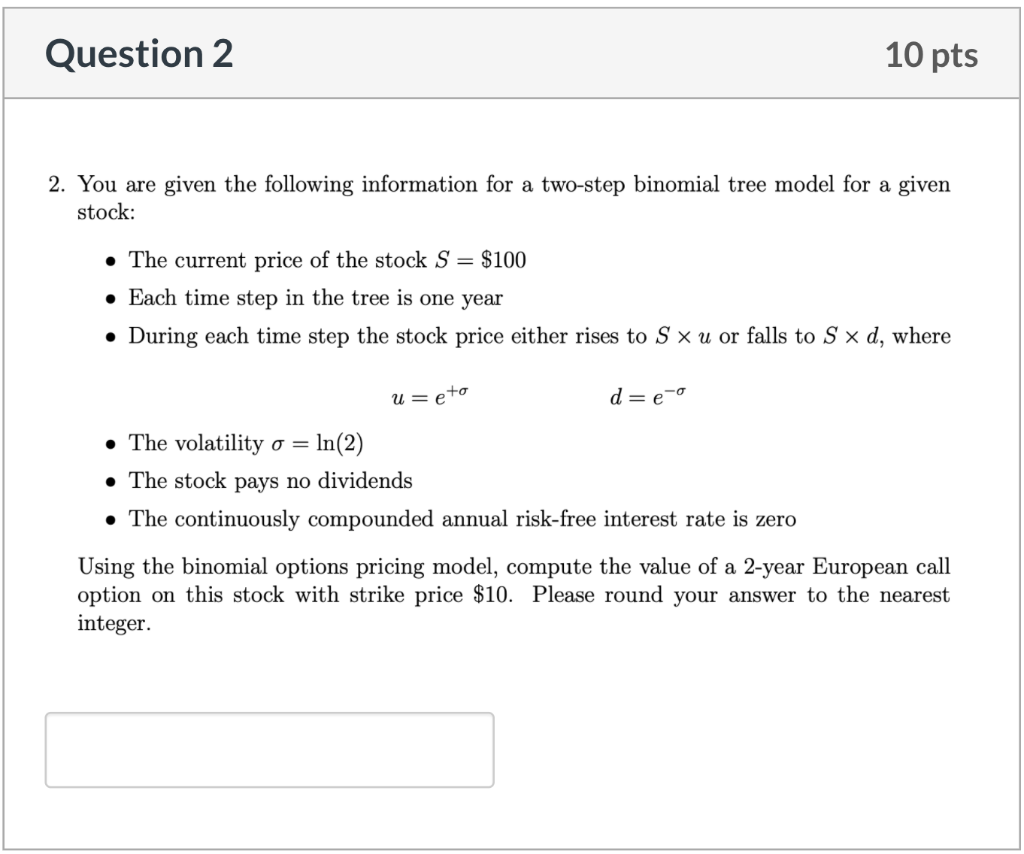

Question: Question 2 10 pts 2. You are given the following information for a two-step binomial tree model for a given stock: The current price of

Question 2 10 pts 2. You are given the following information for a two-step binomial tree model for a given stock: The current price of the stock S = $100 Each time step in the tree is one year During each time step the stock price either rises to S xu or falls to S x d, where u = eto d=e-o The volatility o = ln(2) The stock pays no dividends The continuously compounded annual risk-free interest rate is zero Using the binomial options pricing model, compute the value of a 2-year European call option on this stock with strike price $10. Please round your answer to the nearest integer

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock