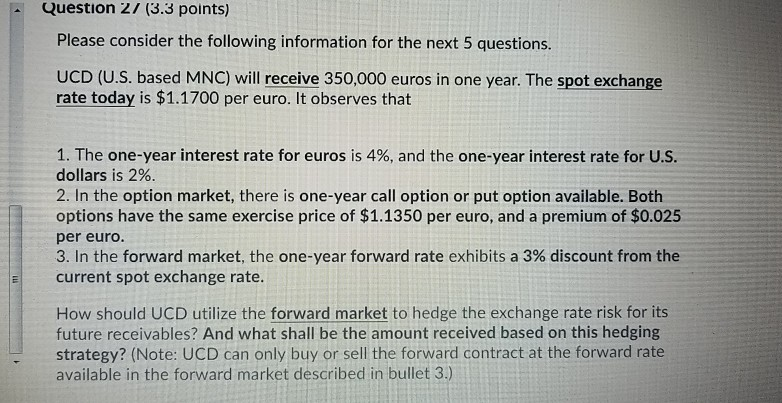

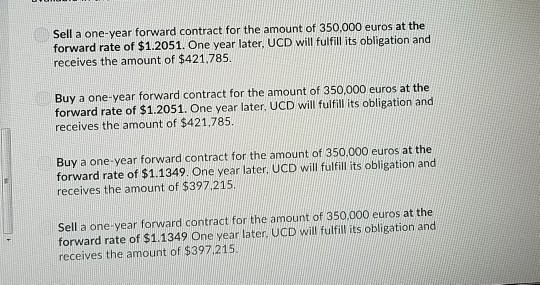

Question: Question 2/ (3.3 points) Please consider the following information for the next 5 questions. UCD (U.S. based MNC) will receive 350,000 euros in one year.

Question 2/ (3.3 points) Please consider the following information for the next 5 questions. UCD (U.S. based MNC) will receive 350,000 euros in one year. The spot exchange rate today is $1.1700 per euro. It observes that I. The one-year interest rate for euros is 4%, and the one-year interest rate for US. dollars is 2%. 2. In the option market, there is one-year call option or put option available. Both options have the same exercise price of $1.1350 per euro, and a premium of $0.025 per euro. 3. In the forward market, the one-year forward rate exhibits a 3% discount from the current spot exchange rate. How should UCD utilize the forward market to hedge the exchange rate risk for its future receivables? And what shall be the amount received based on this hedging strategy? (Note: UCD can only buy or sell the forward contract at the forward rate available in the forward market described in bullet 3.) Sell a one-year forward contract for the amount of 350.000 euros at the forward rate of $1.2051. One year later, UCD will fulfill its obligation and receives the amount of $421.785 Buy a one-year forward contract for the amount of 350.000 euros at the forward rate of $1.2051. One year later, UCD will fulfill its obligation and receives the amount of $421,785 Buy a one-year forward contract for the amount of 350,000 euros at the forward rate of $1.1349. One year later, UCD will fulfill its obligation and receives the amount of $397,215 Sell a one-year forward contract for the amount of 350,000 euros at the forward rate of $1.1349 One year later, UGD will fulfill its obligation and receives the amount of $397215

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts