Question: QUESTION 2 PART A (continued) Marks Discuss, with reasons. the appropriate accounting treatment and disclosure requirements for the matters referred to in additional information (5)

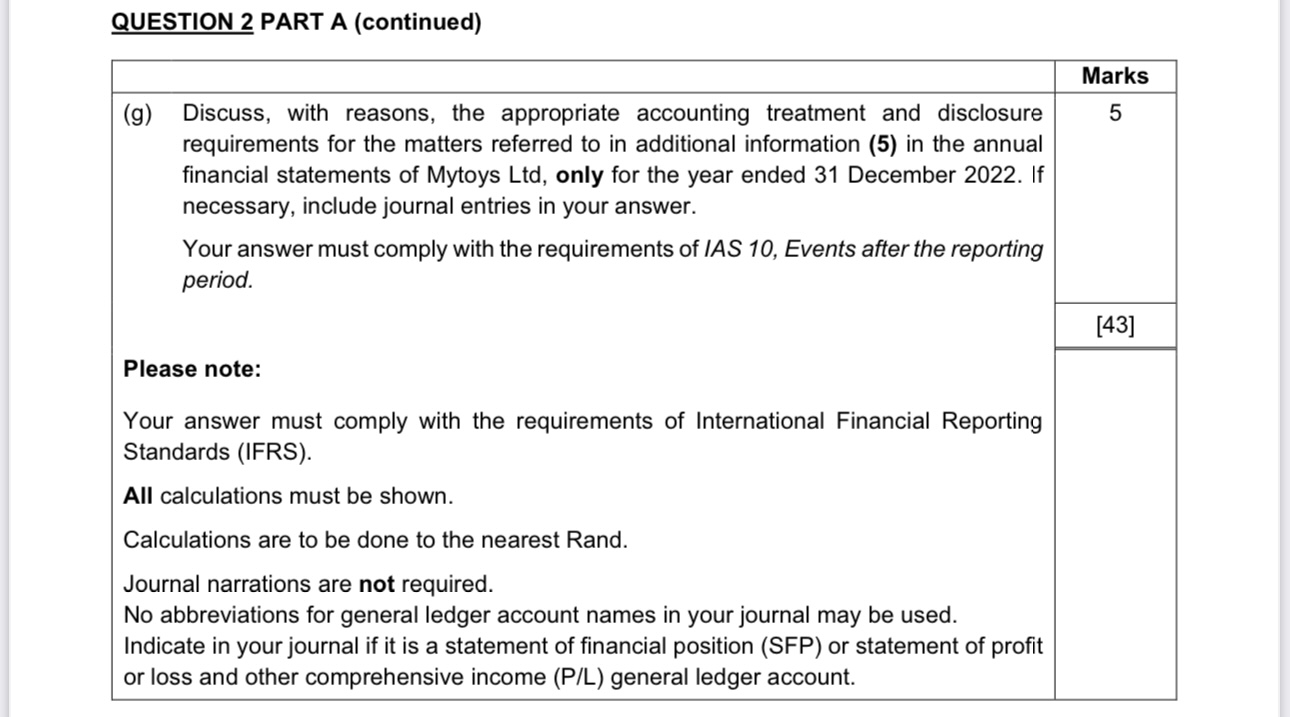

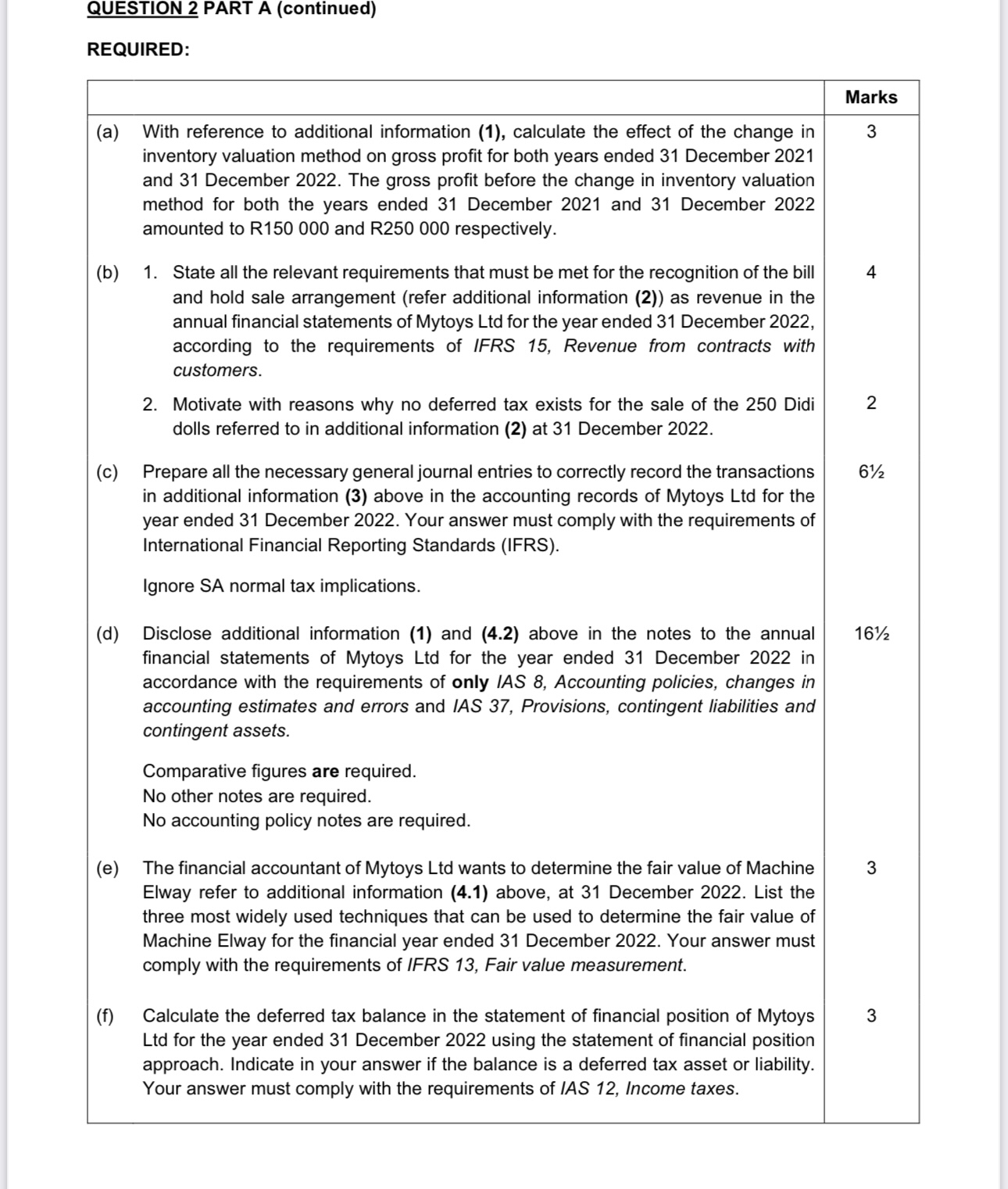

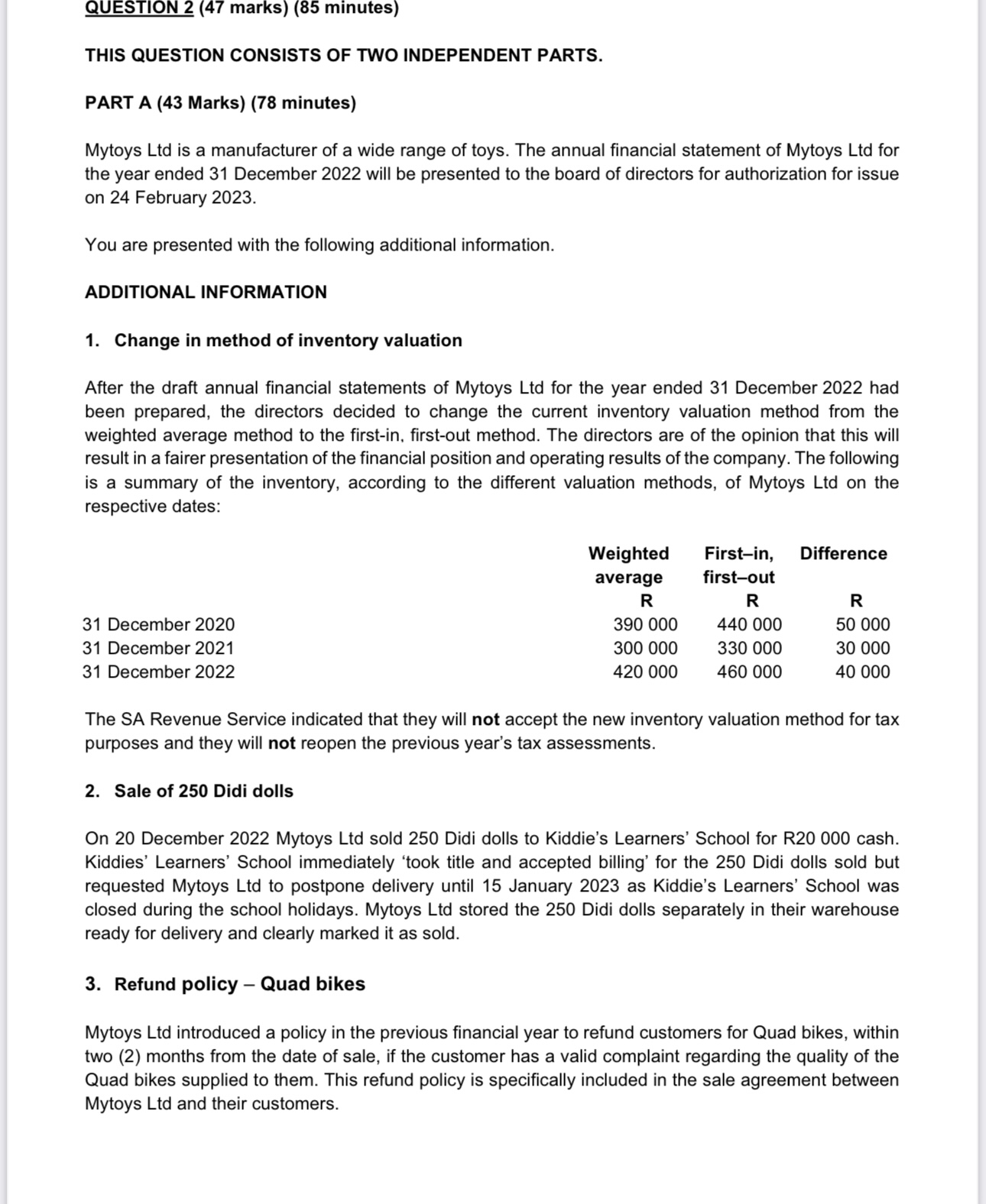

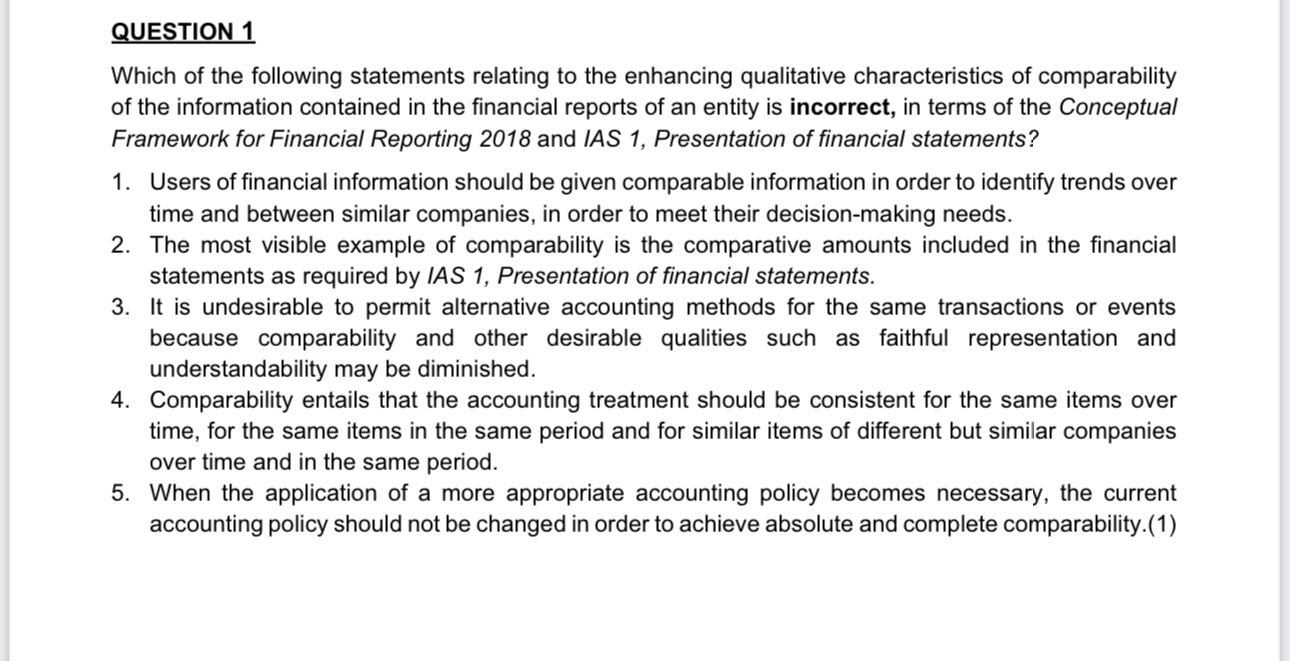

QUESTION 2 PART A (continued) Marks Discuss, with reasons. the appropriate accounting treatment and disclosure requirements for the matters referred to in additional information (5) in the annual nancial statements of Mytoys Ltd. only for the year ended 31 December 2022. If necessary. include journal entries in your answer. Your answer must comply with the requirements of 1A8 10, Events after the reporting period. Please note: Your answer must comply with the requirements of International Financial Reporting Standards (IFRS). All calculations must be shown. Calculations are to be done to the nearest Rand. Journal narrations are not required. No abbreviations for general ledger account names in yourjournal may be used. Indicate in yourjournal if it is a statement of nancial position (SFP) or statement of prot or loss and other comprehensive income (P!L] general ledger account. QUESTION 2 PART A (continued) REQUIRED: (b) (C) (d) (e) (1') With reference to additional information (1), calculate the effect of the change in inventory valuation method on gross prot for both years ended 31 December 2021 and 31 December 2022. The gross prot before the change in inventory valuation method for both the years ended 31 December 2021 and 31 December 2022 amounted to R150 000 and R250 000 respectively. 1. State all the relevant requirements that must be met for the recognition of the bill and hold sale arrangement (refer additional information (2)) as revenue in the annual nancial statements of Mytoys Ltd for the year ended 31 December 2022, according to the requirements of iFRS 15, Revenue from contracts with customers. 2. Motivate with reasons why no deferred tax exists for the sale of the 250 Didi dolls referred to in additional information (2) at 31 December 2022. Prepare all the necessary general joumal entries to correctly record the transactions in additional information (3) above in the accounting records of Mytoys Ltd for the year ended 31 December 2022. Your answer must comply with the requirements of International Financial Reporting Standards (IFRS). Ignore SA normal tax implications. Disclose additional information (1) and (4.2) above in the notes to the annual nancial statements of Mytoys Ltd for the year ended 31 December 2022 in accordance with the requirements of only MS 8, Accounting poiicies, changes in accounting estimates and errors and MS 37, Provisions, contingent iiabiiities and contingent assets. Comparative gures are required. No other notes are required. No accounting policy notes are required. The financial accountant of Mytoys Ltd wants to determine the fair value of Machine Elway refer to additional information (4.1) above, at 31 December 2022. List the three most widely used techniques that can be used to determine the fair value of Machine Elway for the nancial year ended 31 December 2022. Your answer must comply with the requirements of iFRS i 3, Fair value measurement. Calculate the deferred tax balance in the statement of nancial position of Mytoys Ltd for the year ended 31 December 2022 using the statement of nancial position approach. Indicate in your answer if the balance is a deferred tax asset or liability. Your answer must comply with the requirements of MS 1'2, income taxes. Marks 61/2 161/2 QUESTION 2 (47 marks) (85 minutes) THIS QUESTION CONSISTS OF TWO INDEPENDENT PARTS. PART A (43 Marks) (78 minutes) Mytoys Ltd is a manufacturer of a wide range of toys. The annual nancial statement of Mytoys Ltd for the year ended 31 December 2022 will be presented to the board of directors for authorization for issue on 24 February 2023. You are presented with the following additional information. ADDITIONAL INFORMATION 1. Change in method of inventory valuation After the draft annual nancial statements of Mytoys Ltd for the year ended 31 December 2022 had been prepared. the directors decided to change the current inventory valuation method from the weighted average method to the first-in. rst-out method. The directors are of the opinion that this will result in a fairer presentation of the financial position and operating results of the company. The following is a summary of the inventory. according to the different valuation methods, of Mytoys Ltd on the respective dates: Weighted Firstin, Difference average rst-out R R R 31 December 2020 390 000 440 000 50 000 31 December 2021 300 000 330 000 30 000 31 December 2022 420 000 460 000 40 000 The SA Revenue Service indicated that they will not accept the new inventory valuation method for tax purposes and they will not reopen the previous year's tax assessments. 2. Sale of 250 Didi dolls On 20 December 2022 Mytoys Ltd sold 250 Didi dolls to Kiddie's Learners' School for R20 000 cash. Kiddies' Learners' School immediately 'took title and accepted billing' for the 250 Didi dolls sold but requested Mytoys Ltd to postpone delivery until 15 January 2023 as Kiddie's Learners' School was closed during the school holidays. Mytoys Ltd stored the 250 Didi dolls separately in their warehouse ready for delivery and clearly marked it as sold. 3. Refund policy Quad bikes Mytoys Ltd introduced a policy in the previous nancial year to refund customers for Quad bikes, within two (2) months from the date of sale. if the customer has a valid complaint regarding the quality of the Quad bikes supplied to them. This refund policy is specically included in the sale agreement between Mytoys Ltd and their customers. QUESTION 1 Which of the following statements relating to the enhancing qualitative characteristics of comparability of the information contained in the nancial reports of an entity is incorrect, in terms of the Conceptual Framework for Financial Reporting 2018 and MS 1, Presentation of financial statements? 1. Users of nancial information should be given comparable information in order to identify trends over time and between similar companies, in order to meet their decision-making needs. The most visible example of comparability is the comparative amounts included in the nancial statements as required by MS 1, Presentation of nanciat statements. It is undesirable to permit alternative accounting methods for the same transactions or events because comparability and other desirable qualities such as faithful representation and understandability may be diminished. Comparability entails that the accounting treatment should be consistent for the same items over time, for the same items in the same period and for similar items of different but similar companies over time and in the same period. When the application of a more appropriate accounting policy becomes necessary, the current accounting policy should not be changed in order to achieve absolute and complete comparability.(1) QUESTION 2 PART A (continued) A provision for refunds. amounting to R170 000. was made in the annual financial statements of Mytoys Ltd for the year ended 31 December 2021 (2020: Rnil), based on the past sales history. During the current nancial year R60 000 was paid to dissatised customers for Quad Bikes returned, of which R19 400 related to sales of Quad Bikes for the year ended 31 December 2021. The nancial director estimated that R156 000 will be refunded to dissatised customers in the rst two months of the next nancial year, relating to Quad Bikes sold during the year ended 31 December 2022. All the transactions relating to the payments and provisions for refunds for the current year have not been recorded yet in the accounting records of Mytoys Ltd for the year ended 31 December 2022. 4. Purchase of Machine Elway 4.1. On 1 January 2022 machine Elway was acquired for the purpose of packaging toys manufactured by Mytoys Ltd at a cost of R150 000. Depreciation and the tax allowance on machine Elway for the current year both amounted to R30 000. 4.2. On 1 September 2022. an employee of Mytoys Ltd instituted a claim of R150 000 against Mytoys Ltd for injuries sustained on 15 August 2022 whilst operating the Elway machine. At year end 31 December 2022, the legal advisors of Mytoys Ltd are of the opinion that it is not probable that Mytoys Ltd will be found liable as all staff were trained to use the Elway machine and were asked to use the Elway machine at their own risk. 5. Inventory On 10 January 2023, part of the inventory of Mytoys Ltd was stolen, which resulted in a loss of R450 000 to the company. This loss includes inventory with a cost amounting to R280 000 that was on hand on 31 December 2022. Mytoys Ltd was not insured for any loss of inventory due to theft. On 20 January 2023 a major competitor of Mytoys Ltd launched a marketing campaign to signicantly reduce the selling prices of playsets. As a result. the sales director of Mytoys Ltd had to also reduce the selling price of their playsets, in order to retain their current market share. The cost of playsets included in inventory of Mytoys Ltd on 31 December 2022. amounted to R190 000. The market selling price of these playsets on hand at year end on 31 December 2022 amounted to R160 000. This information has not been recorded yet in the accounting records of Mytoys Ltd for the year ended 31 December 2022. 6. Taxation The company provides for deferred tax on all temporary differences using the statement of nancial position approach. There is certainty beyond any reasonable doubt that there will be sufcient taxable prot in the future against which any deductible temporary differences can be utilized. There are no other exempt or temporary differences except those mentioned in the question. The SA Normal tax rate remained unchanged at 28% for the past few years. 7. Assume that all amounts are material. 8. Ignore the time value of money. QUESTION 2 PART B (Continued) QUESTION 2 According to IAS 1, Presentation of Financial Statements, which one of the following statements relating to the general features of financial statements of an entity is incorrect? 1. Financial statements of an entity are prepared using the cash flow basis of accounting, with the exception of the cash flow statement which uses the accrual basis of accounting. 2 . Financial statements of an entity present material classes of similar items separately. Financial statements of an entity do not offset assets and liabilities or income and expenses, unless specifically required or permitted by an International Financial Reporting Standard (IFRS) 4. When the financial statements are prepared on the going concern basis it means that the statement of profit or loss and other comprehensive income and the statement of financial positions are drafted on the assumption that there is no intention or need to cease or materially curtail operations, 5. All numerical information presented in financial statements should be accompanied by a comparative amount for the preceding period, unless a standard or interpretation permits otherwise. (1) QUESTION 3 Which of the following circumstances will not give rise to separate disclosure on the face of the statement of profit or loss and other comprehensive income or in the notes of Oilex Lid , a retailer of oil products for the year ended 31 December 2021 according to IAS 1, Presentation of financial statements? 1. Write-down of closing inventory to net realisable value. 2. The reversal of write-downs to the recoverable amount of an investment property. 3 . The profit on disposal of shares held in a subsidiary. 4. The reversal of provision for claims against the reporting entity. 5. Monthly salaries and wages paid to employees. (1) QUESTION 4 If an entity changes the presentation or classification of items in its financial statements, it shall reclassify comparative amounts unless it is impracticably. Which of the following items is not required to be disclosed when an entity decides to reclassify comparative amounts, according to IAS 1, Presentation of financial statements? 1. The nature of the reclassification. 2. The effect of the reclassification on future periods for material and immaterial items. 3. The amount of each item or class of items that is reclassified for the preceding period. 4. The reason for the reclassification. 5. The reason for not reclassifying amounts when it is impracticably to reclassify comparative amounts. (1)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!