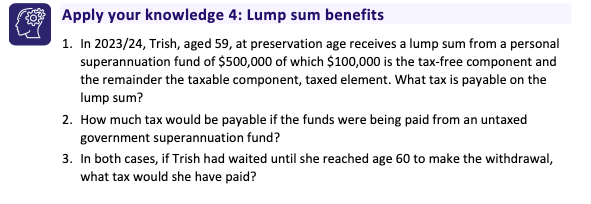

Question: Question 2 Apply your knowledge 4: Lump sum benefits 1. In 2023/24, Trish, aged 59, at preservation age receives a lump sum from a personal

Question 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock