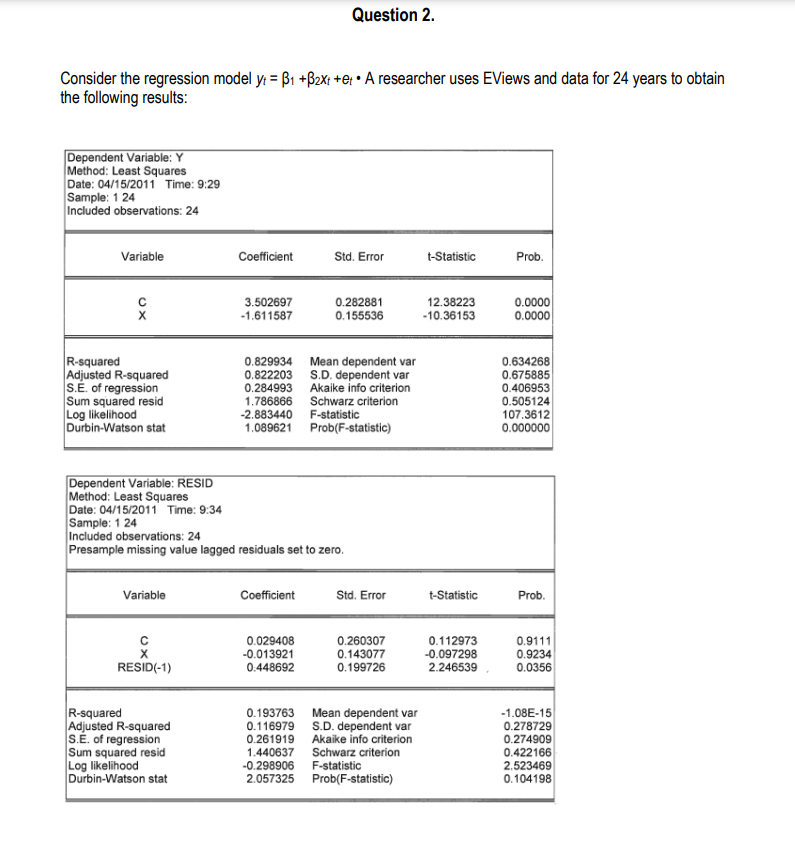

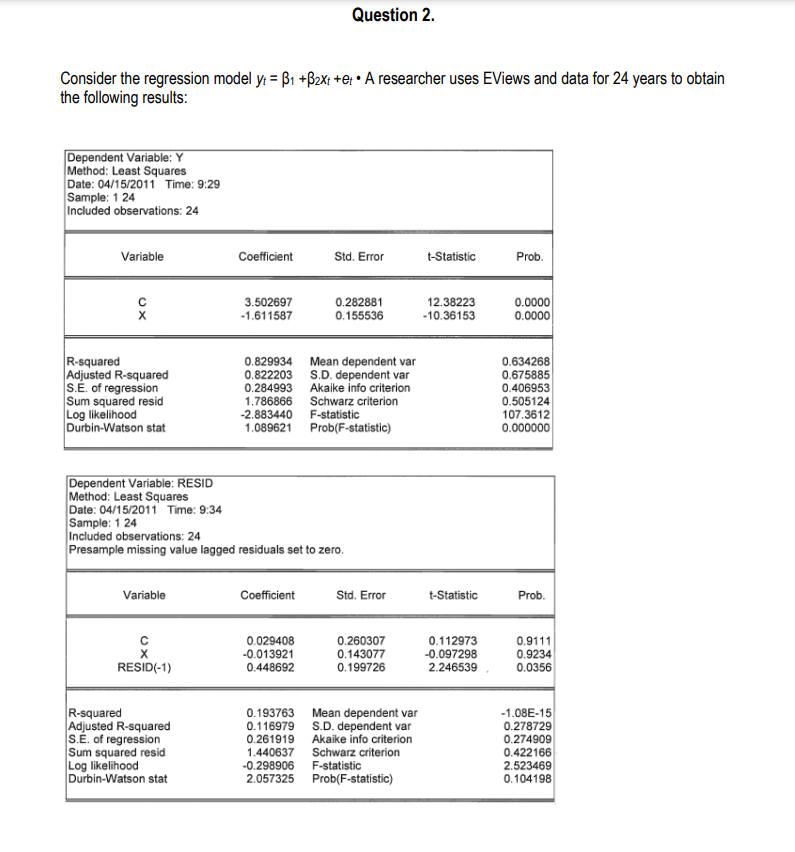

Question: Question 2. Consider the regression model yr = 1 +B2xt +er . A researcher uses EViews and data for 24 years to obtain the following

Question 2. Consider the regression model yr = 1 +B2xt +er . A researcher uses EViews and data for 24 years to obtain the following results: Dependent Variable: Y Method: Least Squares Date: 04/15/2011 Time: 9:29 Sample: 1 24 Included observations: 24 Variable Coefficient Std. Error t-Statistic Prob. 3.502697 0.282881 12.38223 0.0000 XO -1.611587 0.155536 -10.36153 0.0000 R-squared 0.829934 Mean dependent var 0.634268 Adjusted R-squared 0.822203 S.D. dependent var 0.675885 S.E. of regression 0.284993 Akaike info criterion 0.406953 Sum squared resid 1.78686 Schwarz criterion 0.505124 Log likelihood 2.883440 F-statistic 107.3612 Durbin-Watson stat 1.089621 Prob(F-statistic) 0.000000 Dependent Variable: RESID Method: Least Squares Date: 04/15/2011 Time: 9:34 Sample: 1 24 Included observations: 24 Presample missing value lagged residuals set to zero. Variable Coefficient Std. Error t-Statistic Prob C 0.029408 0.260307 0.112973 0.9111 -0.013921 0.143077 -0.097298 0.9234 RESID(-1) 0:448692 0.199726 2.246539 0.0356 R-squared 0.193763 Mean dependent var -1.08E-15 Adjusted R-squared 0.116979 S.D. dependent var 0.278729 S.E. of regression 0.261919 Akaike info criterion 0.274909 Sum squared resid 1.440637 Schwarz criterion 0.422166 Log likelihood -0.298906 F-statistic 2.523469 Durbin-Watson stat 2.057325 Prob(F-statistic) 0.104198Semester Two Final Examination 2023 ECN 3202 Applied Econometrics a) Conduct a Lagrange Multiplier test of the null hypothesis that the' errors are serially uncorrelated against the alternative that they follow an AR(1) process with p # 0. Use a 1% level of significance. Make sure you write out the null and alternative hypotheses in terms of p, the decision rule, the test statistic and your decision

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts