Question: Question 2 (15 marks) An investor has a utility function of the form: U = E(r) 12A02. They have a risk-aversion coefficient of 4. The

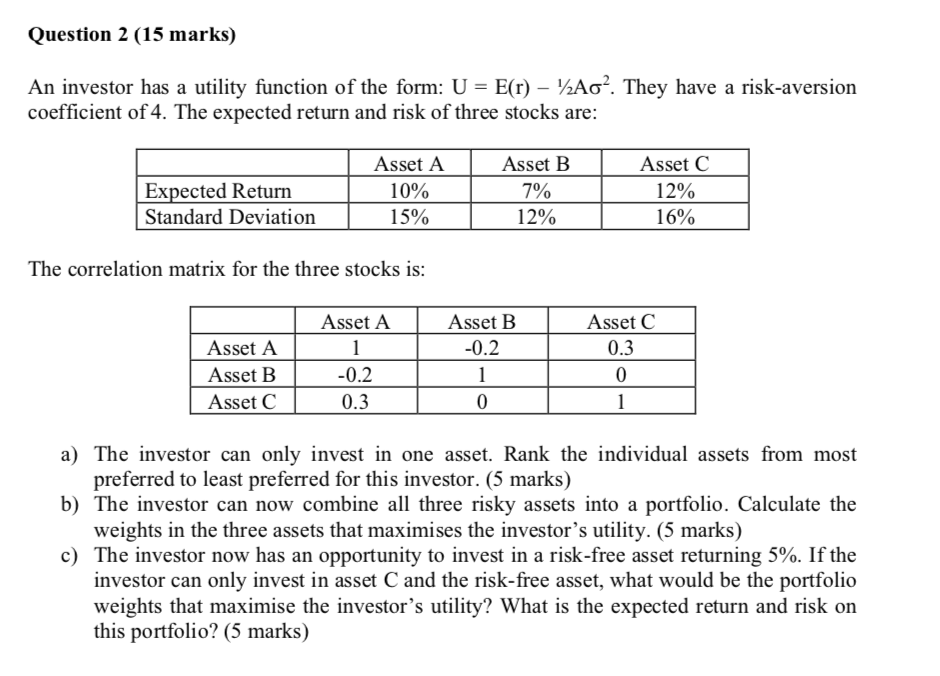

Question 2 (15 marks) An investor has a utility function of the form: U = E(r) 12A02. They have a risk-aversion coefficient of 4. The expected return and risk of three stocks are: Expected Return Standard Deviation Asset A 10% 15% Asset B 7% 12% Asset C 12% 16% The correlation matrix for the three stocks is: Asset A Asset B Asset C Asset A 1 -0.2 0.3 Asset B -0.2 1 0 Asset C 0.3 0 1 a) The investor can only invest in one asset. Rank the individual assets from most preferred to least preferred for this investor. (5 marks) b) The investor can now combine all three risky assets into a portfolio. Calculate the weights in the three assets that maximises the investor's utility. (5 marks) c) The investor now has an opportunity to invest in a risk-free asset returning 5%. If the investor can only invest in asset C and the risk-free asset, what would be the portfolio weights that maximise the investor's utility? What is the expected return and risk on this portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts