Question: Question 2 (1 point) You are given the following term structure of interest rates. S0(0.5) = 0.07, so(1) = 0.075, so(1.5) = 0.077, so(2) =

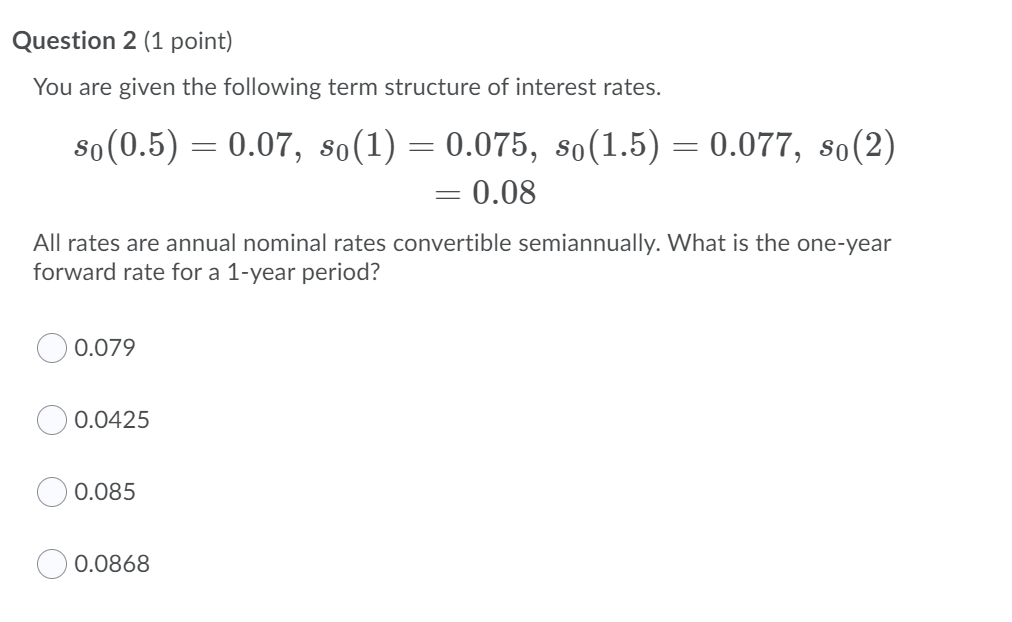

Question 2 (1 point) You are given the following term structure of interest rates. S0(0.5) = 0.07, so(1) = 0.075, so(1.5) = 0.077, so(2) = 0.08 All rates are annual nominal rates convertible semiannually. What is the one-year forward rate for a 1-year period? 0.079 0.0425 0.085 0.0868

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock