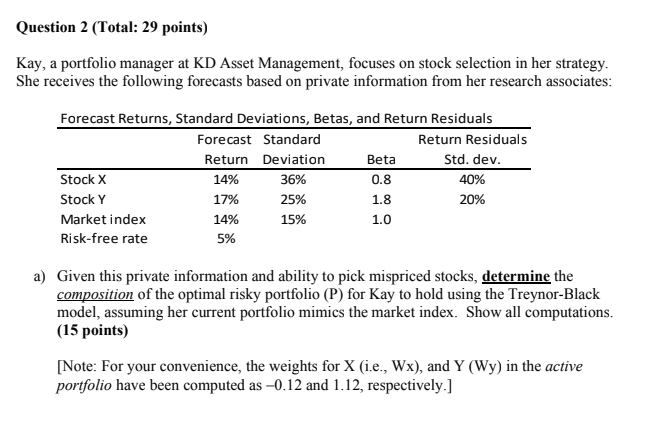

Question: Question 2 (Total: 29 points) Kay, a portfolio manager at KD Asset Management, focuses on stock selection in her strategy She receives the following forecasts

Question 2 (Total: 29 points) Kay, a portfolio manager at KD Asset Management, focuses on stock selection in her strategy She receives the following forecasts based on private information from her research associates Forecast Returns, Standard Deviations, Betas, and Return Residuals Forecast Standard Beta 0.8 1.8 1.0 Return Residuals Std. dev 40% 20% Return Deviation Stock X Stock Y Market index Risk-free rate 14% 1796 1496 5% 36% 25% 15% a) Given this private information and ability to pick mispriced stocks, determine the composition of the optimal risky portfolio (P) for Kay to hold using the Treynor-Blaclk model, assuming her current portfolio mimics the market index. Show all computations (15 points) [Note: For your convenience, the weights for X (i.e., Wx), and Y (Wy) in the active portfolio have been computed as -0.12 and .12, respectively.] b) Calculate the Sharpe ratio of the optimal risky portfolio, P, managed by Kay and compare it to that of the market index portfolio. Show your computations. (4 points) c) If Kay's client is risk averse with a coefficient of risk aversion of 4 (i.e. A-4), compute the exact makeup of the complete portfolio of the client (C), i.e., specify the percentage of funds that should be invested in X, Y, the market index portfolio, and the risk-free asset. Show all computations. (4 points) d) Based on the results you obtained above, graph and label the old and new investment opportunity sets as well as the optimal risky portfolio (P), active portfolio (A), market index portfolio (M), Kay's client portfolio (C), and the risk free rate (ri) for full credit. (6 points) Question 2 (Total: 29 points) Kay, a portfolio manager at KD Asset Management, focuses on stock selection in her strategy She receives the following forecasts based on private information from her research associates Forecast Returns, Standard Deviations, Betas, and Return Residuals Forecast Standard Beta 0.8 1.8 1.0 Return Residuals Std. dev 40% 20% Return Deviation Stock X Stock Y Market index Risk-free rate 14% 1796 1496 5% 36% 25% 15% a) Given this private information and ability to pick mispriced stocks, determine the composition of the optimal risky portfolio (P) for Kay to hold using the Treynor-Blaclk model, assuming her current portfolio mimics the market index. Show all computations (15 points) [Note: For your convenience, the weights for X (i.e., Wx), and Y (Wy) in the active portfolio have been computed as -0.12 and .12, respectively.] b) Calculate the Sharpe ratio of the optimal risky portfolio, P, managed by Kay and compare it to that of the market index portfolio. Show your computations. (4 points) c) If Kay's client is risk averse with a coefficient of risk aversion of 4 (i.e. A-4), compute the exact makeup of the complete portfolio of the client (C), i.e., specify the percentage of funds that should be invested in X, Y, the market index portfolio, and the risk-free asset. Show all computations. (4 points) d) Based on the results you obtained above, graph and label the old and new investment opportunity sets as well as the optimal risky portfolio (P), active portfolio (A), market index portfolio (M), Kay's client portfolio (C), and the risk free rate (ri) for full credit. (6 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts