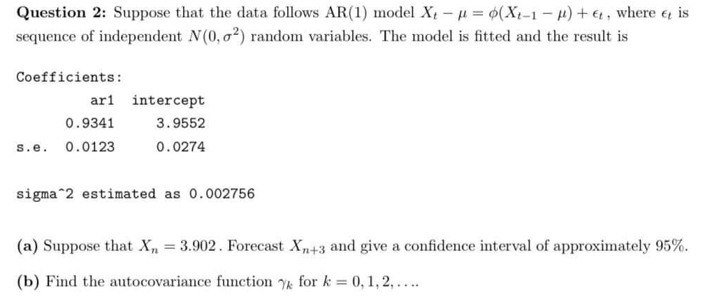

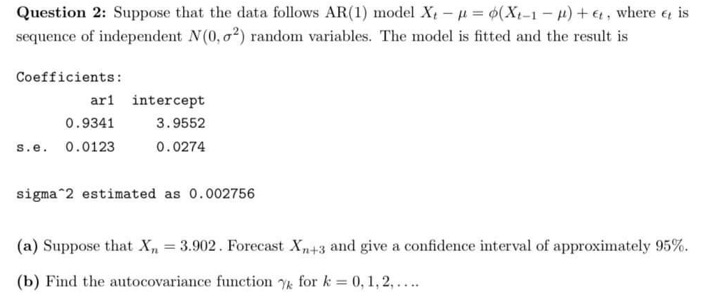

Question: Question 2: Suppose that the data follows AR(1) model Xt - p = $(Xt-1 - /) + e , where et is sequence of independent

Question 2: Suppose that the data follows AR(1) model Xt - p = $(Xt-1 - /) + e , where et is sequence of independent NV(0, o') random variables. The model is fitted and the result is Coefficients : ari intercept 0. 9341 3. 9552 s.e. 0. 0123 0. 0274 sigma*2 estimated as 0. 002756 (a) Suppose that X, = 3.902 . Forecast X,+3 and give a confidence interval of approximately 95%. (b) Find the autocovariance function % for k = 0, 1, 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock