Question: Question 2 Q.2 210 days ago you purchased a newly issued bond with a maturity of 10 years. The bond carries a coupon rate of

Question 2

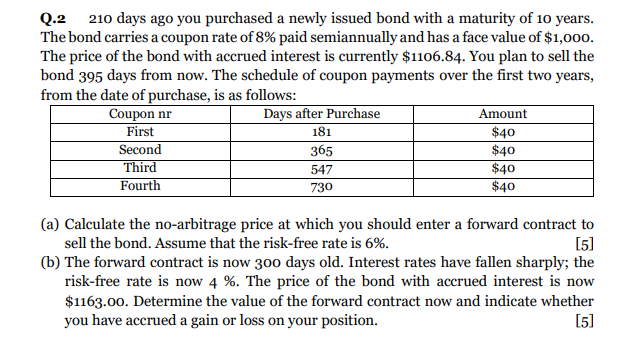

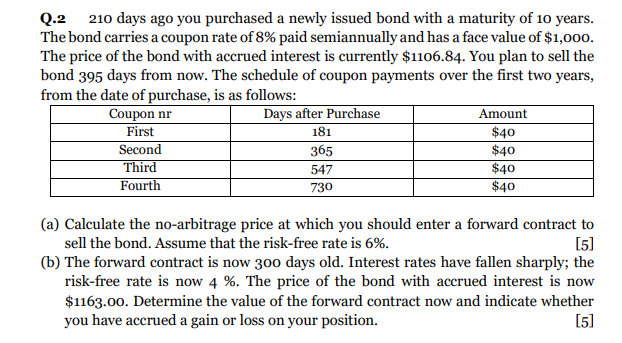

Q.2 210 days ago you purchased a newly issued bond with a maturity of 10 years. The bond carries a coupon rate of 8% paid semiannually and has a face value of $1,000. The price of the bond with accrued interest is currently $1106.84. You plan to sell the bond 395 days from now. The schedule of coupon payments over the first two years, from the date of purchase, is as follows: (a) Calculate the no-arbitrage price at which you should enter a forward contract to sell the bond. Assume that the risk-free rate is 6%. [5] (b) The forward contract is now 300 days old. Interest rates have fallen sharply; the risk-free rate is now 4%. The price of the bond with accrued interest is now $1163.oo. Determine the value of the forward contract now and indicate whether you have accrued a gain or loss on your position. Q.2 210 days ago you purchased a newly issued bond with a maturity of 10 years. The bond carries a coupon rate of 8% paid semiannually and has a face value of $1,000. The price of the bond with accrued interest is currently $1106.84. You plan to sell the bond 395 days from now. The schedule of coupon payments over the first two years, from the date of purchase, is as follows: (a) Calculate the no-arbitrage price at which you should enter a forward contract to sell the bond. Assume that the risk-free rate is 6%. [5] (b) The forward contract is now 300 days old. Interest rates have fallen sharply; the risk-free rate is now 4%. The price of the bond with accrued interest is now $1163.oo. Determine the value of the forward contract now and indicate whether you have accrued a gain or loss on your position

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts