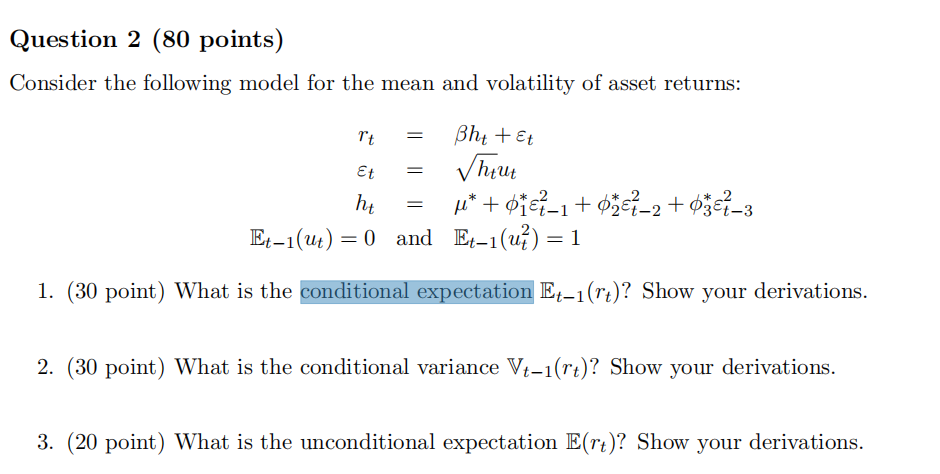

Question: Question 2 (80 points) Consider the following model for the mean and volatility of asset returns: rt = Et = Bht tet hut ht u*

Question 2 (80 points) Consider the following model for the mean and volatility of asset returns: rt = Et = Bht tet hut ht u* + 0167-1 + $767-2 +0367-3 Et1(ut) = 0 and Et-1(u) = 1 = = 1. (30 point) What is the conditional expectation Et-1(rt)? Show your derivations. 2. (30 point) What is the conditional variance Vt-1(rt)? Show your derivations. 3. (20 point) What is the unconditional expectation E(rt)? Show your derivations. Question 2 (80 points) Consider the following model for the mean and volatility of asset returns: rt = Et = Bht tet hut ht u* + 0167-1 + $767-2 +0367-3 Et1(ut) = 0 and Et-1(u) = 1 = = 1. (30 point) What is the conditional expectation Et-1(rt)? Show your derivations. 2. (30 point) What is the conditional variance Vt-1(rt)? Show your derivations. 3. (20 point) What is the unconditional expectation E(rt)? Show your derivations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts