Question: Question 2 e MDL's property development sales contracts are accounted for through three related General Ledger accounts: contract assets, contract liabilities and contract costs. e

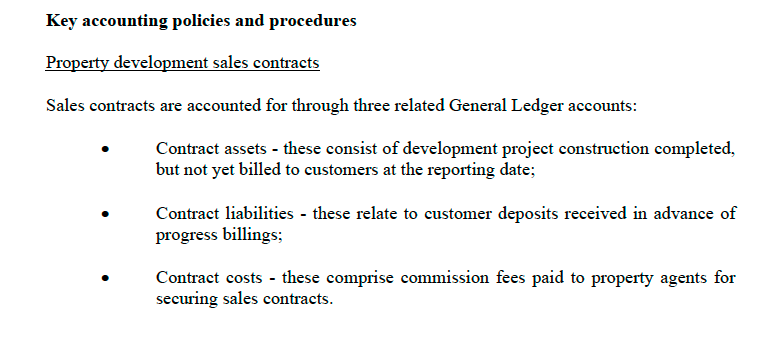

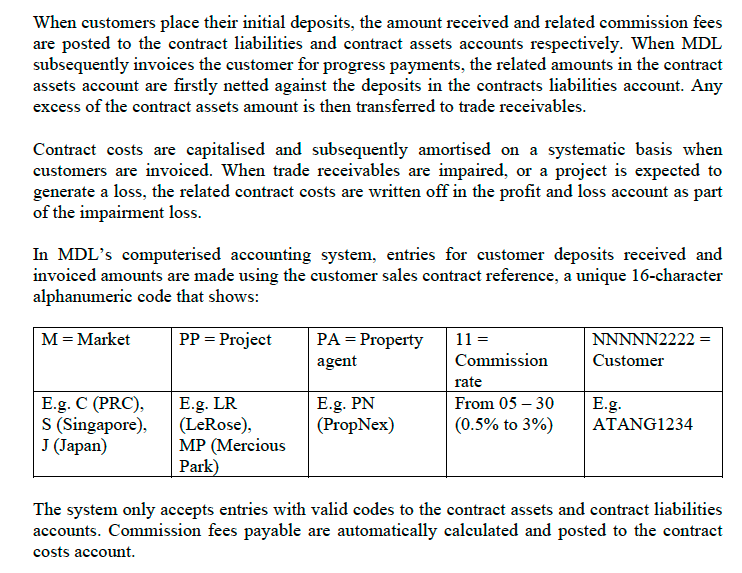

Question 2 e MDL's property development sales contracts are accounted for through three related General Ledger accounts: contract assets, contract liabilities and contract costs. e The system only accepts entries with valid 16-character alphanumeric codes to the contract assets and contract liabilities accounts. e Commission fees payable are automatically calculated and posted to the contract costs account. Question 2a Assess one (1) way the auditor can test the application controls for the contract accounts, using the test data method on the sales contract reference. (3 marks) Question 2b Design and explain: e One (1) test data set to check that commission fees payable are only posted for valid property agents, and correctly calculated. e One (1) test data set to check that invoiced amounts for progress payments are correctly posted to the contract liabilities and trade receivables accounts. Each test data set should include one valid transaction and one invalid transaction. (12 marks) Question 2 Using the sales contract reference ID, appraise how the auditor can use data analytics to check that: e All commission fees have been amortised from the contract costs account for fully completed development projects. e All commission fees have been written off from the contract costs account for customer contracts that have been impaired. (8 marks) CASE Metropolis Developments Limited (MDL) is a leading international real estate company based in Smgapore. Over more than 45 years, it has established a strong reputation for high quality residential and commercial developments. Singapore is MDL's core market, comprising 50% of its total assets and 60-65% of revenue. In the last 10 years, the company has also expanded into the People's Republic of China (PRC). the United Kingdom (UK). Japan, Australia, and Vietnam. Through subsidiaries, associates and joint ventures, it operates in over 50 locations in these markets. MDL 1s listed on the Singapore Exchange (SGX). and regarded as one of the best property development companies in the Singapore market. Its financial year-end is March 31. Business segments and revenue MDL's operations fall into two broad segments: . Property development, which mvolves developing and purchasing properties for sale. The Group develops and sells residential and mixed development projects to customers through fixed-price contracts. Revenue from such contracts 1s usually recognised over time, based on the stage of completion of the project, as determined through certification by quantity surveyors. . Investment properties, which involves developing and purchasing properties for rent. The Group leases out serviced apartments as well as commercial and retail properties., with rental income recognised on a straight-line basis over the related lease term. Key accounting policies and procedures Property development sales contracts Sales contracts are accounted for through three related General Ledger accounts: . Contract assets - these consist of development project construction completed, but not yet billed to customers at the reporting date; . Contract liabilities - these relate to customer deposits received in advance of progress billings: . Contract costs - these comprise commission fees paid to property agents for securing sales contracts. When customers place their initial deposits, the amount received and related commaission fees are posted to the contract liabilities and contract assets accounts respectively. When MDL subsequently invoices the customer for progress payments, the related amounts in the contract assets account are firstly netted against the deposits in the contracts liabilities account. Any excess of the contract assets amount 1s then transferred to trade receivables. Contract costs are capitalised and subsequently amortised on a systematic basis when customers are invoiced. When trade receivables are impaired, or a project is expected to generate a loss, the related contract costs are written off in the profit and loss account as part of the impairment loss. In MDL's computerised accounting system. entries for customer deposits received and invoiced amounts are made using the customer sales contract reference. a unique 16-character alphanumeric code that shows: PP = Project PA = Property 11 = NNNNN2222 = agent Commission Customer rate E.g. C (PRO), E.g. LR From 05 30 E.g. S (Singapore), | (LeRose), (0.5% to 3%) ATANGI1234 J (Japan) MP (Mercious The system only accepts entries with valid codes to the contract assets and contract liabilities accounts. Commission fees payable are automatically calculated and posted to the contract costs account. Valuation of development and investment properties The carrying amounts of the Group's development and investment properties are reviewed at each reporting date to determine if there is any indication of impairment. If so, the recoverable amounts of assets are estimated (being the greater of value in use, and fair value): and where the recoverable amount 1s less than the carrying amount, impairment loss 1s recognised in the profit and loss account. MDL obtains external valuations from independent qualified professionals every year for its mvestment properties, and every two years for its development properties. In the interim periods, the valuation of development properties 1s conducted by management. Impact of the COVID-19 pandemic The pandemic caused massive disruption and long-term challenges to the entire property sector, and MDL was not spared any of the effects. Lockdowns. movement controls and safe management measures had mmmediate and continuing impacts on the launches of its development projects. Work from home practices affected the occupancy and footfall of its residential, commercial and retail investment properties. MDL revenue for the financial year to March 31 202y was $1.19b, down from $1.42b for the previous year. Property development MDL stepped up digital marketing practices such as virtual showflat tours and online sales presentations to maintain business continuity and improve customer accessibility. Through such efforts, its LeRose development was Singapore's best-selling property launch for Q4 202x, selling 60% of units during the launch weekend. Despite this success, revenue from this segment was badly affected by slower construction progress. which slowed down customer billing. Profitability also fell, as more billings came from mid-range projects with lower margins compared to the higher-range projects launched in 202x. Shortage of foreign workers and disruption in the supply of built components and raw materials are expected to continue to delay project completions by up to 12 months, and inerease costs by 15-30% beyond MDL's original budgets. Going forward, job losses and patchy economic recovery might affect the collectability of progress payments billed to customers. Increased uncertainty in the global economic outlook. government policies and market sentiment could also lead to future trends departing from known trends, thus affecting the value of MDL's ongoing projects and land banks. The current carrying value of MDL's unsold development properties could potentially exceed the eventual selling price, resulting in unforeseen losses when these properties are sold. This situation is more likely for development properties with lower profit margins., Investment properties Despite travel restrictions, border closures and a generally subdued outlook, MDL maintained its average occupancy rate at above the national average across its different markets. However, revenue for this segment was reduced by rental rebates of $29m that MDL provided to retail tenants. Higher financing costs also affected profit. Investment in Joint Venture In April 202x, MDL acquired a 51.03% controlling interest in Trustworth Property Group (TW), to expand MDL's product offerings in key cities in the PRC, and establish its position as a major player in the PRC property market. However, TW's liquidity position was subsequently severely impacted by the effects of the COVID-19 pandemic on the PRC economy, and the PRC government measures to cap borrowings for all PRC real estate companies. MDL's initial investment in TW of $800m is accounted for as a joint venture. In September 202x, it extended a $250m working capital loan to help TW manage its worsening liquidity position. In December 202x MDL also provided a financial guarantee of $255m for a loan that TW obtained from a PRC financial institution.Events after the balance sheet date Valuation of development and investment properties Given the uncertainty in economic and market conditions, MDL management obtained external valuations for all its development and investment properties at March 31 202y. . The valuations for development properties were based on assumptions about future selling prices compared to prices of recent transactions, and prices of comparable projects in the vicinity of MDL's developments. . The valuations for investment properties considered the occupancy rates and market rates for similar properties. Based on the valuations obtained, MDL has written off $35m for foreseeable losses on property development projects. and provided for an impairment loss of $100m for its mvestment properties. The external valuation reports highlighted the heightened level of uncertainty in the global economy, such that more caution should be exercised in making judgements based on the valuations provided. and recommended that valuations be reviewed more frequently for both types of properties. Investment in and balances with Joint Venture TW failed to repay certain of its loans and bonds that fell due in Q1 of 202y. MDL's Board of Directors expressed serious concerns regarding MDL's imtial investment and subsequent financial support for TW. In response, MDL senior management engaged an mndependent valuation expert to assess the fair value of net assets acquired in TW. The valuation report indicated that MDL's $800m investment should be reclassified as goodwill. Management have separately evaluated TW's debt maturity profile, past repayment trends, default risk on amounts owed and liqumidity challenges. It has concluded that the working capital loan of $250m is credit-impaired; and the financial guarantee of $255m provided for TW's loan will probably be invoked. Senior management are considering measures to improve TW's hiqudity and profitability while limiting any further financial exposure for MDL. It believes there is potential to divest some of TW's assets and restructure its liabilities to lighten its debt load. However. such divestment will likely take longer to realise, due to the challenging macro-economic environment and the credit tightening measures imposed on the real estate sector i the PRC. Audit matters External auditor MDL's external auditor is one of the Big Four accounting firms. The fee for the 202y audit has been agreed at $2.9m. During the year, the firm has also provided various non-audit services to MDL, with total fees amounting to $1.4m. MDL senior management has approached the external auditor to review the TW investment, in order to identify assets that are profitable and generating positive cash flow, assets that can be realised to improve liquidity, and assets that present feasible options to improve profitability. The review should also identify any major bank loans and non-trade liabilities maturing in 202y and 202z that require debt restructuring. Significant components and component auditors All MDL's components are considered significant, either because of their contribution to group revenue and profits, or because the nature of their business (property development and/or investment properties) are likely to include significant risks of material misstatement in the group financial statements. MDL's subsidiaries in all the markets in which 1t operates are audited by the network firms of MDL's external auditor. All of MDL's associated companies and joint venture partners are audited by one of the Big Four accounting firms. Due to restrictions arising from the COVID-19 pandemic, the external auditor 1s unable to travel to any of MDL's other markets to review the component auditors' audit documentation. Audit Committee MDL's Audit Committee (AC) comprises three non-executive, independent directors. The AC assists the Board of Directors to perform an independent review of the adequacy and effectiveness of MDL's financial reporting process, including: Accounting policies and practices and key internal controls for finance, operations, compliance, IT and risk management; Scope and results of the financial statement audit, the independence and objectivity of the external auditors, and the nature and extent of non-audit services provided during the year. MDL GROUP: KEY FINANCIAL INFORMATION (EXTRACTS) For years ending March 31 NOTE: The 202y draft financial information shown below includes MDL's $800m inves in its PRC joint venture TW. No adjustment has yet been made to impair this investment $250 working capital loan made by MDL, or to reflect the financial guarantee of $255m by MDL for TW's loan from a financial institution in the PRC. Note 202y (draft) 202x (audited) $m Sm Revenue 1,194.6 1,417.3 Items (charged) / reversed include: Impairment on investment properties (100.0) 2.4 Foreseeable loss on development properties (35.0) 6.5 Fees paid to MDL auditors - Audit fees (2.9) (2.8) Non-audit fees (1.4) (1.5) Impairment for trade receivables (25.2) (14.3) Profit before tax 320.0 639.9 Noncurrent assets include Development properties 266.0 96.3 Investment properties 4,111 8 3,969.2 Investment in - Associates 636.9 506.6 Joint ventures 1,702.5 1,073.2 Current assets include Development properties 4,851 9 4,640.1 Contract costs 28.5 23.5 Contract assets 454.7 217.8 Trade & other receivables 1,763.1 739.9 Why Cash & cash equivalents 2,813.9 2,517.9 Total assets 21,309.1 20,880.2 Owners' equity 9,272.0 9,458.2 Non-controlling interests 666.2 671.7 Non-current borrowings 8,756.1 7,673.2 Current liabilities include Trade & other payables 1,213.9 1,079.0 Contract liabilities 240.8 188.6 Current borrowings 2,798.6 2,038.0 Total equity and liabilities 21,309.1 20,880.2Note 1: Segment information Business segment 202y (draft) 202x (audited) $m $m Property development 869.3 1023.0 Investment properties 325.3 394.3 Revenue 1,194.6 1,417.3 Property development 197.8 340.3 Investment properties 122.2 299.6 Profit before tax 320.0 639.9 Geographical segment 202y (draft) 202x (audited) $m $m Singapore 776.5 850.9 UK 124.2 187.7 PRC 68.4 95.8 Japan, Australia & Vietnam 225.5 282.9 Revenue 1,194.6 1,417.3 Note 2: Trade & other receivables includes: 202y (draft) 202x (audited) $m $m Trade receivables 172.3 171.6 Impairment loss on trade receivables (25.2) (14.3) Amounts owing by joint ventures 1,490.0 500.8 The impairment loss on trade receivables was charged according to MDL's accounting policy to provide for all receivable balances outstanding for more than six months at the reporting date. The amounts owing by joint ventures includes the $250m working capital loan given to TW in September 202x. Note 3: Cash & cash equivalents of $2.8b comprise fixed deposits, cash at bank and cash in hand. MDL also holds undrawn committed bank facilities of S$4.2b

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!