Question: Question 2 (25 credits) - start your answer on a new s Note: answers without explanation receive zero points Anton invests in a portfolio that

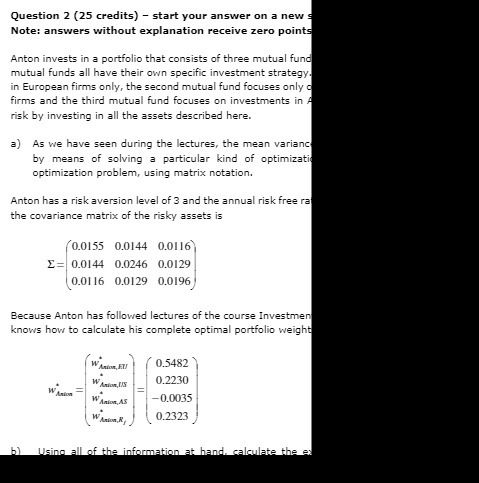

Question 2 (25 credits) - start your answer on a new s Note: answers without explanation receive zero points Anton invests in a portfolio that consists of three mutual fund mutual funds all have their own specific investment strategy, in European firms only, the second mutual fund focuses only c firms and the third mutual fund focuses on investments in A risk by investing in all the assets described here. ) As we have seen during the lectures, the mean varianc by means of solving a particular kind of optimizati optimization problem, using matrix notation. Anton has a risk aversion level of 3 and the annual risk free ra the covariance matrix of the risky assets is 0.0155 0.0144 0.0116 E= 0.0144 0.0246 0.0129 0.0116 0.0129 0.0196 Because Anton has followed lectures of the course Investment knows how to calculate his complete optimal portfolio weight WAsion, ET 0.5482 WAsion, US 0.2230 WAsion WAnion, AS -0.0035 0.2323 Using all I of the information at hand. calculate the ex

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts