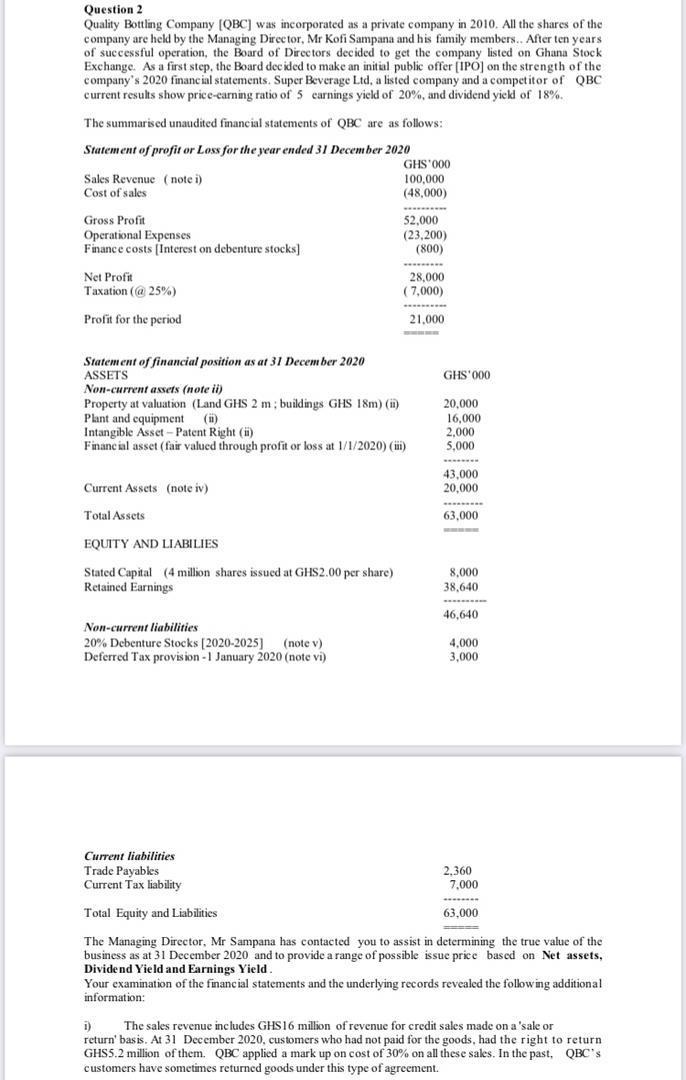

Question 2 Quality Bottling Company [QBC] was incorporated as a private company in 2010. All the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

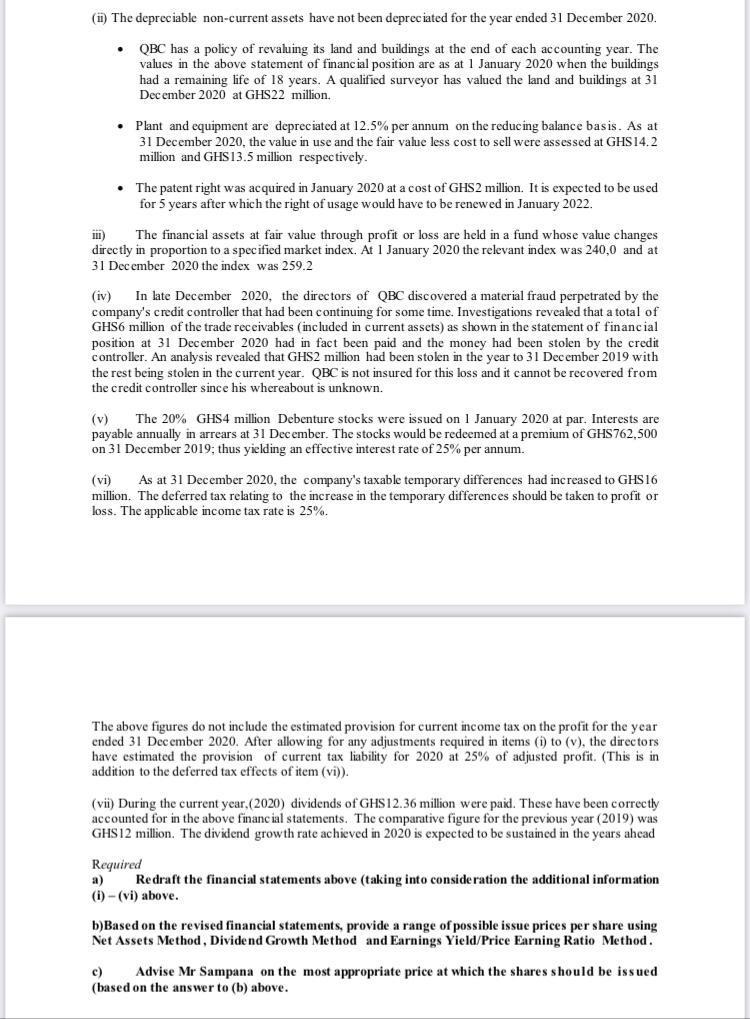

Question 2 Quality Bottling Company [QBC] was incorporated as a private company in 2010. All the shares of the company are held by the Managing Director, Mr Kofi Sampana and his family members.. After ten years. of successful operation, the Board of Directors decided to get the company listed on Ghana Stock Exchange. As a first step, the Board decided to make an initial public offer [IPO] on the strength of the company's 2020 financial statements. Super Beverage Ltd, a listed company and a competitor of QBC current results show price-carning ratio of 5 earnings yield of 20%, and dividend yield of 18%. The summarised unaudited financial statements of QBC are as follows: Statement of profit or Loss for the year ended 31 December 2020 GHS'000 Sales Revenue (note i) Cost of sales 100,000 (48,000) ********** Gross Profit 52,000 Operational Expenses (23,200) Finance costs [Interest on debenture stocks] (800) Net Profit 28,000 Taxation (@25%) (7,000) Profit for the period 21,000 Statement of financial position as at 31 December 2020 ASSETS GHS'000 Non-current assets (note ii) Property at valuation (Land GHS 2 m; buildings GHS 18m) (ii) 20,000 Plant and equipment (ii) 16,000 Intangible Asset-Patent Right (ii) 2,000 Financial asset (fair valued through profit or loss at 1/1/2020) (iii) 5,000 ******** 43,000 20,000 Current Assets (note iv) ********* Total Assets 63,000 EQUITY AND LIABILIES Stated Capital (4 million shares issued at GHS2.00 per share) Retained Earnings 8,000 38,640 46,640 Non-current liabilities 20% Debenture Stocks [2020-2025] (note v) Deferred Tax provision-1 January 2020 (note vi) 4,000 3,000 Current liabilities Trade Payables Current Tax liability 2.360 7,000 ******** Total Equity and Liabilities 63,000 - The Managing Director, Mr Sampana has contacted you to assist in determining the true value of the business as at 31 December 2020 and to provide a range of possible issue price based on Net assets, Dividend Yield and Earnings Yield. Your examination of the financial statements and the underlying records revealed the following additional information: i) The sales revenue includes GHS16 million of revenue for credit sales made on a 'sale or return' basis. At 31 December 2020, customers who had not paid for the goods, had the right to return. GHS5.2 million of them. QBC applied a mark up on cost of 30% on all these sales. In the past, QBC's customers have sometimes returned goods under this type of agreement. (ii) The depreciable non-current assets have not been depreciated for the year ended 31 December 2020. QBC has a policy of revaluing its land and buildings at the end of each accounting year. The values in the above statement of financial position are as at 1 January 2020 when the buildings had a remaining life of 18 years. A qualified surveyor has valued the land and buildings at 31 December 2020 at GHS22 million.. Plant and equipment are depreciated at 12.5% per annum on the reducing balance basis. As at 31 December 2020, the value in use and the fair value less cost to sell were assessed at GHS14.2 million and GHS13.5 million respectively. The patent right was acquired in January 2020 at a cost of GHS2 million. It is expected to be used for 5 years after which the right of usage would have to be renewed in January 2022. II) The financial assets at fair value through profit or loss are held in a fund whose value changes directly in proportion to a specified market index. At 1 January 2020 the relevant index was 240,0 and at 31 December 2020 the index was 259.2 (iv) In late December 2020, the directors of QBC discovered a material fraud perpetrated by the company's credit controller that had been continuing for some time. Investigations revealed that a total of GHS6 million of the trade receivables (included in current assets) as shown in the statement of financial position at 31 December 2020 had in fact been paid and the money had been stolen by the credit controller. An analysis revealed that GHS2 million had been stolen in the year to 31 December 2019 with the rest being stolen in the current year. QBC is not insured for this loss and it cannot be recovered from the credit controller since his whereabout is unknown. (v) The 20% GHS4 million Debenture stocks were issued on 1 January 2020 at par. Interests are payable annually in arrears at 31 December. The stocks would be redeemed at a premium of GHS762,500 on 31 December 2019; thus yielding an effective interest rate of 25% per annum. (vi) As at 31 December 2020, the company's taxable temporary differences had increased to GHS 16 million. The deferred tax relating to the increase in the temporary differences should be taken to profit or loss. The applicable income tax rate is 25%. The above figures do not include the estimated provision for current income tax on the profit for the year ended 31 December 2020. After allowing for any adjustments required in items (i) to (v), the directors. have estimated the provision of current tax liability for 2020 at 25% of adjusted profit. (This is in addition to the deferred tax effects of item (vi)). (vii) During the current year, (2020) dividends of GHS12.36 million were paid. These have been correctly accounted for in the above financial statements. The comparative figure for the previous year (2019) was GHS12 million. The dividend growth rate achieved in 2020 is expected to be sustained in the years ahead Required Redraft the financial statements above (taking into consideration the additional information (i)-(vi) above. b)Based on the revised financial statements, provide a range of possible issue prices per share using Net Assets Method, Dividend Growth Method and Earnings Yield/Price Earning Ratio Method. c) Advise Mr Sampana on the most appropriate price at which the shares should be issued (based on the answer to (b) above. Question 2 Quality Bottling Company [QBC] was incorporated as a private company in 2010. All the shares of the company are held by the Managing Director, Mr Kofi Sampana and his family members.. After ten years. of successful operation, the Board of Directors decided to get the company listed on Ghana Stock Exchange. As a first step, the Board decided to make an initial public offer [IPO] on the strength of the company's 2020 financial statements. Super Beverage Ltd, a listed company and a competitor of QBC current results show price-carning ratio of 5 earnings yield of 20%, and dividend yield of 18%. The summarised unaudited financial statements of QBC are as follows: Statement of profit or Loss for the year ended 31 December 2020 GHS'000 Sales Revenue (note i) Cost of sales 100,000 (48,000) ********** Gross Profit 52,000 Operational Expenses (23,200) Finance costs [Interest on debenture stocks] (800) Net Profit 28,000 Taxation (@25%) (7,000) Profit for the period 21,000 Statement of financial position as at 31 December 2020 ASSETS GHS'000 Non-current assets (note ii) Property at valuation (Land GHS 2 m; buildings GHS 18m) (ii) 20,000 Plant and equipment (ii) 16,000 Intangible Asset-Patent Right (ii) 2,000 Financial asset (fair valued through profit or loss at 1/1/2020) (iii) 5,000 ******** 43,000 20,000 Current Assets (note iv) ********* Total Assets 63,000 EQUITY AND LIABILIES Stated Capital (4 million shares issued at GHS2.00 per share) Retained Earnings 8,000 38,640 46,640 Non-current liabilities 20% Debenture Stocks [2020-2025] (note v) Deferred Tax provision-1 January 2020 (note vi) 4,000 3,000 Current liabilities Trade Payables Current Tax liability 2.360 7,000 ******** Total Equity and Liabilities 63,000 - The Managing Director, Mr Sampana has contacted you to assist in determining the true value of the business as at 31 December 2020 and to provide a range of possible issue price based on Net assets, Dividend Yield and Earnings Yield. Your examination of the financial statements and the underlying records revealed the following additional information: i) The sales revenue includes GHS16 million of revenue for credit sales made on a 'sale or return' basis. At 31 December 2020, customers who had not paid for the goods, had the right to return. GHS5.2 million of them. QBC applied a mark up on cost of 30% on all these sales. In the past, QBC's customers have sometimes returned goods under this type of agreement. (ii) The depreciable non-current assets have not been depreciated for the year ended 31 December 2020. QBC has a policy of revaluing its land and buildings at the end of each accounting year. The values in the above statement of financial position are as at 1 January 2020 when the buildings had a remaining life of 18 years. A qualified surveyor has valued the land and buildings at 31 December 2020 at GHS22 million.. Plant and equipment are depreciated at 12.5% per annum on the reducing balance basis. As at 31 December 2020, the value in use and the fair value less cost to sell were assessed at GHS14.2 million and GHS13.5 million respectively. The patent right was acquired in January 2020 at a cost of GHS2 million. It is expected to be used for 5 years after which the right of usage would have to be renewed in January 2022. II) The financial assets at fair value through profit or loss are held in a fund whose value changes directly in proportion to a specified market index. At 1 January 2020 the relevant index was 240,0 and at 31 December 2020 the index was 259.2 (iv) In late December 2020, the directors of QBC discovered a material fraud perpetrated by the company's credit controller that had been continuing for some time. Investigations revealed that a total of GHS6 million of the trade receivables (included in current assets) as shown in the statement of financial position at 31 December 2020 had in fact been paid and the money had been stolen by the credit controller. An analysis revealed that GHS2 million had been stolen in the year to 31 December 2019 with the rest being stolen in the current year. QBC is not insured for this loss and it cannot be recovered from the credit controller since his whereabout is unknown. (v) The 20% GHS4 million Debenture stocks were issued on 1 January 2020 at par. Interests are payable annually in arrears at 31 December. The stocks would be redeemed at a premium of GHS762,500 on 31 December 2019; thus yielding an effective interest rate of 25% per annum. (vi) As at 31 December 2020, the company's taxable temporary differences had increased to GHS 16 million. The deferred tax relating to the increase in the temporary differences should be taken to profit or loss. The applicable income tax rate is 25%. The above figures do not include the estimated provision for current income tax on the profit for the year ended 31 December 2020. After allowing for any adjustments required in items (i) to (v), the directors. have estimated the provision of current tax liability for 2020 at 25% of adjusted profit. (This is in addition to the deferred tax effects of item (vi)). (vii) During the current year, (2020) dividends of GHS12.36 million were paid. These have been correctly accounted for in the above financial statements. The comparative figure for the previous year (2019) was GHS12 million. The dividend growth rate achieved in 2020 is expected to be sustained in the years ahead Required Redraft the financial statements above (taking into consideration the additional information (i)-(vi) above. b)Based on the revised financial statements, provide a range of possible issue prices per share using Net Assets Method, Dividend Growth Method and Earnings Yield/Price Earning Ratio Method. c) Advise Mr Sampana on the most appropriate price at which the shares should be issued (based on the answer to (b) above.

Expert Answer:

Answer rating: 100% (QA)

a Sales 16000000 Cost of sales 100000 Plant and equipment depreciation 125 of 277 million 346250 Pat... View the full answer

Related Book For

Fundamentals of Financial Accounting

ISBN: 978-0078025914

5th edition

Authors: Fred Phillips, Robert Libby, Patricia Libby

Posted Date:

Students also viewed these accounting questions

-

The Kare Counseling Center was incorporated as a not-for-profit organization 10 years ago. Its adjusted trial balance as of June 30, 2020, follows. 1. Salaries and fringe benefits were allocated to...

-

Statements of profit and loss for the year ended 31 march 2015: Byby Cycle RM000 RM000 Revenue 24,200 10,800 Cost of sales -17,800 -6,800 Gross profit 6,400 4,000 Distribution cost -500 -340...

-

After stocktaking for the year ended 31 May 20X2 had taken place, the closing inventory of Cobden Ltd was aggregated to a figure of 87,612. During the course of the audit that followed, the...

-

choess answaer that How many bits are required to store one BCD digit?" 2 8 1 Kilo bits are equal to 1000 bits 1024 bits 1012 bits 1008 bits The function of the encoder is to convert coded...

-

Callison Company performs the following accounting tasks during the year. ______Analyzing and interpreting information. ______Classifying economic events. ______Explaining uses, meaning, and...

-

(a) A compound with formula RuCl3.5H2O is dissolved in water, forming a solution that is approximately the same color as the solid. Immediately after forming the solution, the addition of excess...

-

For a sample of size n = 20, the following values were obtained: b0 = 1.05, b1 = 4.50, se = 0.54, (x x )2 = 10.9, x = 8.52. Construct a 95% confidence interval for the mean response when x = 10.

-

Sara Collier, the bookkeeper for Danner, Cheney, and Howe, a political consulting firm, has recently completed an accounting course at her local college. One of the topics covered in the course was...

-

Sprints stock is currently trading at $36.00 The stock will pay a dividend of $3.40 and dividends are expected to increase by 7.00% thereafter. What is the cost of equity for Sprint based on the...

-

On January 1, 20X1, Wade Crimbring, Inc., a dealer in used manufacturing equipment, sold a CNC milling machine to Fletcher Bros., a new business that plans to fabricate utility trailers. To conserve...

-

This is Shakira's first week on her new job at Jack in the Box food restaurant.. She has had the opportunity to work with two of the shift managers. She notices that the morning manager assigns tasks...

-

How do shifts in both demand and supply affect equilibrium quantities and prices?

-

What will happen to the equilibrium price and quantity of overnight letter delivery service as the price of Internet access falls?

-

What will happen to the equilibrium price and quantity of tennis balls if court rental fees decline?

-

What is the elasticity of supply of land within the borough limits of Manhattan?

-

What is the elasticity of supply of lemonade?

-

7.9.1 Determine the force P for each of the 3 pulley systems. The weight of the load is 100N in each case. (a) (b)

-

Refer to Example 9.15. Add the following functionality to this program: Allow the user to enter the cost of a gallon of gas on each trip and use a function, Cost() to calculate the cost of purchasing...

-

For each of the following independent situations, prepare journal entries to record the initial trans-action on December 31 and the adjustment required on January 31. a. Magnificent Magazines...

-

Sonic Corp. runs the largest chain of drive-in restaurants in the United States. In its 10-K filed on November 25, 2013, Sonic reported the following changes in the Allowance for Doubtful Accounts...

-

How do the accounting methods used for passive investments and investments involving a significant influence differ?

-

Use Lagrange's equation to derive the equations governing the rotations \(\theta_{1}, \theta_{2}\), and \(\theta_{3}\) for the springconnected triple pendulum system shown in Figure 5.41. 6000 k 6000...

-

A rigid beam acts as a compound pendulum, suspended from an elastically restrained block that can undergo horizontal motion, as drawn in Figure 5.43. Derive the equations of motion using Lagrange's...

-

A pendulum is suspended from a torsionally restrained disk, as in Figure 5.42, where \(\alpha\) is the angle of rotation of the disk, and \(\theta\) is the relative angle of the pendulum measured...

Study smarter with the SolutionInn App