Question: Question 20 (2 points) You just inherited $1,000,000 dollars. The universe of available securities includes two risky funds, A and B, and T-bills. The data

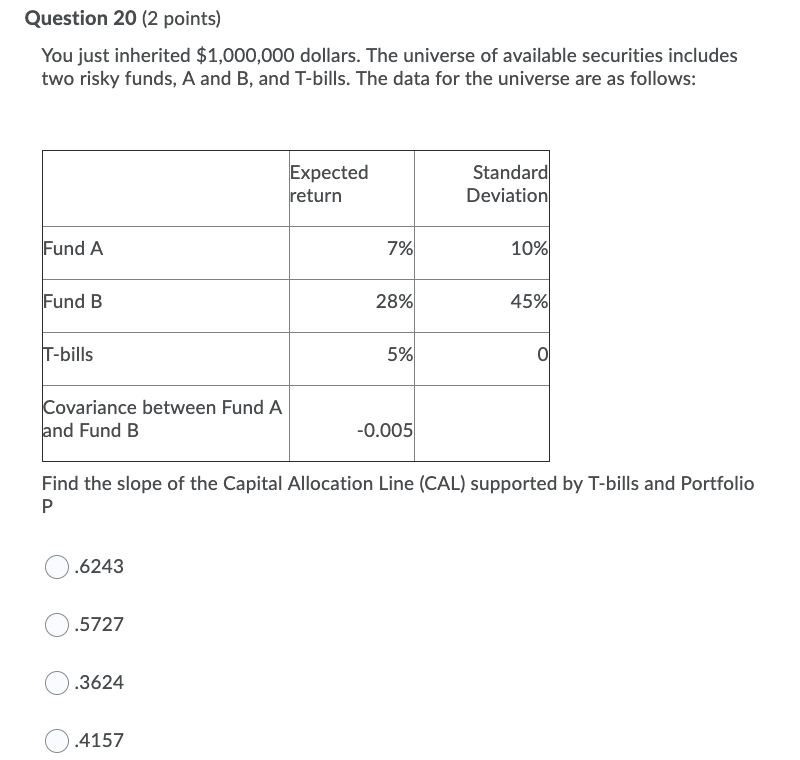

Question 20 (2 points) You just inherited $1,000,000 dollars. The universe of available securities includes two risky funds, A and B, and T-bills. The data for the universe are as follows: Expected return Standard Deviation Fund A 7% 10% Fund B 28% 45% T-bills 5% Covariance between Fund A and Fund B -0.005 Find the slope of the Capital Allocation Line (CAL) supported by T-bills and Portfolio 0.6243 0.5727 0.3624 0.4157

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock