Question: Question 2 (12 marks) Note that Question 2 has two parts - Part (A) and (B). Part (A) is not related to Part (B) Part

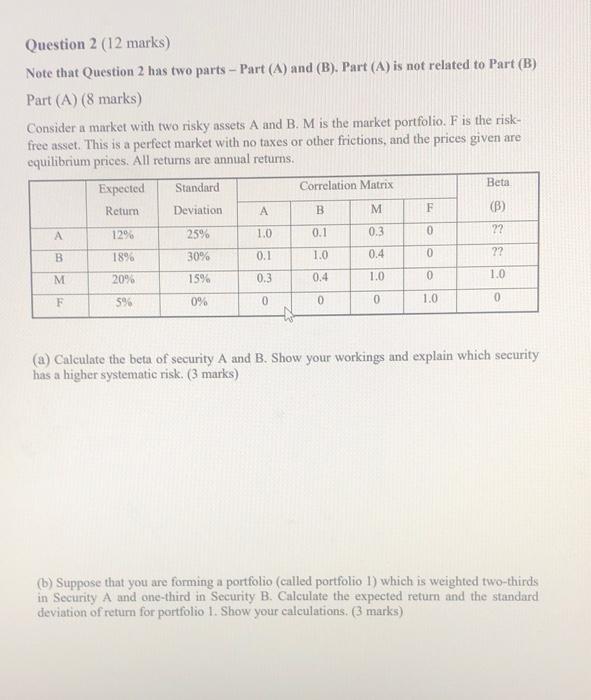

Question 2 (12 marks) Note that Question 2 has two parts - Part (A) and (B). Part (A) is not related to Part (B) Part (A) (8 marks) Consider a market with two risky assets A and B. M is the market portfolio. F is the risk- free asset. This is a perfect market with no taxes or other frictions, and the prices given are equilibrium prices. All returns are annual returns. Expected Beta Standard Correlation Matrix Retum Deviation B M F (B) 12% 25% A 1.0 0.1 0.3 0 22 B 18% 30% 0.1 1.0 ?? 0 0.4 M 2096 1596 0.3 0.4 1.0 1.0 0 5% 0% 0 0 0 1.0 0 (a) Calculate the beta of security A and B. Show your workings and explain which security has a higher systematic risk. (3 marks) (b) Suppose that you are forming a portfolio (called portfolio 1) which is weighted two-thirds in Security A and one-third in Security B. Calculate the expected return and the standard deviation of return for portfolio 1. Show your calculations. [3 marks) (c) Now suppose that the correlation between stock A and B was 0.01 instead of the number given in the table. Without doing any calculations explain what effect this would have on the return and standard deviation of your portfolio. (2 marks) I Part (B) (4 marks) Your investment portfolio consists of $15,000 invested in only one stock Apple. Suppose the risk-free rate is 5% Apple stock has an expected return of 12% and a volatility of 40% and the market portfolio has an expected return of 10% and a volatility of 18%. Under the CAPM assumptions, what investment has the highest possible expected return while having the same volatility as Apple? What is the expected return of this investment? (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts