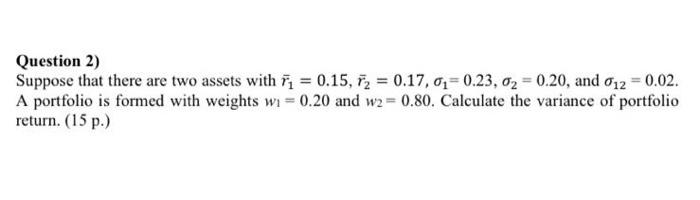

Question: Question 2) Suppose that there are two assets with 77 = 0.15, r2 = 0.17.0,= 0.23, 02 = 0.20, and 012 = 0.02. A portfolio

Question 2) Suppose that there are two assets with 77 = 0.15, r2 = 0.17.0,= 0.23, 02 = 0.20, and 012 = 0.02. A portfolio is formed with weights wi = 0.20 and w2=0.80. Calculate the variance of portfolio return. (15 p.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock