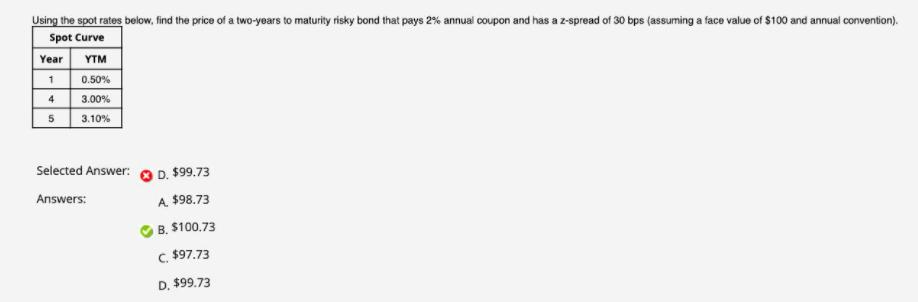

Question: Using the spot rates below, find the price of a two-years to maturity risky bond that pays 2% annual coupon and has a z-spread

Using the spot rates below, find the price of a two-years to maturity risky bond that pays 2% annual coupon and has a z-spread of 30 bps (assuming a face value of $100 and annual convention). Spot Curve Year YTM 0.50% 3.00% 4 3.10% Selected Answer: O D. $99.73 Answers: A $98.73 B. $100.73 C. $97.73 D. $99.73

Step by Step Solution

★★★★★

3.40 Rating (159 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock