Question: Question 2 (20 marks) Listed below is a simplified balance sheet showing the dollar value and duration of assets and liabilities held. For ease

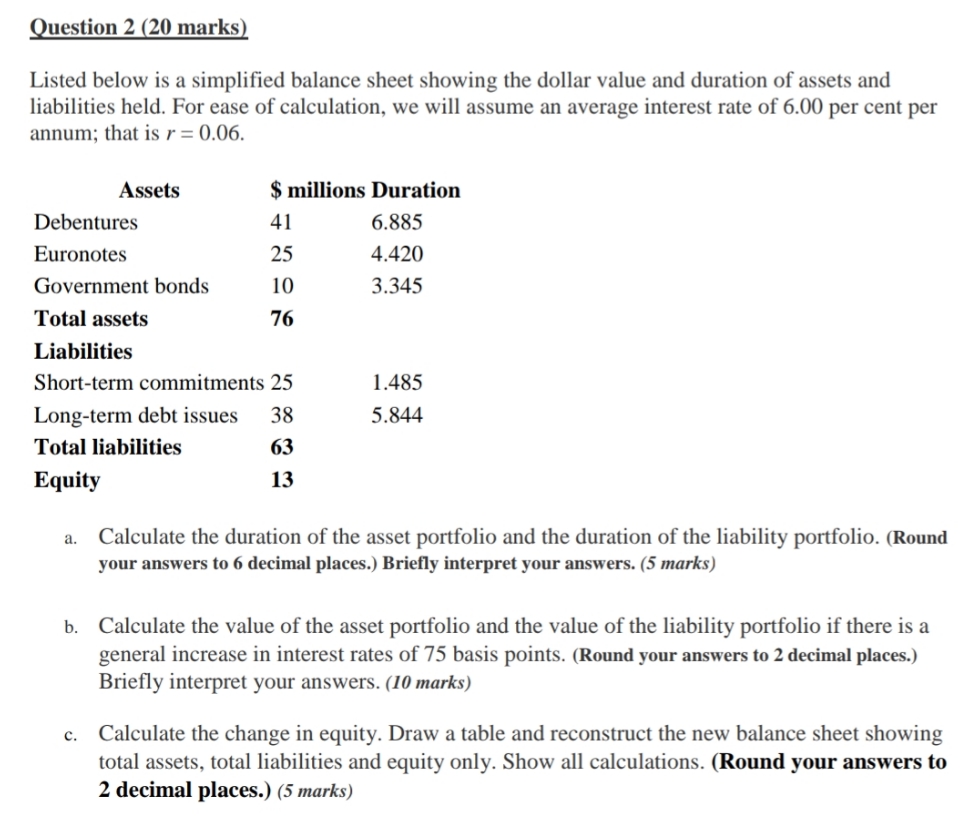

Question 2 (20 marks) Listed below is a simplified balance sheet showing the dollar value and duration of assets and liabilities held. For ease of calculation, we will assume an average interest rate of 6.00 per cent per annum; that is r = 0.06. $ millions Duration Assets Debentures 41 6.885 Euronotes 25 4.420 Government bonds 10 3.345 Total assets 76 Liabilities Short-term commitments 25 1.485 Long-term debt issues 38 5.844 Total liabilities 63 Equity a. 13 Calculate the duration of the asset portfolio and the duration of the liability portfolio. (Round your answers to 6 decimal places.) Briefly interpret your answers. (5 marks) b. Calculate the value of the asset portfolio and the value of the liability portfolio if there is a general increase in interest rates of 75 basis points. (Round your answers to 2 decimal places.) Briefly interpret your answers. (10 marks) C. Calculate the change in equity. Draw a table and reconstruct the new balance sheet showing total assets, total liabilities and equity only. Show all calculations. (Round your answers to 2 decimal places.) (5 marks)

Step by Step Solution

There are 3 Steps involved in it

Here are the calculations for the questions a Duration of asset portfolio Assets m Duration Debentur... View full answer

Get step-by-step solutions from verified subject matter experts