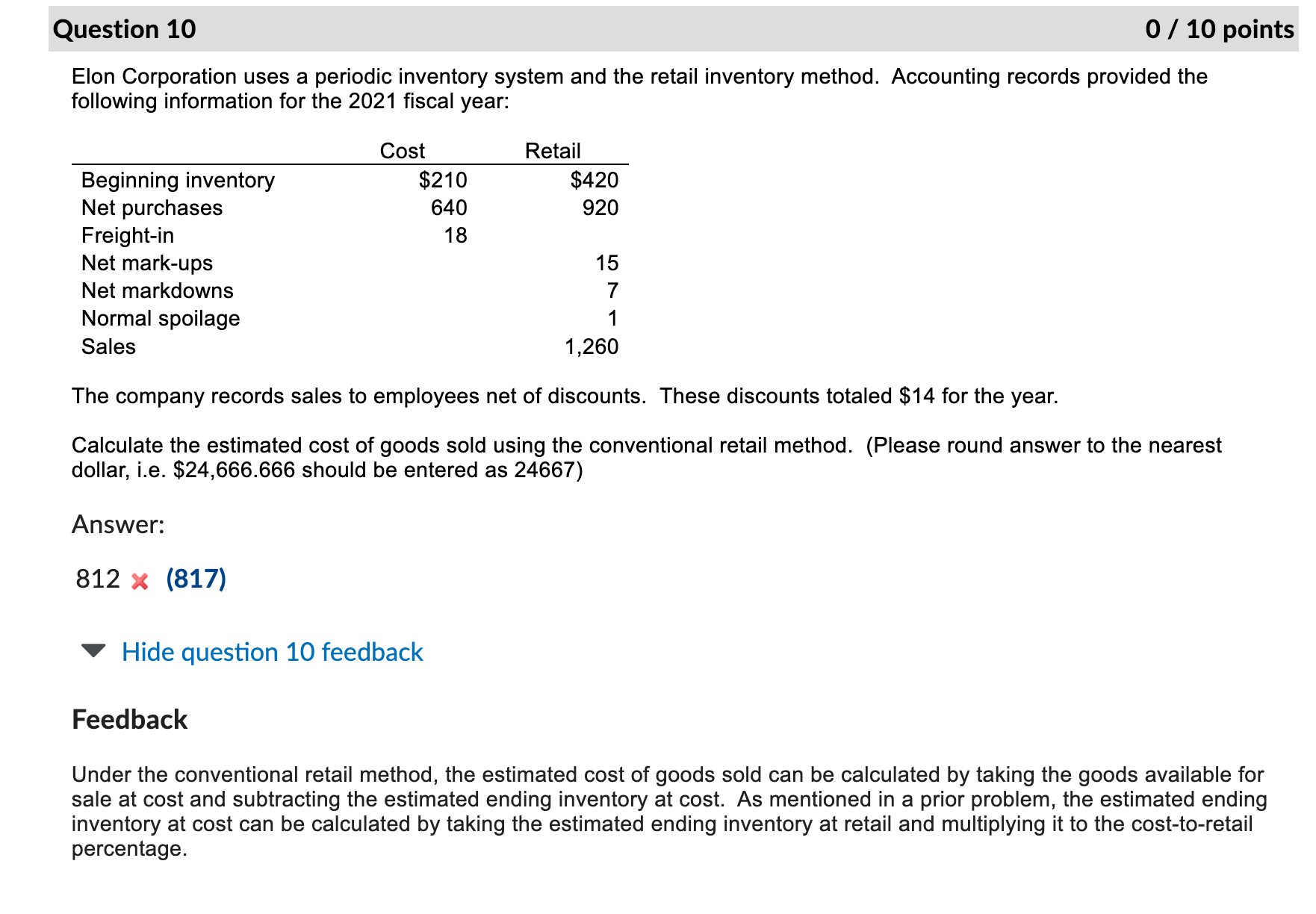

Question 2 0 / 10 points Figeroua Corporation estimates that it lost $90,000 in inventory from a recent flood. The following information is available from the records of the company's periodic inventory system: beginning inventory, $170,000, purchases and net sales from the beginning of the year through the date of the flood, $402,000 and $740,000 respectively. Calculate the company's estimated cost of goods sold. Answer: 90,000 % (482,000) Hide question 2 feedback Feedback The gross profit method estimates the amount of ending inventory in a reporting period. This is of use in the following situations; 1) For interim periods between physical inventory counts, and 2) When inventory was destroyed and you need to back into the ending inventory balance for the purpose of filing a claim for insurance reimbursement. Question 3 0/ 10 points Figeroua Corporation estimates that it lost $80,000 in inventory from a recent flood. The following information is available from the records of the company's periodic inventory system: beginning inventory, $150,000, purchases and net sales from the beginning of the year through the date of the flood, $459,000 and $650,000 respectively. Calculate the company's estimated gross profit. Answer: 570,000 % (121,000) Hide question 3 feedback Feedhack Feedback The gross profit method estimates the amount of ending inventory in a reporting period. This is of use in the following situations; 1) For interim periods between physical inventory counts, and 2) When inventory was destroyed and you need to back into the ending inventory balance for the purpose of filing a claim for insurance reimbursement. Question 4 0/ 10 points Figeroua Corporation estimates that it lost $70,000 in inventory from a recent flood. The following information is available from the records of the company's periodic inventory system: beginning inventory, $170,000, purchases and net sales from the beginning of the year through the date of the flood, $481,000 and $690,000 respectively. Calculate the company's estimated gross profit ratio (Please round answer to one decimal place, i.e. 26.66% should be entered as 26.7) Answer: 89.9 % (15.8) Hide question 4 feedback Feedback The gross profit method estimates the amount of ending inventory in a reporting period. This is of use in the following situations; 1) For interim periods between physical inventory counts, and 2) When inventory was destroyed and you need to back into the ending inventory balance for the purpose of filing a claim for insurance reimbursement. Question 7 0 / 10 points Elon Corporation uses a periodic inventory system and the retail inventory method. Accounting records provided the following information for the 2021 fiscal year: Cost Retail Beginning inventory $220 $400 Net purchases 680 940 Freight-in 19 Net mark-ups 18 Net markdowns 7 Normal spoilage 3 Sales 1,290 The company records sales to employees net of discounts. These discounts totaled $17 for the year. Calculate the goods available for sale at retail. Answer: 1,355 x (1,351) Hide question 7 feedback Feedback Under the retail method of accounting, goods available for sale at retail can be calculated by taking the beginning inventory at retail and adding net purchases at retail as well as net markups while subtracting net markdowns. Question 8 0 / 10 points Elon Corporation uses a periodic inventory system and the retail inventory method. Accounting records provided the following information for the 2021 fiscal year: Cost Retail Beginning inventory $200 $380 Net purchases 680 970 Freight-in 17 Net mark-ups 18 Net markdowns 6 Normal spoilage 2 Sales 1,250 The company records sales to employees net of discounts. These discounts totaled $15 for the year. Calculate the estimated ending inventory at retail. Answer: 101 x (95) Hide question 8 feedback Feedback Under the retail method, estimated ending inventory at retail can be calculated by taking the goods available for sale at retail and subtracting normal spoilage, sales, and employee discounts. As mentioned in a prior problem, goods available for sale at retail can be calculated by taking the beginning inventory at retail and adding net purchases at retail as well as net markups while subtracting net markdowns. Question 9 0 / 10 points Elon Corporation uses a periodic inventory system and the retail inventory method. Accounting records provided the following information for the 2021 fiscal year: Cost Retail Beginning inventory $220 $400 Net purchases 600 920 Freight-in 17 Net mark-ups 15 Net markdowns 7 Normal spoilage 3 Sales 1,350 The company records sales to employees net of discounts. These discounts totaled $18 for the year. Calculate the estimated ending inventory at cost using the conventional retail method. (Please round answer to the nearest dollar, i.e. $24,666.666 should be entered as 24667) Answer: 103 x (-23) Hide question 9 feedback Feedback To calculate the estimated ending inventory at retail, you must take the goods available for sale at retail and deduct sales, employee discounts and normal spoilage. Question 10 0/ 10 points Elon Corporation uses a periodic inventory system and the retail inventory method. Accounting records provided the following information for the 2021 fiscal year: Cost Retail Beginning inventory $210 $420 Net purchases 640 920 Freight-in 18 Net mark-ups 15 Net markdowns 7 Normal spoilage 1 Sales 1,260 The company records sales to employees net of discounts. These discounts totaled $14 for the year. Calculate the estimated cost of goods sold using the conventional retail method. (Please round answer to the nearest dollar, i.e. $24,666.666 should be entered as 24667) Answer: 812 x (817) Hide question 10 feedback Feedback Under the conventional retail method, the estimated cost of goods sold can be calculated by taking the goods available for sale at cost and subtracting the estimated ending inventory at cost. As mentioned in a prior problem, the estimated ending inventory at cost can be calculated by taking the estimated ending inventory at retail and multiplying it to the cost-to-retail percentage

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!