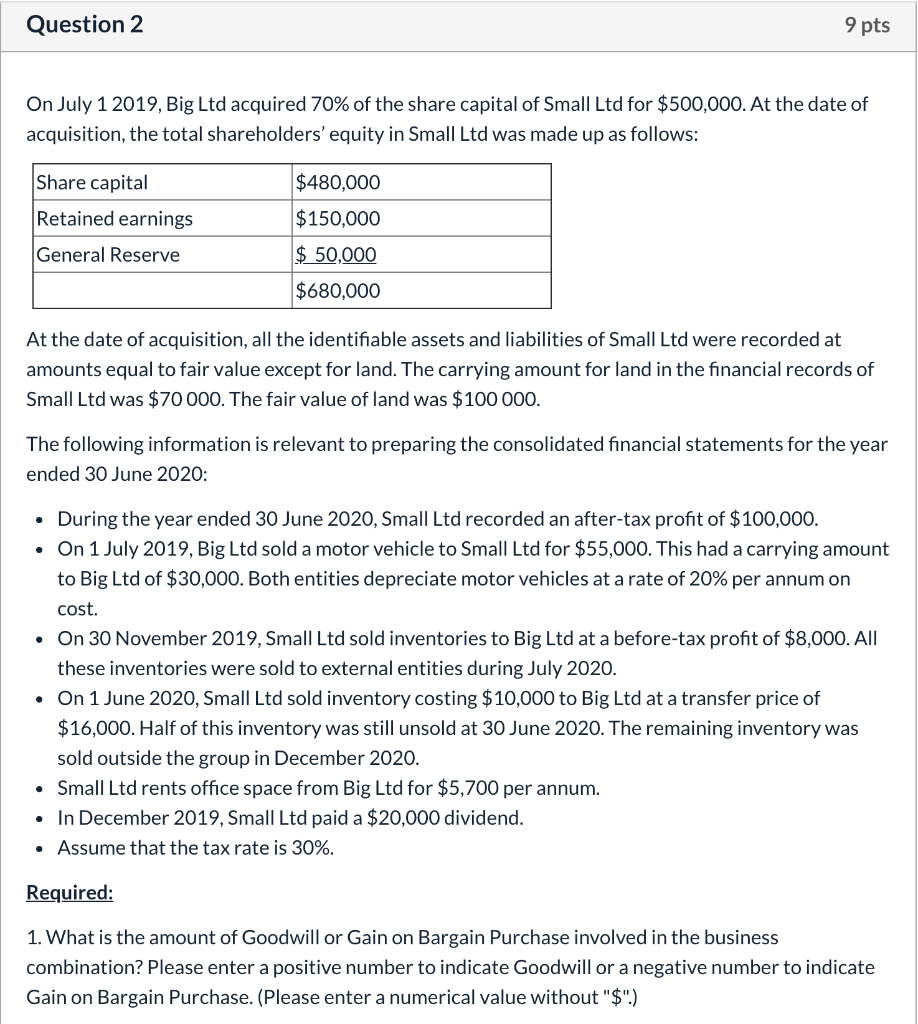

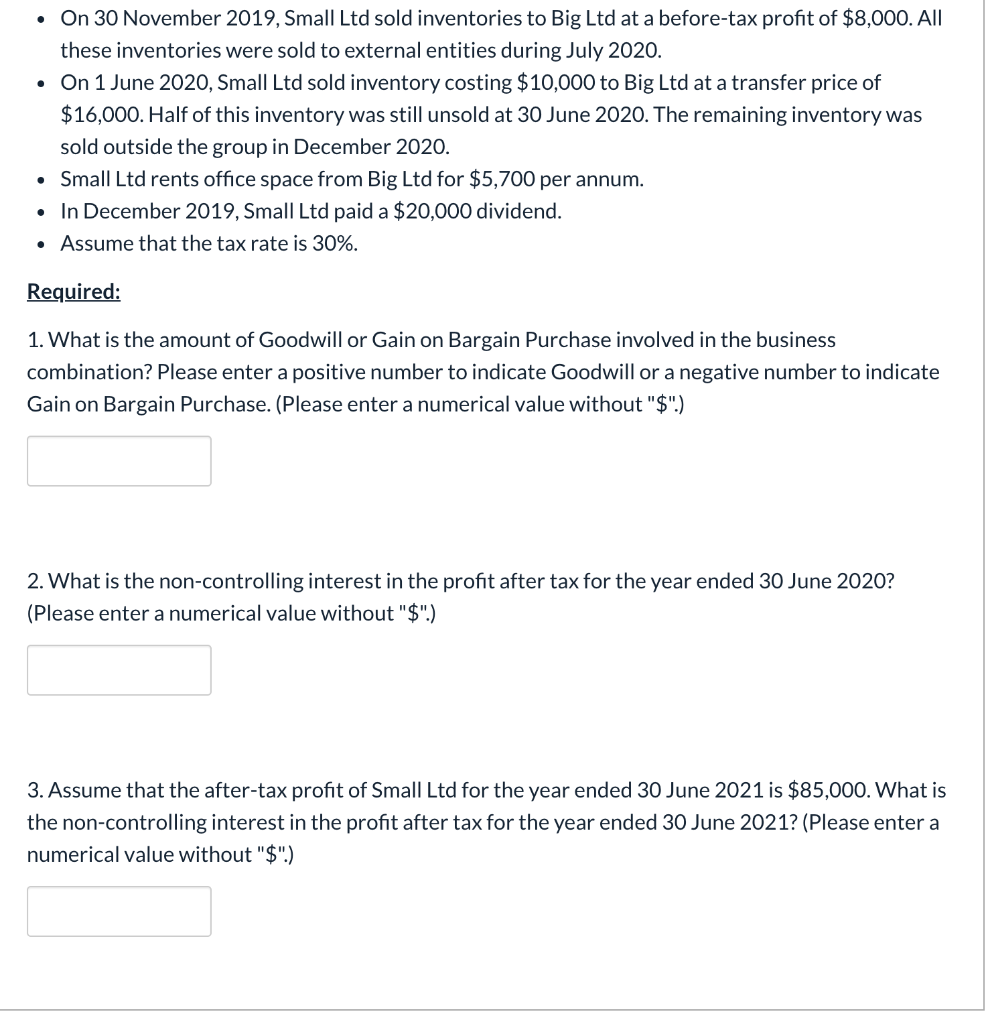

Question: Question 2 9 pts On July 1 2019, Big Ltd acquired 70% of the share capital of Small Ltd for $500,000. At the date of

Question 2 9 pts On July 1 2019, Big Ltd acquired 70% of the share capital of Small Ltd for $500,000. At the date of acquisition, the total shareholders' equity in Small Ltd was made up as follows: $480,000 Share capital Retained earnings $150,000 $ 50,000 General Reserve $680,000 At the date of acquisition, all the identifiable assets and liabilities of Small Ltd were recorded at amounts equal to fair value except for land. The carrying amount for land in the financial records of Small Ltd was $70 000. The fair value of land was $100 000. The following information is relevant to preparing the consolidated financial statements for the year ended 30 June 2020: During the year ended 30 June 2020, Small Ltd recorded an after-tax profit of $100,000. On 1 July 2019, Big Ltd sold a motor vehicle to Small Ltd for $55,000. This had a carrying amount to Big Ltd of $30,000. Both entities depreciate motor vehicles at a rate of 20% per annum on cost. On 30 November 2019, Small Ltd sold inventories to Big Ltd at a before-tax profit of $8,000. All these inventories were sold to external entities during July 2020. On 1 June 2020, Small Ltd sold inventory costing $10,000 to Big Ltd at a transfer price of $16,000. Half of this inventory was still unsold at 30 June 2020. The remaining inventory was sold outside the group in December 2020. Small Ltd rents office space from Big Ltd for $5,700 per annum. In December 2019, Small Ltd paid a $20,000 dividend. Assume that the tax rate is 30%. . . Required: 1. What is the amount of Goodwill or Gain on Bargain Purchase involved in the business combination? Please enter a positive number to indicate Goodwill or a negative number to indicate Gain on Bargain Purchase. (Please enter a numerical value without "$".) On 30 November 2019, Small Ltd sold inventories to Big Ltd at a before-tax profit of $8,000. All these inventories were sold to external entities during July 2020. On 1 June 2020, Small Ltd sold inventory costing $10,000 to Big Ltd at a transfer price of $16,000. Half of this inventory was still unsold at 30 June 2020. The remaining inventory was sold outside the group in December 2020. Small Ltd rents office space from Big Ltd for $5,700 per annum. In December 2019, Small Ltd paid a $20,000 dividend. Assume that the tax rate is 30%. Required: 1. What is the amount of Goodwill or Gain on Bargain Purchase involved in the business combination? Please enter a positive number to indicate Goodwill or a negative number to indicate Gain on Bargain Purchase. (Please enter a numerical value without "$") 2. What is the non-controlling interest in the profit after tax for the year ended 30 June 2020? (Please enter a numerical value without "$".) 3. Assume that the after-tax profit of Small Ltd for the year ended 30 June 2021 is $85,000. What is the non-controlling interest in the profit after tax for the year ended 30 June 2021? (Please enter a numerical value without "$") Question 2 9 pts On July 1 2019, Big Ltd acquired 70% of the share capital of Small Ltd for $500,000. At the date of acquisition, the total shareholders' equity in Small Ltd was made up as follows: $480,000 Share capital Retained earnings $150,000 $ 50,000 General Reserve $680,000 At the date of acquisition, all the identifiable assets and liabilities of Small Ltd were recorded at amounts equal to fair value except for land. The carrying amount for land in the financial records of Small Ltd was $70 000. The fair value of land was $100 000. The following information is relevant to preparing the consolidated financial statements for the year ended 30 June 2020: During the year ended 30 June 2020, Small Ltd recorded an after-tax profit of $100,000. On 1 July 2019, Big Ltd sold a motor vehicle to Small Ltd for $55,000. This had a carrying amount to Big Ltd of $30,000. Both entities depreciate motor vehicles at a rate of 20% per annum on cost. On 30 November 2019, Small Ltd sold inventories to Big Ltd at a before-tax profit of $8,000. All these inventories were sold to external entities during July 2020. On 1 June 2020, Small Ltd sold inventory costing $10,000 to Big Ltd at a transfer price of $16,000. Half of this inventory was still unsold at 30 June 2020. The remaining inventory was sold outside the group in December 2020. Small Ltd rents office space from Big Ltd for $5,700 per annum. In December 2019, Small Ltd paid a $20,000 dividend. Assume that the tax rate is 30%. . . Required: 1. What is the amount of Goodwill or Gain on Bargain Purchase involved in the business combination? Please enter a positive number to indicate Goodwill or a negative number to indicate Gain on Bargain Purchase. (Please enter a numerical value without "$".) On 30 November 2019, Small Ltd sold inventories to Big Ltd at a before-tax profit of $8,000. All these inventories were sold to external entities during July 2020. On 1 June 2020, Small Ltd sold inventory costing $10,000 to Big Ltd at a transfer price of $16,000. Half of this inventory was still unsold at 30 June 2020. The remaining inventory was sold outside the group in December 2020. Small Ltd rents office space from Big Ltd for $5,700 per annum. In December 2019, Small Ltd paid a $20,000 dividend. Assume that the tax rate is 30%. Required: 1. What is the amount of Goodwill or Gain on Bargain Purchase involved in the business combination? Please enter a positive number to indicate Goodwill or a negative number to indicate Gain on Bargain Purchase. (Please enter a numerical value without "$") 2. What is the non-controlling interest in the profit after tax for the year ended 30 June 2020? (Please enter a numerical value without "$".) 3. Assume that the after-tax profit of Small Ltd for the year ended 30 June 2021 is $85,000. What is the non-controlling interest in the profit after tax for the year ended 30 June 2021? (Please enter a numerical value without "$")

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts